Estrategia de bandas de Bollinger con stop-loss dinámico

Resumen

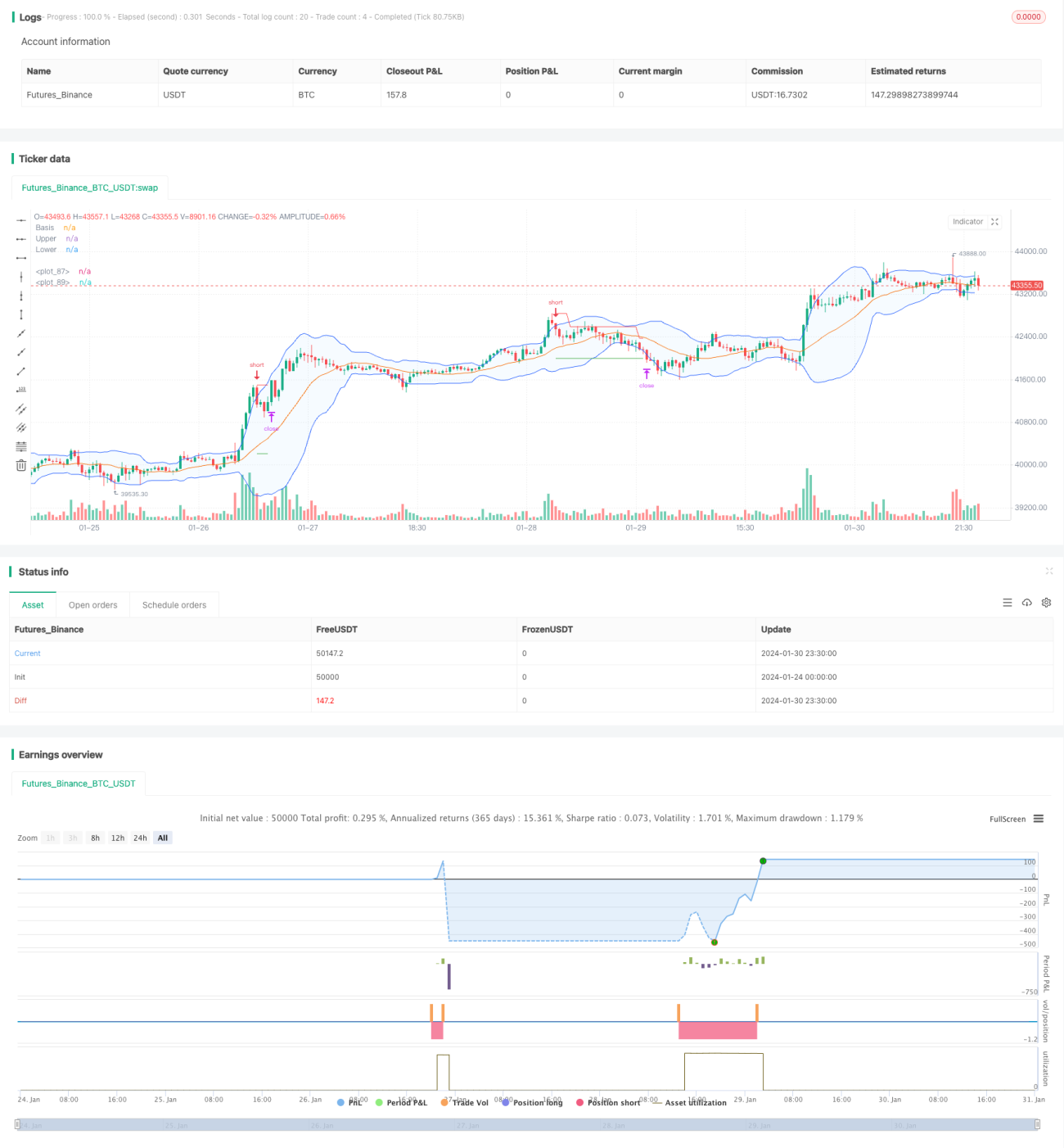

Esta estrategia utiliza las bandas superior e inferior de Bollinger para implementar un stop loss dinámico. Abre una posición corta cuando el precio supera la banda superior de Bollinger, y una posición larga cuando supera la banda inferior, con un stop loss dinámico que sigue la evolución del precio.

Principio

El núcleo de la estrategia reside en las bandas superior e inferior de Bollinger. La banda media es la media móvil de n días, la banda superior es la media móvil + k * desviación estándar de n días, y la banda inferior es la media móvil – k * desviación estándar de n días. Cuando el precio rebota al alza desde la banda inferior, se abre una posición larga; cuando el precio cae desde la banda superior, se abre una posición corta. Al mismo tiempo, la estrategia establece un nivel de stop loss que se ajusta dinámicamente a medida que el precio se mueve, junto con un nivel de take profit, logrando un control prudente del riesgo.

Ventajas

- Aprovecha la fuerte tendencia de las Bandas de Bollinger a revertir hacia la media, capturando tendencias de medio a largo plazo.

- Las señales de compra y venta son claras y fáciles de ejecutar.

- Implementa un stop loss dinámico con deslizamiento, maximizando las ganancias bloqueadas y controlando el riesgo.

- Permite ajustar los parámetros según el mercado para adaptarse a diferentes condiciones.

Riesgos y soluciones

- En mercados laterales, las Bandas de Bollinger pueden generar múltiples señales de compra y venta, lo que puede llevar a quedar atrapado. La solución es establecer niveles de stop loss razonables para limitar la pérdida por operación.

- Una configuración inadecuada de los parámetros puede reducir la tasa de aciertos. La solución es optimizar los parámetros de forma razonable según el instrumento.

Direcciones de optimización

- Optimizar el período de la media móvil para adaptarlo a las características del instrumento.

- Agregar un filtro de tendencia para evitar mercados laterales.

- Combinar con otros indicadores como filtro para mejorar la estabilidad de la estrategia.

Resumen

Esta estrategia aprovecha la propiedad de reversión a la media de las Bandas de Bollinger, combinada con un stop loss dinámico con deslizamiento, para obtener ganancias de tendencias de medio a largo plazo con control de riesgo. Es una estrategia cuantitativa adaptable y de alta estabilidad. Mediante la optimización de parámetros y reglas, puede adaptarse a más instrumentos y generar rendimientos estables en operaciones en vivo.

/*backtest

start: 2024-01-24 00:00:00

end: 2024-01-31 00:00:00

period: 30m

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(shorttitle="BB Strategy", title="Bollinger Bands Strategy", overlay=true)

length = input.int(20, minval=1, group = "Bollinger Bands")

maType = input.string("SMA", "Basis MA Type", options = ["SMA", "EMA", "SMMA (RMA)", "WMA", "VWMA"], group = "Bollinger Bands")- 1