Stratégie arc-en-ciel de moyenne mobile pour trading automatique complet

Aperçu

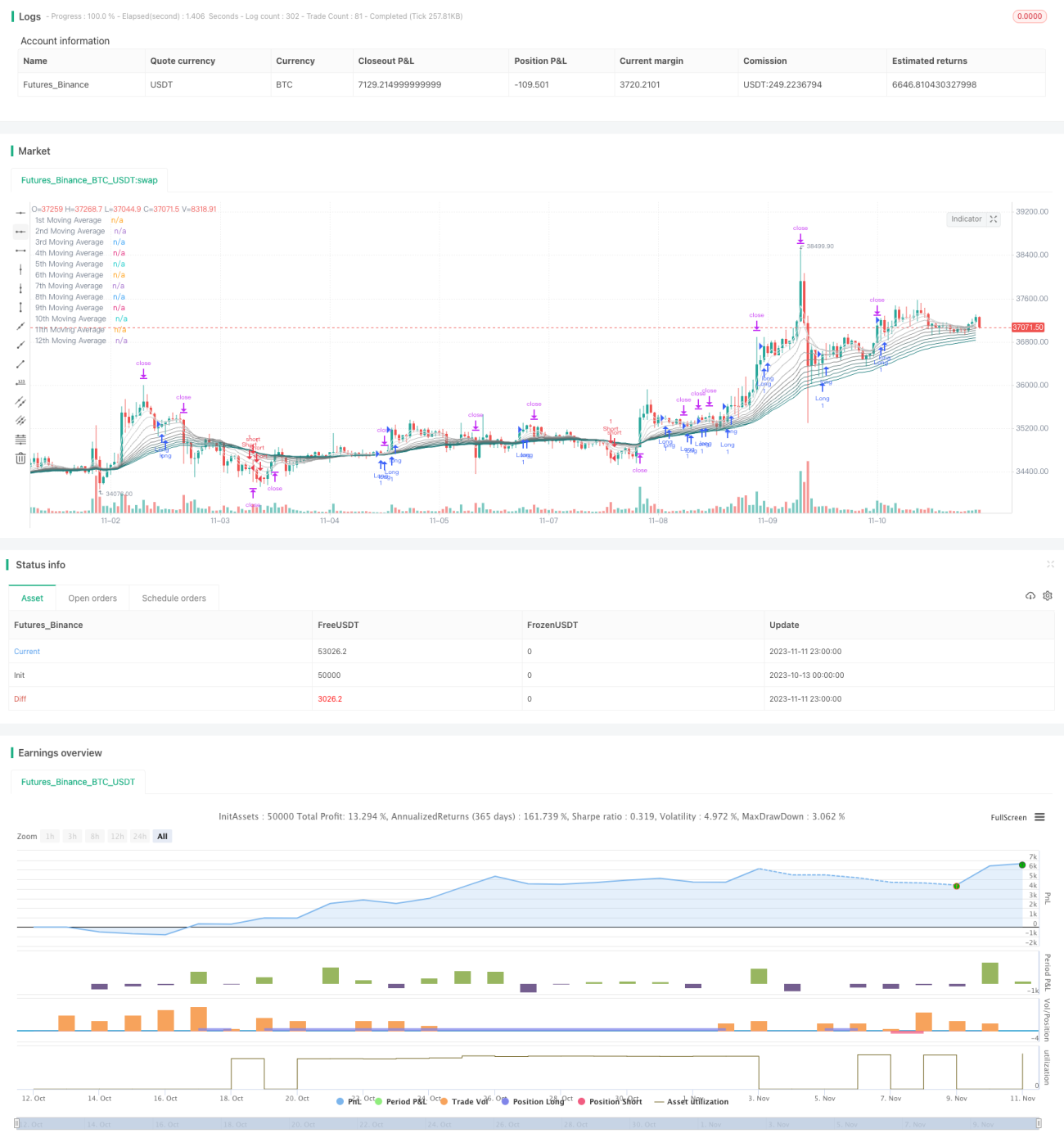

La stratégie Rainbow des Moyennes Mobiles Automatisées Intégrales est une stratégie typique de combinaison de moyennes mobiles sur plusieurs périodes. Elle utilise 12 moyennes mobiles de différentes périodes, et détermine la direction du marché ainsi que les conditions d'ouverture, de stop-loss et de take-profit en fonction de l'ordre des moyennes mobiles et de leur relation avec le prix, permettant ainsi un trading automatisé. Cette stratégie peut identifier automatiquement les tendances et dispose d'un mécanisme de stop-loss solide pour contrôler les risques.

