Estrategia arcoíris de media móvil totalmente automática

Resumen

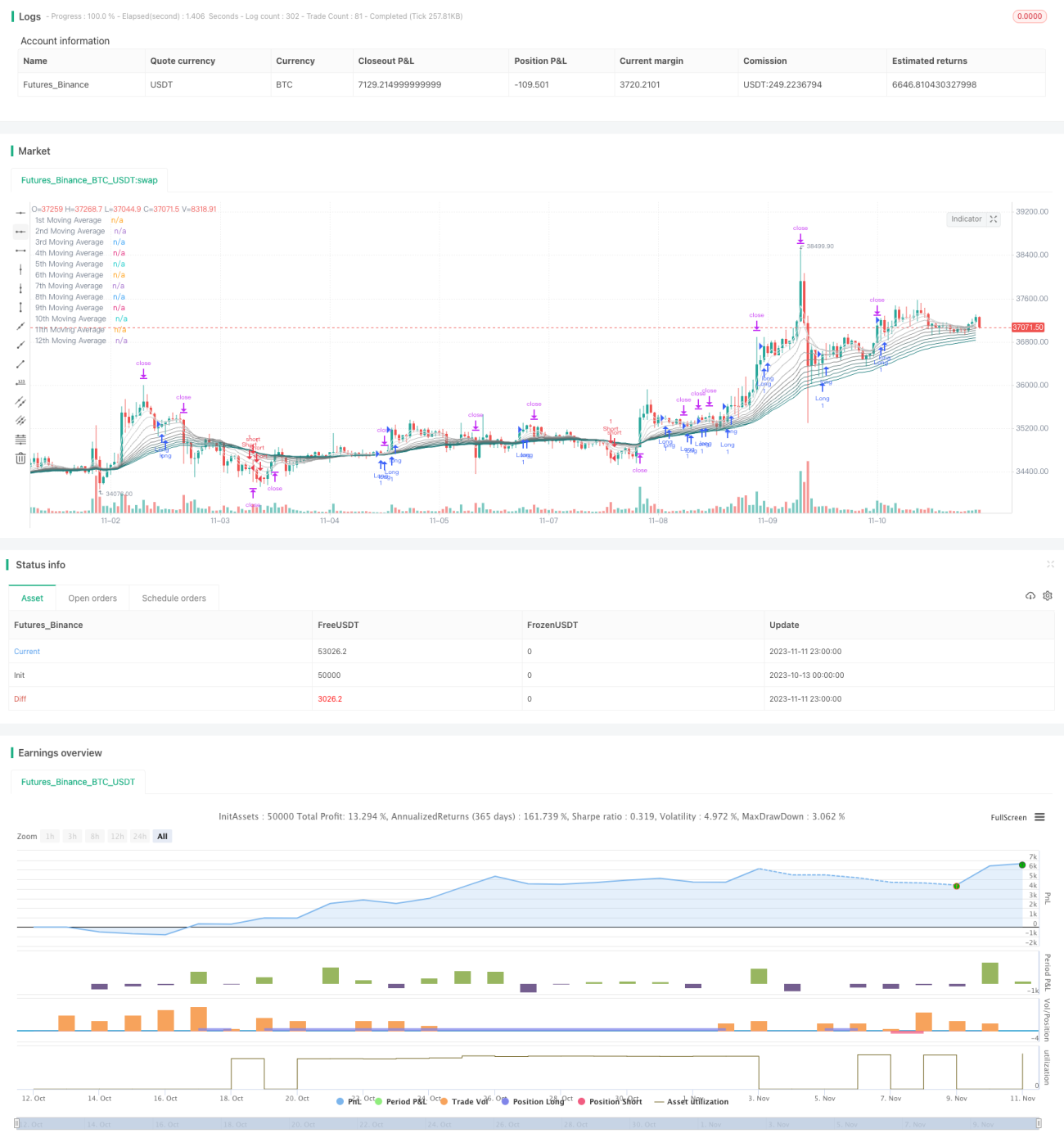

La Estrategia Arcoíris de Medias Móviles para Trading Automático Integral es una estrategia típica de combinación de medias móviles de múltiples períodos de tiempo. Utiliza 12 medias móviles de diferentes períodos, y determina la dirección del mercado y las condiciones para abrir posiciones, detener pérdidas y tomar ganancias mediante el orden de las medias móviles y la relación con el precio, logrando un trading automático. Esta estrategia puede identificar automáticamente la tendencia y cuenta con un mecanismo sólido de stop loss para controlar el riesgo.

