Estrategia de trading cuantitativo basada en múltiples indicadores

Resumen

Esta estrategia integra tres indicadores técnicos principales—medias móviles, el Índice de Fuerza Relativa (RSI) y el indicador de Convergencia/Divergencia de Medias Móviles (MACD)—para abrir y cerrar posiciones largas y cortas de forma automática. El nombre de la estrategia incluye "múltiples indicadores" para destacar la variedad de indicadores que emplea.

Principio de la estrategia

La estrategia determina la dirección de la tendencia comparando la relación entre dos medias móviles, y combina el indicador RSI para evitar perder oportunidades de reversión. Específicamente, utiliza EMA o SMA para calcular una línea rápida y una línea lenta. Cuando la línea rápida cruza por encima de la línea lenta, se genera una señal de compra; cuando la cruza por debajo, es una señal de venta. Para filtrar falsos rompimientos, la estrategia también incorpora una lógica direccional del RSI: solo cuando el RSI también cumple las condiciones se emite una señal de trading.

Además, la estrategia integra el indicador MACD para tomar decisiones de trading. Cuando la línea de diferencia del MACD cruza por encima de la línea cero, es una señal de compra; cuando cruza por debajo, es una señal de venta. Esto permite que el MACD detecte si la tendencia está cambiando, evitando señales erróneas en puntos de inflexión.

Análisis de ventajas

La mayor ventaja de esta estrategia es que integra múltiples indicadores para filtrar señales, lo que reduce eficazmente las señales falsas y mejora la calidad de las mismas. En concreto:

-

La combinación de líneas rápida y lenta con el RSI evita los falsos rompimientos que se producirían con el uso exclusivo de medias móviles.

-

La integración del MACD permite anticipar si la tendencia se va a revertir, evitando señales equivocadas en puntos de inflexión.

-

Permite elegir entre EMA o SMA, adaptando los parámetros del indicador a las características del mercado.

-

Ofrece opciones de gestión de capital para controlar el tamaño de cada orden, gestionando eficazmente el riesgo.

-

Incluye stop loss y take profit, lo que permite fijar ganancias y evitar pérdidas mayores.

Análisis de riesgos

La estrategia se enfrenta principalmente a los siguientes riesgos:

-

Una optimización inadecuada de los parámetros puede dar lugar a un rendimiento deficiente. Es necesario dedicar tiempo a probar distintas combinaciones de parámetros.

-

Aún existe la probabilidad de que los indicadores emitan señales falsas. Cuando los tres indicadores coinciden en una señal errónea, se pueden producir pérdidas significativas.

-

El rendimiento en un solo activo no es consistente; es necesario extender la estrategia a otros activos.

-

Datos insuficientes pueden hacer que la eficacia de la estrategia disminuya en el futuro.

Direcciones de optimización

La estrategia puede optimizarse en varios aspectos:

-

Probar diferentes combinaciones de parámetros de los indicadores para encontrar los óptimos.

-

Añadir un stop loss dinámico en el mecanismo de stop loss. Cuando el precio se mueve una cierta distancia, se puede usar un trailing stop para fijar ganancias.

-

Incorporar un indicador de tendencia de mayor plazo para evitar operar en contra de la tendencia principal, por ejemplo integrando el ADX.

-

Añadir un módulo de gestión de capital para mejorar el control del riesgo.

-

Incluir filtros de factores fundamentales como noticias.

Resumen

Esta estrategia integra múltiples indicadores técnicos (medias móviles, RSI y MACD) para identificar y filtrar señales direccionales largas y cortas. Su ventaja principal es que filtra eficazmente las señales falsas, mejorando la calidad de las señales. Sus principales desventajas son la selección de parámetros y la probabilidad residual de señales falsas por parte de los indicadores. Las futuras direcciones de optimización incluyen el ajuste de parámetros, la mejora del stop loss y el filtrado de tendencias. En general, la estrategia como marco de múltiples indicadores es efectiva, y requiere optimización y validación continuas.

