Lazy-Bear-Momentum-Squeeze-Strategie

Übersicht

Die Lazy-Bear-Momentum-Squeeze-Strategie ist eine quantitative Handelsstrategie, die Bollinger-Bänder, Keltner-Kanäle und Momentumindikatoren kombiniert. Sie nutzt Bollinger-Bänder und Keltner-Kanäle, um zu beurteilen, ob sich der Markt derzeit in einer Squeeze-Phase befindet, und generiert dann zusammen mit dem Momentumindikator Handelssignale.

Der Hauptvorteil dieser Strategie besteht darin, dass sie automatisch den Beginn einer trendstarken Bewegung erkennen und mit Hilfe des Momentumindikators den Einstiegszeitpunkt bestimmen kann. Es gibt jedoch auch gewisse Risiken, die eine Parametereinstellung für verschiedene Instrumente erfordern.

Prinzip der Strategie

Die Lazy-Bear-Momentum-Squeeze-Strategie basiert auf den folgenden drei Indikatoren:

- Bollinger-Bänder: bestehend aus mittlerer Linie, oberer Linie und unterer Linie

- Keltner-Kanäle: bestehend aus mittlerer Linie, oberer Linie und unterer Linie

- Momentumindikator: Differenz zwischen dem aktuellen Preis und dem Preis vor n Tagen

Wenn die obere Linie der Bollinger-Bänder niedriger als die obere Linie der Keltner-Kanäle ist und die untere Linie der Bollinger-Bänder höher als die untere Linie der Keltner-Kanäle ist, nehmen wir an, dass sich der Markt in einer Squeeze-Phase befindet. Dies bedeutet normalerweise, dass eine trendstarke Bewegung kurz bevorsteht.

Um den Einstiegszeitpunkt zu bestimmen, verwenden wir den Momentumindikator, um die Geschwindigkeit der Preisänderung zu beurteilen. Wenn der Momentumwert seinen Durchschnitt nach oben durchbricht, wird ein Kaufsignal generiert; wenn der Momentumwert seinen Durchschnitt nach unten durchbricht, wird ein Verkaufssignal generiert.

Analyse der Strategievorteile

Die Hauptvorteile der Lazy-Bear-Momentum-Squeeze-Strategie sind:

- Sie kann den Beginn eines Trends automatisch erkennen und frühzeitig einsteigen

- Die Kombination mehrerer Indikatoren reduziert Fehlsignale

- Sie berücksichtigt sowohl Trend- als auch Umkehrhandelsansätze

- Die Parameter können individuell angepasst werden, um eine Optimierung für verschiedene Instrumente zu ermöglichen

Risikoanalyse

Die Lazy-Bear-Momentum-Squeeze-Strategie birgt auch gewisse Risiken:

- Die Wahrscheinlichkeit von Fehlsignalen der Bollinger-Bänder und Keltner-Kanäle ist relativ hoch

- Der Momentumindikator kann instabil sein und den optimalen Einstiegspunkt verpassen

- Ohne Parametereinstellung ist die Wirksamkeit beeinträchtigt

- Die Ergebnisse hängen stark vom gehandelten Instrument ab

Um die Risiken zu reduzieren, wird empfohlen, die Längenparameter der Bollinger-Bänder und Keltner-Kanäle zu optimieren, die Stop-Loss-Punkte anzupassen, liquide Handelsinstrumente zu wählen und die Signale mit anderen Indikatoren zu verifizieren.

Optimierungsrichtung der Strategie

Um die Wirkung der Lazy-Bear-Momentum-Squeeze-Strategie weiter zu verbessern, sind die wichtigsten Optimierungsrichtungen:

- Testen verschiedener Parameterkombinationen für verschiedene Instrumente und Zeitrahmen

- Optimieren der Längen der Bollinger-Bänder und Keltner-Kanäle

- Optimieren der Länge des Momentumindikators

- Unterschiedliche Stop-Loss- und Take-Profit-Strategien für Long- und Short-Positionen entwickeln

- Hinzufügen weiterer Indikatoren zur Signalverifizierung

Durch umfangreiche Tests und Optimierungen kann die Gewinnrate und Rentabilität dieser Strategie erheblich gesteigert werden.

