Stratégie de momentum de retour à la moyenne

Aperçu

La stratégie de momentum par régression moyenne est une stratégie de trading de tendance qui suit la moyenne des prix à court terme. Elle combine des indicateurs de régression moyenne et de momentum pour évaluer la tendance à moyen terme du marché.

Principe de la stratégie

La stratégie calcule d'abord la droite de régression moyenne des prix et l'écart type. Ensuite, en combinant les seuils prédéfinis Upper Threshold et Lower Threshold, elle détermine si le prix dépasse un écart type de la droite de régression moyenne. Si c'est le cas, un signal de trading est généré.

Pour un signal long, le prix doit être inférieur d'un écart type à la droite de régression moyenne, le prix de clôture doit être inférieur à la moyenne mobile SMA de période LENGTH, et supérieur à la moyenne mobile SMA de tendance (TREND SMA). Si ces trois conditions sont remplies, une position longue est ouverte. La condition de sortie est que le prix franchisse à la hausse la SMA de période LENGTH.

Pour un signal court, le prix doit être supérieur d'un écart type à la droite de régression moyenne, le prix de clôture doit être supérieur à la SMA de période LENGTH, et inférieur à la SMA de tendance. Si ces trois conditions sont remplies, une position courte est ouverte. La condition de sortie est que le prix franchisse à la baisse la SMA de période LENGTH.

La stratégie intègre également un pourcentage de profit cible (Percent Profit Target) et un pourcentage de stop loss (Percent Stop Loss) pour la gestion des gains et des pertes.

Le mode de sortie peut être choisi entre le franchissement de la moyenne mobile ou le franchissement de la régression linéaire.

Grâce à la combinaison de trades longs et courts, du filtrage de tendance et des stop-loss/take-profit, la stratégie permet de détecter et de suivre les tendances à moyen terme du marché.

Avantages de la stratégie

-

L'indicateur de régression moyenne permet d'évaluer efficacement si le prix s'écarte de la valeur centrale.

-

L'indicateur de momentum SMA filtre le bruit du marché à court terme.

-

Les trades longs et courts permettent de capter les opportunités de tendance dans les deux directions.

-

Le mécanisme de stop-loss et take-profit permet de contrôler efficacement les risques.

-

Le mode de sortie optionnel permet de s'adapter avec flexibilité aux conditions du marché.

-

Stratégie de trading de tendance complète, permettant de bien saisir les tendances à moyen terme.

Risques de la stratégie

-

L'indicateur de régression moyenne est sensible aux réglages des paramètres ; un seuil mal défini peut générer de faux signaux.

-

Dans des marchés très volatils, les stop-loss peuvent être déclenchés trop fréquemment.

-

Pendant les périodes de range, la fréquence de trading peut être trop élevée, augmentant les coûts de transaction et le risque de slippage.

-

Si la liquidité de l'instrument négocié est insuffisante, le contrôle du slippage peut être médiocre.

-

Le trading bilatéral (long et court) comporte un risque plus élevé, nécessitant une gestion de capital prudente.

Ces risques peuvent être atténués par l'optimisation des paramètres, l'ajustement des méthodes de stop-loss, et une gestion de capital appropriée.

Pistes d'optimisation de la stratégie

-

Optimiser les réglages des paramètres de la régression moyenne et du momentum pour les adapter aux caractéristiques des différents instruments.

-

Ajouter des indicateurs de détection de tendance pour améliorer la capacité à identifier les tendances.

-

Optimiser la stratégie de stop-loss pour mieux résister aux fortes fluctuations du marché.

-

Ajouter un module de gestion de position permettant d'ajuster la taille des positions en fonction des conditions du marché.

-

Ajouter davantage de modules de gestion des risques, tels que le contrôle du drawdown maximal, le suivi de la courbe de valeur nette, etc.

-

Envisager d'intégrer des méthodes d'apprentissage automatique pour optimiser automatiquement les paramètres de la stratégie.

Conclusion

En résumé, la stratégie de momentum par régression moyenne, grâce à une conception simple et efficace des indicateurs, permet de capter les retours vers la valeur moyenne à moyen terme. La stratégie présente une bonne adaptabilité et universalité, mais comporte également certains risques. Grâce à une optimisation continue et à la combinaison avec d'autres stratégies, de meilleures performances peuvent être obtenues. Dans l'ensemble, cette stratégie est assez complète et constitue une méthode de trading de tendance digne d'intérêt.

