Stratégie de suivi de tendance par momentum avec bandes de Bollinger

Aperçu

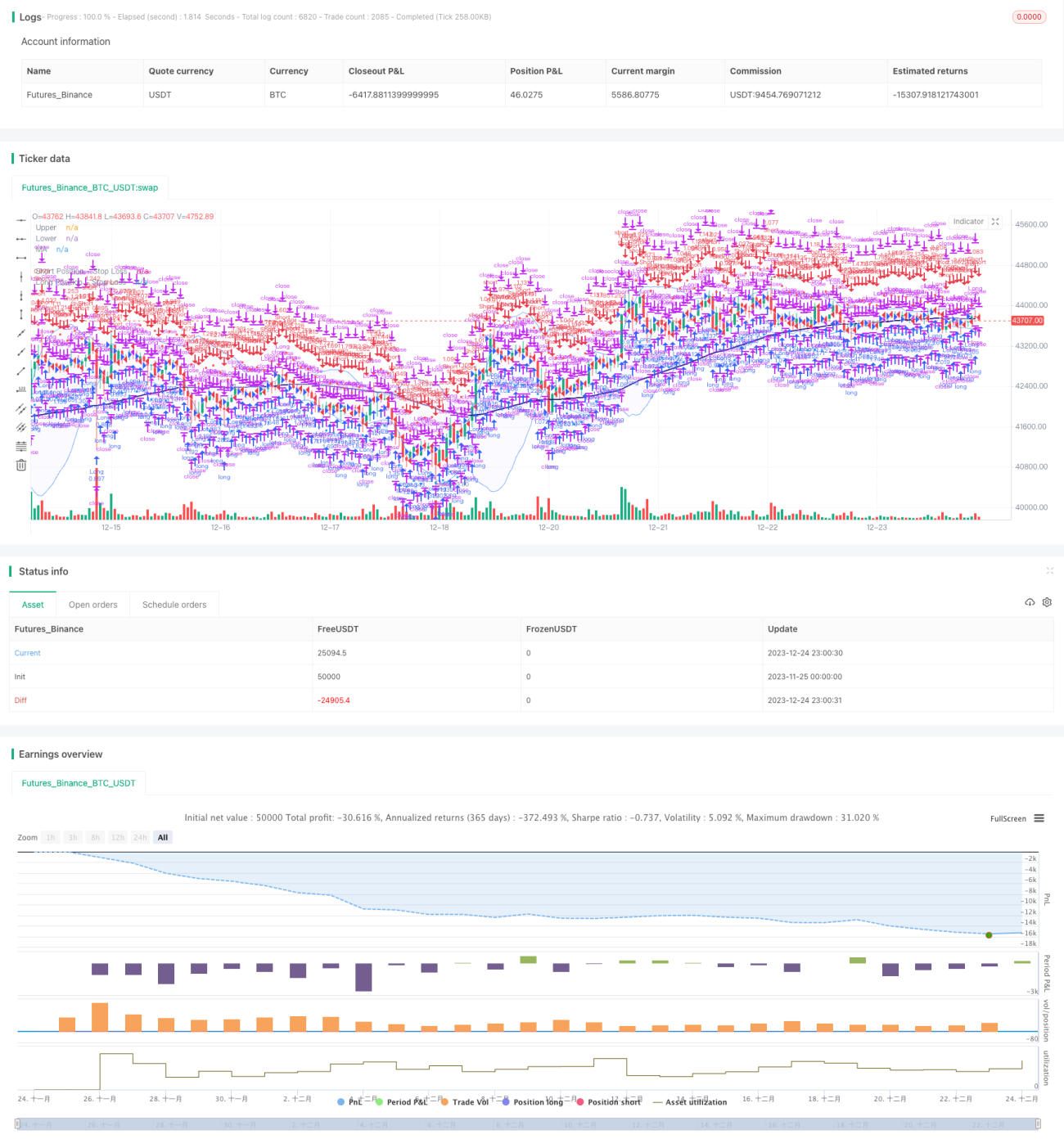

Cette stratégie met en œuvre un suivi de tendance robuste basé sur les bandes de Bollinger, les moyennes mobiles et l'analyse de volume. Elle vise à capturer les retournements de tendance potentiels et à profiter de l'élan du marché.