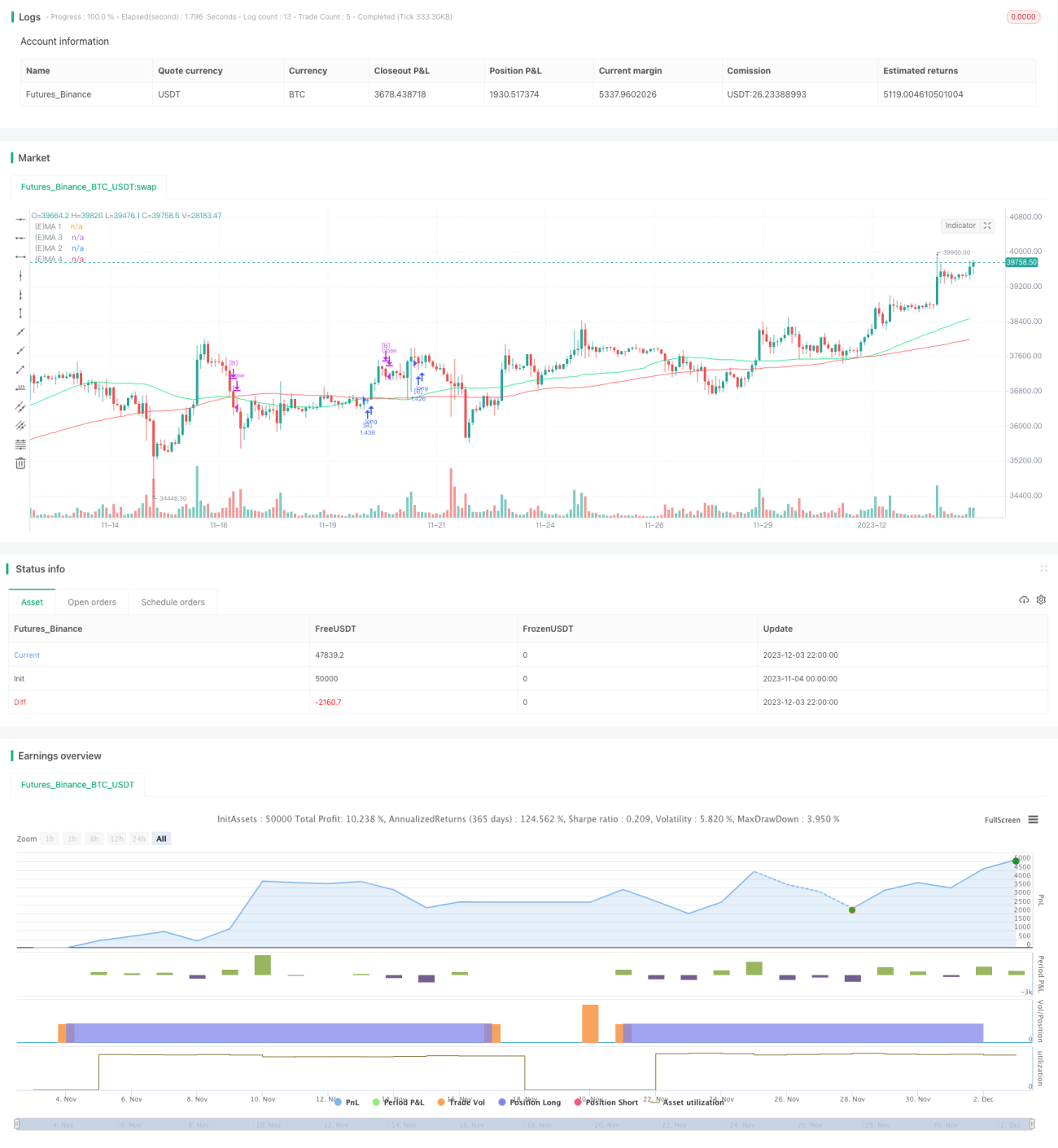

/*backtest

start: 2023-11-04 00:00:00

end: 2023-12-04 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fikira

//@version=4

strategy("Strategy Tester EMA-SMA-RSI-MACD", shorttitle="Strat-test", overlay=true, max_bars_back=5000, - 1