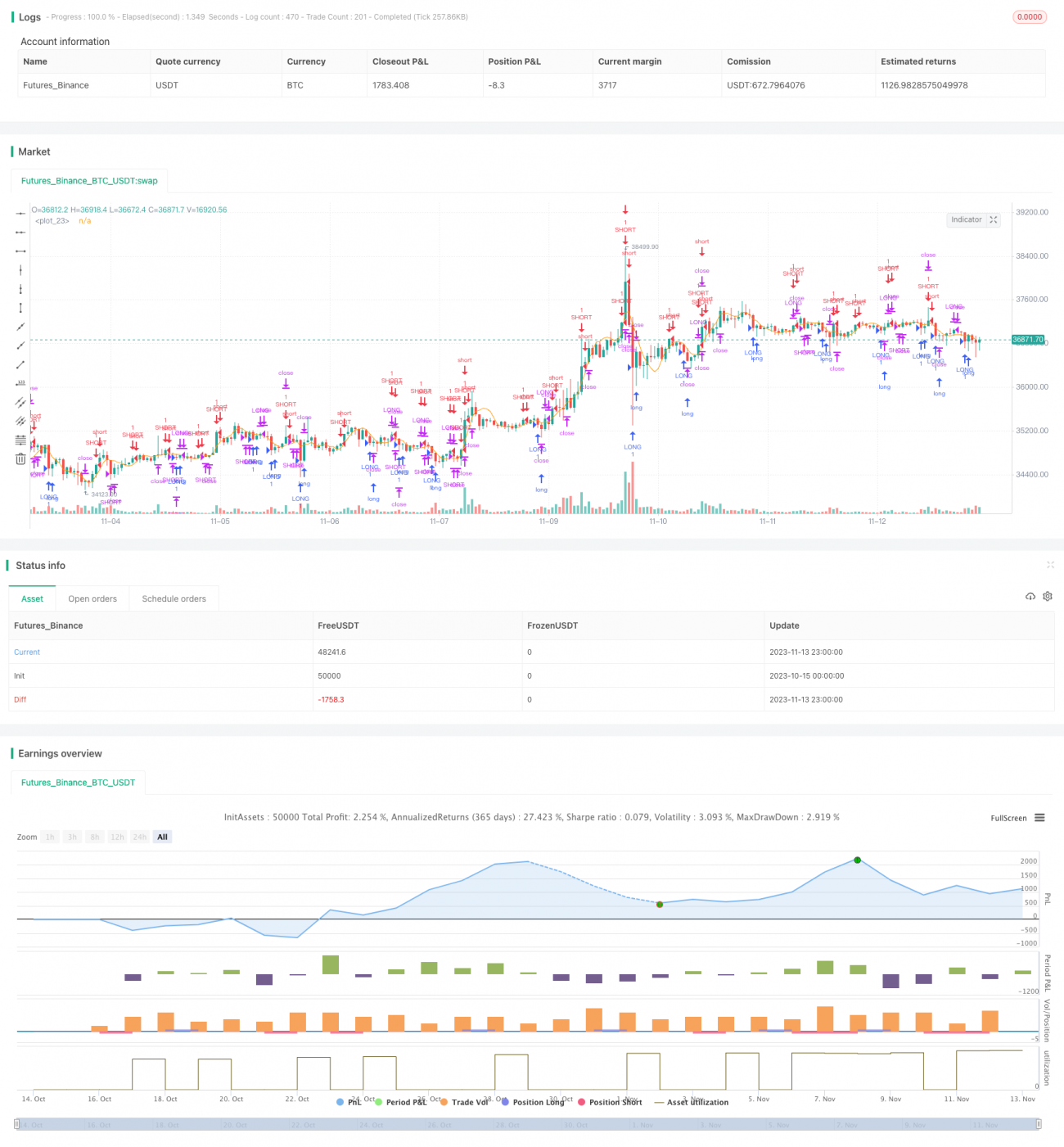

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1