Estrategia Momentum Squeeze de Lazy Bear

Resumen

La estrategia de compresión de momento del oso perezoso es una estrategia de trading cuantitativa que combina las Bandas de Bollinger, los Canales Keltner y el indicador de momento. Utiliza las Bandas de Bollinger y los Canales Keltner para determinar si el mercado se encuentra en un estado de compresión y luego combina el indicador de momento para generar señales de trading.

La principal ventaja de esta estrategia es que puede identificar automáticamente el inicio de tendencias direccionales y determinar el momento de entrada junto con el indicador de momento. Sin embargo, también presenta ciertos riesgos y requiere optimización de parámetros para diferentes instrumentos.

Principio de la estrategia

La estrategia de compresión de momento del oso perezoso se basa en los siguientes tres indicadores:

- Bandas de Bollinger: contienen una banda media, una banda superior y una banda inferior.

- Canales Keltner: contienen un canal medio, un canal superior y un canal inferior.

- Indicador de Momento: la diferencia entre el precio actual y el precio de hace n días.

Cuando la banda superior de Bollinger esté por debajo del canal superior de Keltner y la banda inferior de Bollinger esté por encima del canal inferior de Keltner, consideramos que el mercado está en estado de compresión. Esto generalmente significa que un movimiento direccional está a punto de comenzar.

Para determinar el momento de entrada, utilizamos el indicador de momento para medir la velocidad del cambio de precio. Cuando el momento rompe al alza su media, se genera una señal de compra; cuando el momento rompe a la baja su media, se genera una señal de venta.

Análisis de ventajas de la estrategia

Las principales ventajas de la estrategia de compresión de momento del oso perezoso son:

- Puede identificar automáticamente el momento de inicio de una tendencia, permitiendo entrar temprano.

- Combina múltiples indicadores para evitar señales falsas.

- Considera tanto operaciones de tendencia como de reversión.

- Parámetros personalizables para optimización según diferentes instrumentos.

Análisis de riesgos

La estrategia de compresión de momento del oso perezoso también conlleva ciertos riesgos:

- Las Bandas de Bollinger y los Canales Keltner tienen una probabilidad relativamente alta de generar señales falsas.

- El indicador de momento puede ser inestable y puede perder el punto de entrada óptimo.

- Se requiere optimización de parámetros, de lo contrario el rendimiento es deficiente.

- La efectividad depende en gran medida del instrumento negociado.

Para reducir el riesgo, se recomienda optimizar los parámetros de longitud de las Bandas de Bollinger y los Canales Keltner, ajustar los niveles de stop loss, elegir instrumentos con buena liquidez y verificar con otros indicadores.

Direcciones de optimización de la estrategia

Para mejorar aún más el efecto de la estrategia de compresión de momento del oso perezoso, las principales direcciones de optimización son:

- Probar combinaciones de parámetros para diferentes instrumentos y marcos de tiempo.

- Optimizar la longitud de las Bandas de Bollinger y los Canales Keltner.

- Optimizar la longitud del indicador de momento.

- Establecer diferentes estrategias de stop loss y take profit para posiciones largas y cortas.

- Agregar otros indicadores para verificar las señales.

Mediante pruebas y optimización integrales, se puede mejorar significativamente la tasa de aciertos y la rentabilidad de esta estrategia.

Resumen

La estrategia de compresión de momento del oso perezoso integra múltiples indicadores con un fuerte poder de juicio y puede identificar eficazmente el momento de inicio de una tendencia. Sin embargo, también conlleva ciertos riesgos y requiere optimización de parámetros para diferentes instrumentos de trading. Mediante pruebas y optimización continuas, esta estrategia puede convertirse en un sistema de trading algorítmico eficiente.

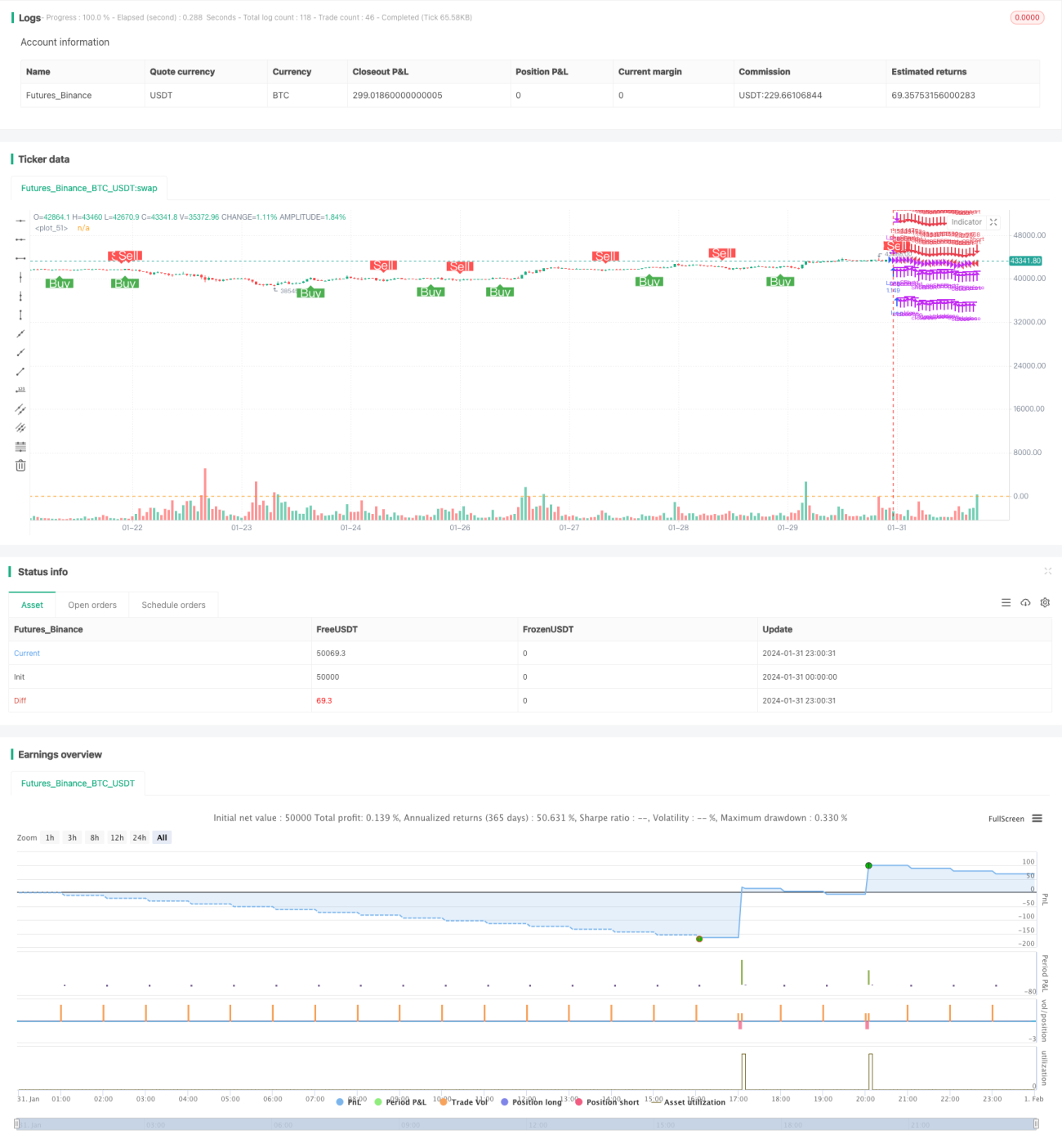

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1