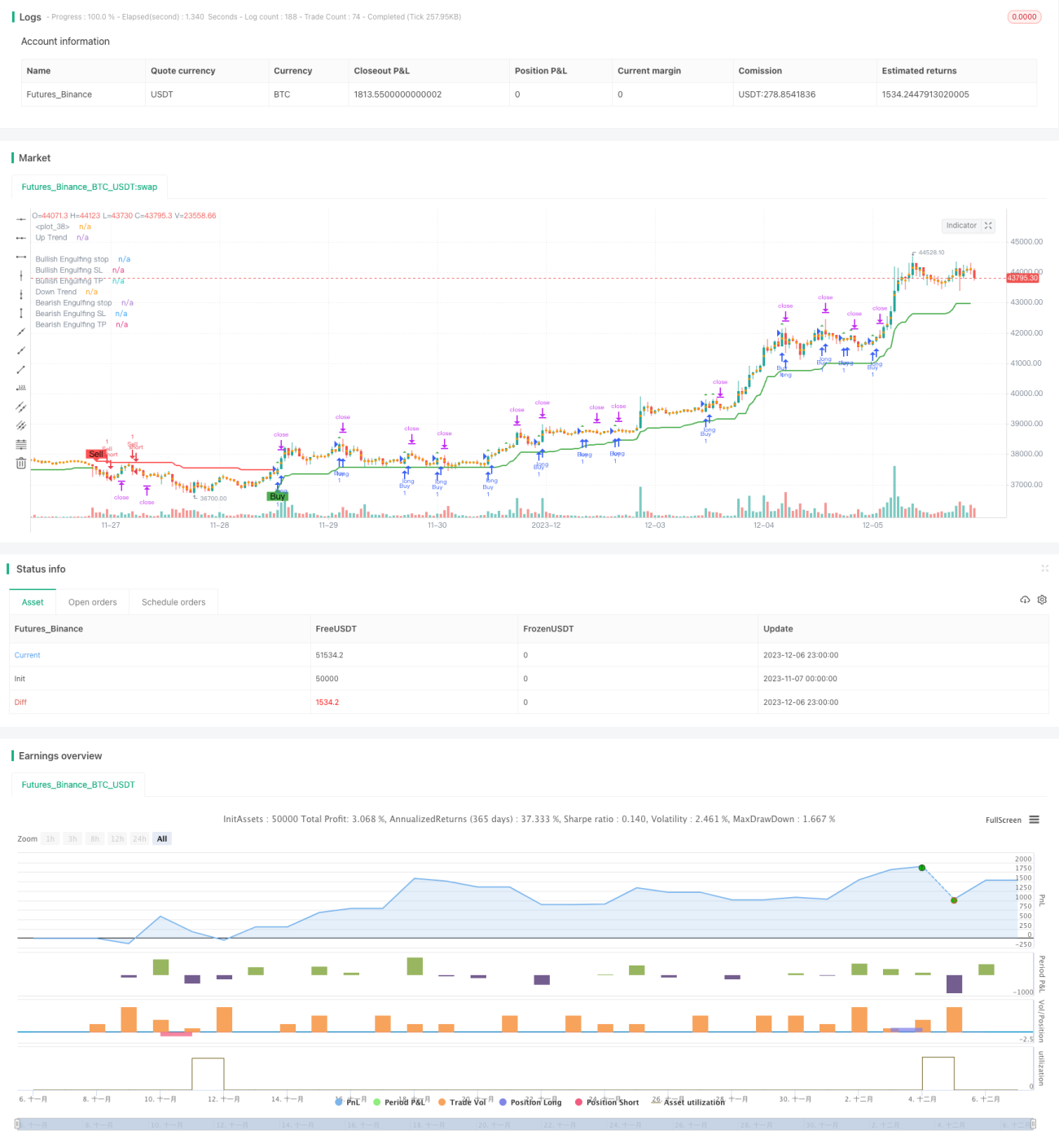

Stratégie SuperTrend Engulfing Bullet

Aperçu

La stratégie de la bougie engloutissante super-tendance est une stratégie de suivi de tendance qui combine l'Average True Range (ATR), l'indicateur super-tendance et les figures engloutissantes pour identifier la direction de la tendance, tout en recherchant des opportunités d'entrée avec un ratio avantageux lorsque la figure engloutissante confirme la tendance.

Principe de la stratégie

Cette stratégie utilise d'abord l'ATR et l'indicateur super-tendance pour déterminer la direction actuelle de la tendance du marché. Plus précisément, lorsque le prix est inférieur à la bande supérieure, on définit une tendance baissière, et lorsque le prix est supérieur à la bande inférieure, on définit une tendance haussière.

En confirmant la direction de la tendance, la stratégie vérifie également si la bougie forme une figure engloutissante. Selon la logique du code, en tendance haussière, si la clôture de la bougie précédente est supérieure à l'ouverture de la bougie actuelle et que la clôture de la bougie actuelle est inférieure à son ouverture, cela déclenche une engloutissante haussière ; en tendance baissière, si la clôture de la bougie précédente est inférieure à l'ouverture de la bougie actuelle et que la clôture de la bougie actuelle est supérieure à son ouverture, cela déclenche une engloutissante baissière.

Lorsque la figure engloutissante est alignée avec la direction de la tendance, un signal de trading est généré. De plus, la stratégie calcule un niveau de stop-loss et un niveau de take-profit basés sur la figure engloutissante. Après l'entrée, si le prix atteint le stop-loss ou le take-profit, la position est fermée.

Analyse des avantages

Cette stratégie combine les avantages du suivi de tendance et de la reconnaissance de figures, permettant d'identifier les signaux de retournement dans les marchés en tendance, et ainsi de capturer des mouvements importants aux points de retournement. De plus, le mécanisme de stop-loss permet de contrôler efficacement le risque de perte.

Analyse des risques

Le principal risque de cette stratégie réside dans la possibilité que la figure engloutissante soit un faux signal (faux breakout), générant ainsi des signaux erronés. De plus, les niveaux de stop-loss et de take-profit peuvent être trop arbitraires, empêchant d'atteindre un équilibre entre gains et pertes. Il est recommandé d'optimiser la combinaison des paramètres et d'ajuster les niveaux de stop-loss et de take-profit de manière appropriée.

Axes d'optimisation

On peut envisager d'optimiser en temps réel les paramètres de l'ATR pour mieux capturer les changements de volatilité du marché. On peut également étudier d'autres indicateurs pour identifier la tendance, afin d'améliorer encore la robustesse de la stratégie. En ce qui concerne le stop-loss et le take-profit, un trailing stop dynamique constitue également une piste d'optimisation envisageable.

Conclusion

La stratégie de la bougie engloutissante super-tendance intègre les avantages du suivi de tendance et de la reconnaissance de figures, et exploite les figures engloutissantes comme signaux de retournement, permettant d'obtenir des gains élevés aux points de retournement du marché. Cependant, cette stratégie présente également un certain risque de faux signaux, nécessitant des tests et des optimisations supplémentaires pour maîtriser le risque.

- 1