Zusammenfassung

Die Lazy-Bear-Momentum-Squeeze-Strategie integriert mehrere Indikatoren mit starker Urteilskraft und kann den Beginn eines Trends effektiv erkennen. Allerdings gibt es auch gewisse Risiken, die eine Parametereinstellung für verschiedene Handelsinstrumente erfordern. Durch kontinuierliche Tests und Optimierungen kann diese Strategie zu einem effizienten algorithmischen Handelssystem werden.

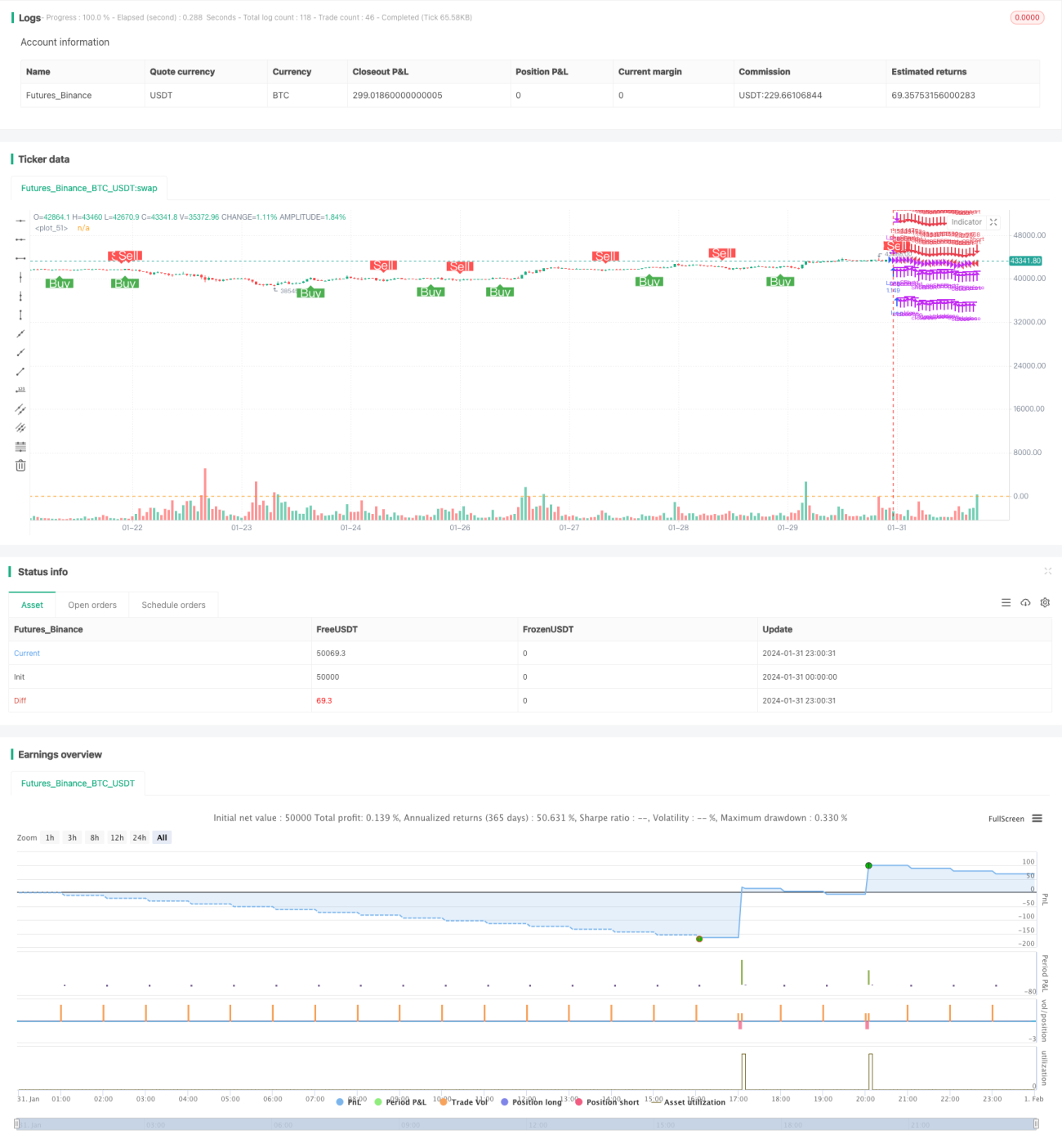

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1