Estrategia de Engulfing de Super Trend

Resumen

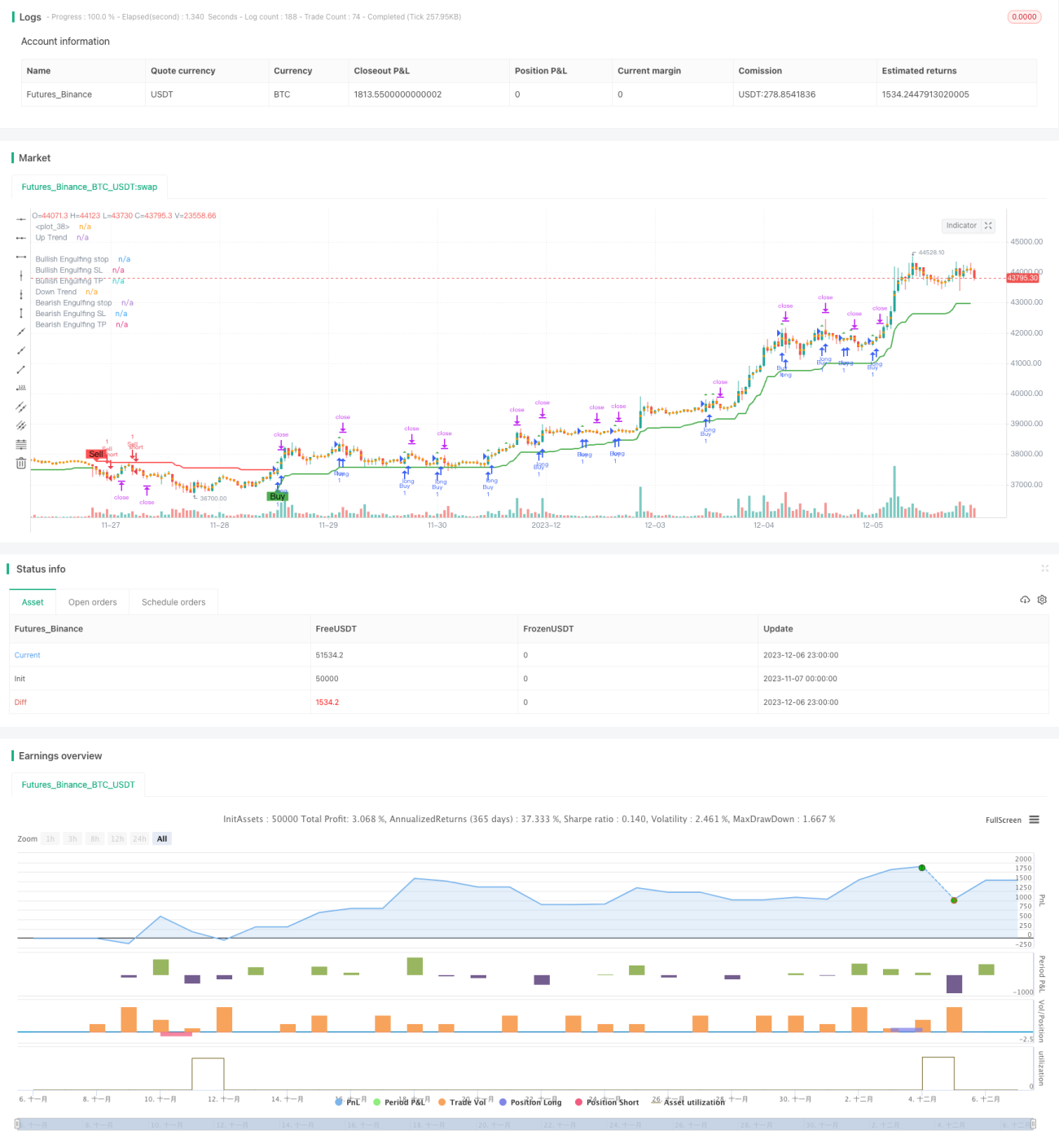

La estrategia de Engulfing de Tendencia Súper es una estrategia de seguimiento de tendencia que combina el Rango Verdadero Medio (ATR), el indicador de Tendencia Súper y el patrón de envolvimiento para identificar la dirección de la tendencia, y busca oportunidades de entrada con una relación favorable cuando el patrón de envolvimiento confirma la tendencia.

Principio de la Estrategia

Esta estrategia primero utiliza el ATR y el indicador de Tendencia Súper para determinar la dirección actual de la tendencia del mercado. Específicamente, cuando el precio está por debajo de la banda superior, se define como una tendencia bajista; cuando el precio está por encima de la banda inferior, se define como una tendencia alcista.

Al confirmar la dirección de la tendencia, la estrategia también juzga si la vela forma un patrón de envolvimiento. Según la lógica del código, en una tendencia alcista, cuando el cierre de la vela anterior es superior a la apertura de la vela actual y el cierre de la vela actual es inferior a su apertura, se desencadena un envolvimiento alcista. En una tendencia bajista, cuando el cierre de la vela anterior es inferior a la apertura de la vela actual y el cierre de la vela actual es superior a su apertura, se desencadena un envolvimiento bajista.

Cuando el patrón de envolvimiento coincide con la dirección de la tendencia, se genera una señal de trading. Además, la estrategia calcula niveles de stop-loss y take-profit basados en el patrón de envolvimiento. Una vez en la posición, si el precio alcanza el stop-loss o el take-profit, se sale de la posición actual.

Análisis de Ventajas

Esta estrategia combina las ventajas del seguimiento de tendencia y el reconocimiento de patrones, lo que permite identificar señales de reversión en mercados con tendencia, capturando movimientos significativos en los puntos de inflexión del mercado. Además, el mecanismo de stop-loss puede controlar eficazmente el riesgo de pérdidas.

Análisis de Riesgos

El mayor riesgo de esta estrategia es que el patrón de envolvimiento puede ser una ruptura falsa, generando señales erróneas. Además, la configuración de stop-loss y take-profit puede ser demasiado arbitraria, impidiendo alcanzar el punto de equilibrio. Se recomienda optimizar la combinación de parámetros y ajustar adecuadamente las posiciones de stop-loss y take-profit.

Direcciones de Optimización

Se puede considerar la optimización en tiempo real de los parámetros del ATR para capturar mejor los cambios en la volatilidad del mercado. También se pueden investigar otros indicadores para identificar la tendencia, mejorando aún más la estabilidad de la estrategia. En cuanto al stop-loss y take-profit, el trailing stop dinámico también es una idea factible de optimización.

Conclusión

La estrategia de Engulfing de Tendencia Súper integra las ventajas del seguimiento de tendencia y el reconocimiento de patrones, utilizando el patrón de envolvimiento como señal de reversión para obtener altos rendimientos en los puntos de inflexión del mercado. Sin embargo, también existe cierto riesgo de señales falsas, por lo que se requieren más pruebas y optimizaciones para controlar el riesgo.

- 1