Principio

La estrategia utiliza 12 medias móviles, incluyendo períodos de 3, 5, 8 hasta 55 períodos. El tipo de media móvil puede seleccionarse entre EMA, SMA, RMA, etc. Primero, la estrategia evalúa la relación de orden de las medias móviles de corto y largo plazo (líneas de 1 a 4 períodos y líneas de 5 a 8 períodos). Si las medias de corto plazo están por encima, se considera un entorno de tendencia alcista; si están por debajo, un entorno de tendencia bajista.

En una tendencia alcista, si el precio supera la media móvil correspondiente al mínimo anterior, se considera una señal de apertura de posición larga. El stop loss se sitúa en la media móvil correspondiente al mínimo anterior, y el take profit se establece a 1,6 veces la distancia del stop loss. En una tendencia bajista, si el precio supera la media móvil correspondiente al máximo anterior, se considera una señal de apertura de posición corta. El stop loss se sitúa en la media móvil correspondiente al máximo anterior, y el take profit es 1,6 veces la distancia del stop loss.

La estrategia también cuenta con una función de detección de reversión de tendencia. Durante la tenencia de una posición, si las medias móviles de corto plazo cambian su orden y el precio supera el máximo o mínimo más reciente, se considera una posible reversión de tendencia. En ese caso, se cierra la posición actual y se abre una posición en la dirección contraria, utilizando el nuevo máximo o mínimo como niveles de stop loss y take profit.

Ventajas

-

La estrategia utiliza análisis de múltiples marcos temporales, lo que permite identificar bien la dirección de la tendencia.

-

Incorpora el juicio sobre el orden ascendente o descendente de las medias móviles, evitando ser engañado por mercados en rango.

-

Cuenta con un mecanismo completo de stop loss que controla eficazmente el riesgo de cada operación.

-

Dispone de una función de detección de reversión de tendencia, que permite capturar oportunidades de reversión oportunamente y reducir el riesgo sistémico.

-

Los parámetros son flexibles; los períodos y tipos de medias móviles se pueden personalizar.

-

Utiliza un stop loss dinámico (trailing stop) para maximizar las ganancias.

Riesgos

-

Al tratarse de una estrategia de combinación de múltiples medias móviles, el rendimiento se ve afectado por la configuración de parámetros, por lo que requiere pruebas de optimización.

-

En mercados laterales, las medias móviles pueden generar señales falsas. Se deben ajustar los parámetros adecuadamente o abstenerse de operar.

-

Existe cierto rezago, lo que puede provocar pérdida de oportunidades cerca de los puntos de inflexión de la tendencia.

-

Se debe prestar atención a otros indicadores técnicos para evitar abrir posiciones cortas cerca de niveles de soporte importantes.

-

El riesgo sistémico debe ser monitoreado; el mecanismo de detección de reversión no lo elimina por completo.

-

Es necesario incorporar mecanismos adicionales para controlar el drawdown, como un gestión dinámica del tamaño de la posición.

Direcciones de optimización

-

Probar diferentes tipos de medias móviles y configuraciones de parámetros para encontrar la combinación óptima.

-

Optimizar el mecanismo de detección de reversión, estableciendo condiciones más precisas para su activación.

-

Incorporar un sistema de gestión dinámica del tamaño de la posición, reduciendo la exposición cuando el drawdown sea excesivo.

-

Considerar la incorporación de algoritmos de aprendizaje automático para entrenar modelos que identifiquen puntos clave con grandes volúmenes de datos.

-

Combinar señales de otros indicadores para mejorar la precisión de las decisiones.

-

Crear un portfolio de trading multi-instrumento para diversificar el riesgo mediante correlaciones bajas.

Resumen

La Estrategia Arcoíris de Medias Móviles para Trading Automático Integral es, en general, una estrategia sólida de seguimiento de tendencia, con una fuerte capacidad de identificación de tendencias y control de riesgos. Mediante la optimización de parámetros y la incorporación de gestión dinámica de posiciones, entre otras mejoras, puede convertirse en una estrategia de trading cuantitativo muy práctica. Sus ideas son claras y fáciles de entender, a la vez que ofrece cierta flexibilidad, lo que la hace digna de estudio, uso y optimización continua.

- 1