Stratégie de tendance à double EMA avec croisements dorés et mortels

1

Follow

1802

Followers

Aperçu

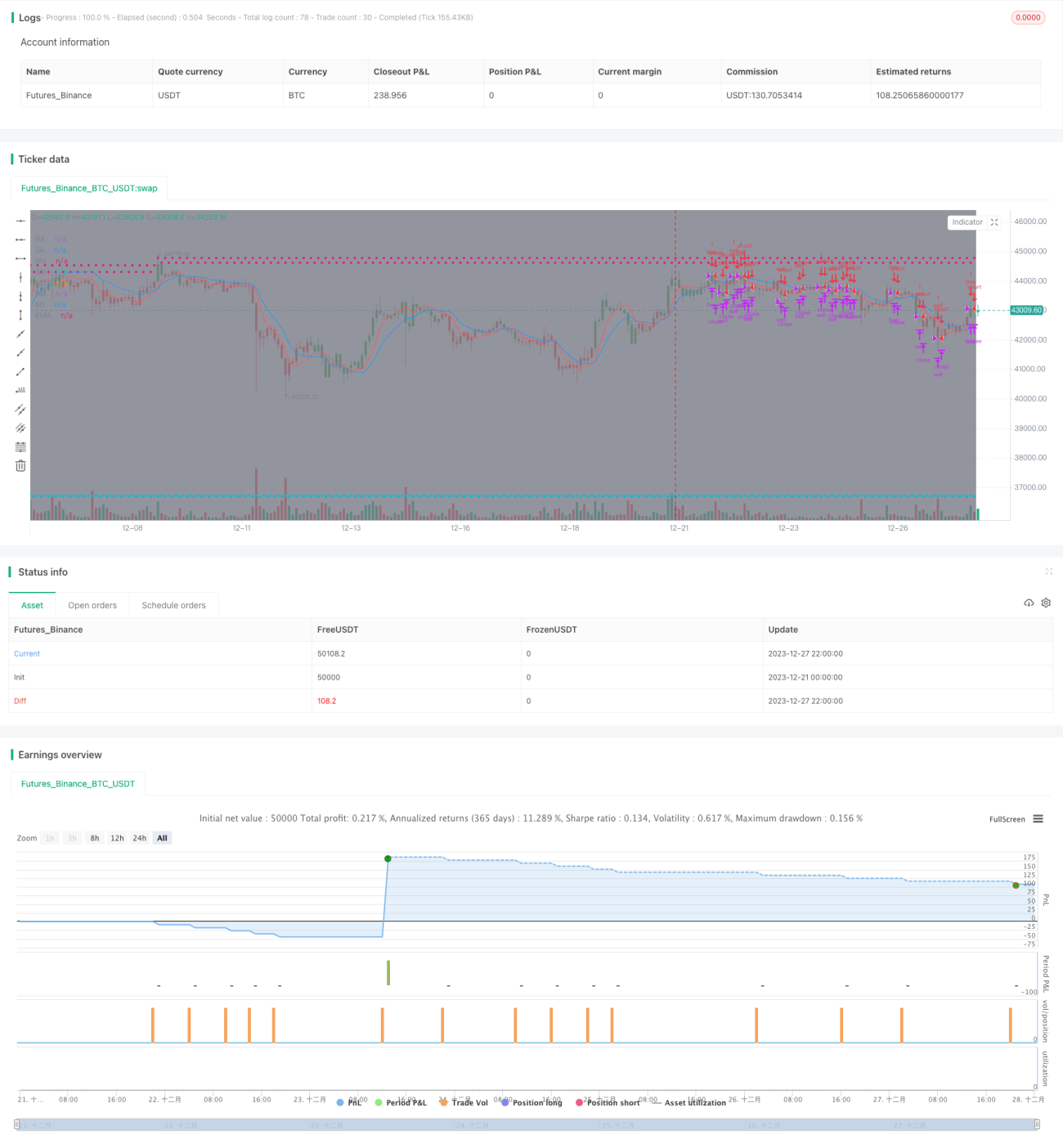

Cette stratégie utilise le croisement doré et le croisement mortel de la double EMA pour déterminer la direction actuelle de la tendance, et combine l’indicateur RSI pour éviter de manquer des opportunités d’achat ou de vente. Il s’agit d’une stratégie typique de suivi de tendance.

Principe de la stratégie

- Calculer les moyennes mobiles EMA sur 10 et 20 périodes, nommées respectivement ma00 et ma01.

- Lorsque ma00 passe au-dessus de ma01, un signal d’achat est généré.

- Lorsque ma00 passe en dessous de ma01, un signal de vente est généré.

- Simultanément, lorsque le prix passe au-dessus de ma00, si ma00 est supérieur à ma01, cela génère également un signal d’achat.

- De même, lorsque le prix passe en dessous de ma00, si ma00 est inférieur à ma01, cela génère également un signal de vente.

- Grâce à cette double vérification, il est possible d’éviter de manquer certains points d’entrée ou de sortie.

- Définir des niveaux de stop-loss et de take-profit pour gérer les risques.

Analyse des avantages

- L’utilisation d’une double EMA permet de filtrer efficacement les faux dépassements.

- La double condition empêche de manquer des ordres.

- Les niveaux de stop-loss et de take-profit aident à contrôler les risques.

Analyse des risques

- Cette stratégie basée sur la double EMA est une stratégie de suivi de tendance ; en période de range, les signaux d’achat/vente sont fréquents et le stop-loss risque d’être souvent déclenché.

- Elle ne permet pas de détecter précisément les points de retournement de tendance, ce qui peut entraîner des pertes.

- Un mauvais réglage du stop-loss peut amplifier les pertes.

Pistes d’optimisation

- Il est possible d’optimiser la période des EMA pour trouver la meilleure combinaison de paramètres.

- Ajouter d’autres indicateurs pour améliorer la stabilité de la stratégie.

- Mettre en place un stop-loss dynamique, ajustant le point de sortie en fonction de la volatilité du marché.

Source

Pine

/*backtest

start: 2023-12-21 00:00:00

end: 2023-12-28 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title='[STRATEGY][RS]MicuRobert EMA cross V1', shorttitle='S', overlay=true, pyramiding=0, initial_capital=100000)

USE_TRADESESSION = input(title='Use Trading Session?', type=bool, defval=true)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1