Principe

La stratégie utilise 12 moyennes mobiles, allant de 3 périodes, 5 périodes, 8 périodes jusqu'à 55 périodes. Le type de moyenne mobile peut être choisi parmi EMA, SMA, RMA, etc. La stratégie évalue d'abord la relation d'ordre entre les moyennes mobiles à court terme et à long terme (lignes 1-4 et lignes 5-8). Si les lignes courtes sont au-dessus, le marché est considéré comme haussier ; si elles sont en dessous, le marché est considéré comme baissier.

En tendance haussière, si le prix dépasse la moyenne mobile correspondant au point bas précédent, un signal d'ouverture de position longue est validé. Le stop-loss est placé sur la moyenne mobile du point bas précédent, et le take-profit est fixé à 1,6 fois la distance du stop-loss. En tendance baissière, si le prix dépasse la moyenne mobile correspondant au point haut précédent, un signal d'ouverture de position courte est validé. Le stop-loss est placé sur la moyenne mobile du point haut précédent, et le take-profit est fixé à 1,6 fois la distance du stop-loss.

La stratégie dispose également d'une fonction de détection de retournement de tendance. Pendant la détention d'une position, si l'ordre des moyennes mobiles à court terme change et que le prix dépasse le plus récent point haut ou bas, la stratégie considère qu'un retournement de tendance a pu se produire. Dans ce cas, la position actuelle est fermée et une position opposée est ouverte, avec les nouveaux points haut ou bas comme niveaux de stop-loss et de take-profit.

Avantages

- La stratégie utilise une analyse multi-périodes, ce qui permet de bien juger la direction de la tendance.

- L'intégration de la vérification de l'ordre croissant ou décroissant des moyennes mobiles évite les signaux trompeurs en marché volatil.

- La stratégie dispose d'un mécanisme de stop-loss complet, permettant de contrôler efficacement le risque de chaque transaction.

- La fonction de détection de retournement de tendance permet de capter rapidement les opportunités de retournement, réduisant le risque systémique.

- Les paramètres de la stratégie sont flexibles : les périodes et les types de moyennes mobiles sont personnalisables.

- La stratégie utilise un stop-loss suiveur (trailing stop), ce qui permet de verrouiller un maximum de profits.

Risques

- Stratégie combinant plusieurs moyennes mobiles, les paramètres influencent ses performances et nécessitent des tests d'optimisation.

- En marché volatil sans tendance claire, les moyennes mobiles peuvent générer de faux signaux. Il convient d'ajuster les paramètres ou de ne pas trader temporairement.

- Il existe un certain retard, ce qui peut entraîner un risque de manquer des opportunités près des points de retournement de tendance.

- Il faut surveiller d'autres indicateurs techniques pour éviter d'ouvrir une position courte près de supports importants.

- Le risque systémique doit être surveillé ; le mécanisme de détection de retournement ne peut pas l'éliminer complètement.

- Le contrôle du drawdown nécessite des mécanismes supplémentaires, comme une gestion dynamique de la taille des positions.

Pistes d'optimisation

- Tester différents types de moyennes mobiles et paramètres pour trouver la meilleure combinaison.

- Optimiser le mécanisme de détection de retournement en définissant des conditions de déclenchement plus précises.

- Ajouter un système de gestion dynamique des positions, réduisant la taille en cas de drawdown important.

- Envisager d'intégrer des algorithmes d'apprentissage automatique pour identifier les niveaux clés à partir de grandes données.

- Combiner avec d'autres signaux d'indicateurs pour améliorer la précision des décisions.

- Créer un portefeuille multi-produits, en utilisant les corrélations faibles pour diversifier les risques.

Conclusion

La stratégie Rainbow des Moyennes Mobiles Automatisées Intégrales est globalement une stratégie de suivi de tendance solide, dotée d'une bonne capacité d'identification des tendances et de contrôle des risques. Avec une optimisation des paramètres et l'ajout d'une gestion dynamique des positions, elle peut devenir une stratégie de trading quantitatif très pratique. Cette stratégie est claire et facile à comprendre tout en offrant une certaine flexibilité, ce qui mérite une étude approfondie, une utilisation et une amélioration continue.

- 1