Principe de la stratégie

Bandes de Bollinger

-

Utilisation des bandes de Bollinger pour identifier les conditions de surachat et de survente du marché. Les bandes supérieure et inférieure offrent une visualisation claire pour faciliter la prise de décision.

-

Le principe de base des bandes de Bollinger consiste à calculer les bandes supérieure et inférieure à partir du prix médian et de l'écart type sur une période donnée. Un franchissement à la hausse de la bande supérieure est un signal de surachat, tandis qu'un franchissement à la baisse de la bande inférieure est un signal de survente.

Filtre de moyenne mobile

-

Implémentation d'un filtre de moyenne mobile pour renforcer l'identification de la tendance. L'utilisateur peut choisir différents types de moyennes mobiles, telles que la moyenne mobile simple, la moyenne mobile exponentielle et la moyenne mobile pondérée.

-

Un signal d'achat (vente) est généré lorsque le prix franchit à la hausse (baisse) la moyenne mobile.

Analyse de volume

-

Permet à l'utilisateur d'intégrer l'analyse de volume dans la stratégie pour confirmer les signaux. Les barres de volume de différentes couleurs indiquent si le volume est supérieur ou inférieur à la moyenne.

-

Un volume dépassant la ligne moyenne peut être utilisé pour confirmer les signaux de prix.

Analyse des avantages

Stratégie de suivi de tendance robuste

-

Identification des retournements de tendance du marché basée sur les bandes de Bollinger, les moyennes mobiles et le volume.

-

Capacité à capturer rapidement la tendance des prix et à en tirer profit.

Flexibilité et personnalisation

-

L'utilisateur peut choisir les paramètres des bandes de Bollinger, le type et la longueur de la moyenne mobile pour optimiser.

-

Les positions longues et courtes peuvent être contrôlées séparément.

Visualisation et confirmation

-

Double mécanisme de confirmation : les signaux de prix des bandes de Bollinger sont confirmés par la moyenne mobile et le volume.

-

Affichage intuitif des signaux de trading tels que la moyenne mobile et le niveau stop-loss.

Gestion des risques

-

Calcul du stop-loss basé sur l'ATR. Personnalisation possible de la période ATR et du multiple ATR pour le stop.

-

Ajustement de la taille de la position en fonction du pourcentage de risque de la position. Contrôle efficace des pertes individuelles.

Analyse des risques

Risque lié à la période de backtest

- Différentes périodes historiques peuvent affecter les performances de la stratégie. Il convient de réaliser des backtests sur différentes périodes pour garantir sa robustesse.

Risque de retournement de tendance

- Dans les marchés en range, les stop-loss peuvent être fréquemment déclenchés. Ce risque peut être réduit en optimisant les paramètres de la moyenne mobile.

Risque de suroptimisation

- L'optimisation de multiples paramètres peut conduire à un surajustement. Utiliser différentes combinaisons de paramètres et effectuer des tests de robustesse.

Risque de retard des indicateurs techniques

- Les indicateurs présentent un certain retard. Les décisions doivent tenir compte de l'évolution réelle des prix, sans se fier uniquement aux indicateurs.

Pistes d'optimisation

Optimisation des paramètres

- Optimiser les paramètres des bandes de Bollinger, le type de moyenne mobile et les paramètres ATR pour différentes classes d'actifs et périodes.

Optimisation de la taille des positions

- Tester différents pourcentages de risque par position et optimiser le multiple du stop-loss.

Optimisation des signaux

- Tester l'ajout d'autres indicateurs auxiliaires pour filtrer les signaux, comme le KD, le MACD, etc.

Optimisation du code

- Optimiser la logique de génération des signaux pour réduire les ouvertures inutiles. Utiliser la programmation orientée objet pour améliorer l'extensibilité.

Conclusion

Cette stratégie intègre les bandes de Bollinger, les moyennes mobiles et l'analyse de volume pour construire un système de trading mécanique de suivi de tendance. Ses atouts résident dans un mécanisme de confirmation de signaux puissant et un contrôle des risques efficace. Par la suite, l'optimisation des paramètres et des signaux peut améliorer la stabilité et la rentabilité de la stratégie. Cette stratégie peut servir de référence méthodologique pour les investisseurs cherchant à suivre les tendances.

- 1