Strategi Momentum Sederhana Berdasarkan SMA, EMA, dan Volume Perdagangan

Ikhtisar

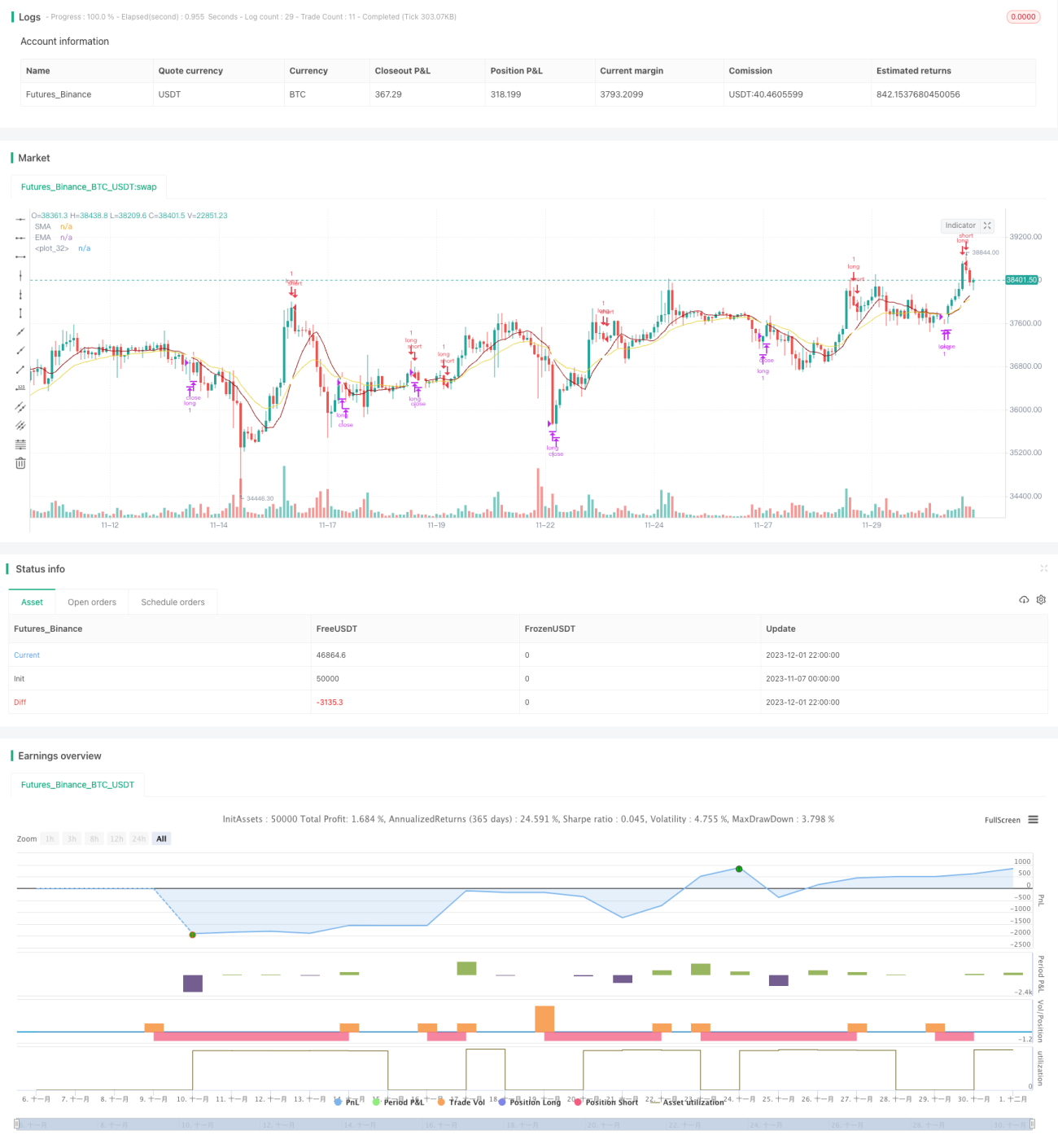

Strategi ini adalah strategi momentum intraday sederhana yang hanya mengambil posisi long (tidak short). Strategi ini memanfaatkan indikator SMA, EMA, dan volume untuk mencoba masuk pasar pada waktu yang optimal (yaitu saat harga dan momentum sama-sama naik). Keunggulannya adalah sederhana dalam implementasi dan memiliki kemampuan tertentu dalam mengidentifikasi tren.

Prinsip Strategi

Logika pembuatan sinyal Entry pada strategi ini adalah: ketika indikator SMA berada di atas indikator EMA dan terjadi tren naik selama 3 atau 4 candle berturut-turut, dan harga terendah candle di tengah lebih tinggi dari harga pembukaan candle awal kenaikan, maka sinyal Entry dihasilkan.

Logika pembuatan sinyal Exit adalah: ketika indikator SMA memotong ke bawah indikator EMA, maka sinyal Exit dihasilkan.

Strategi ini hanya mengambil posisi long, tidak short. Logika Entry dan Exit-nya memiliki kemampuan tertentu dalam mengidentifikasi tren naik yang berkelanjutan.

Analisis Keunggulan

Strategi ini memiliki keunggulan sebagai berikut:

-

Logika strategi sederhana, mudah dipahami dan diimplementasikan;

-

Menggunakan indikator teknis umum seperti SMA, EMA, dan volume, parameter dapat disesuaikan secara fleksibel;

-

Memiliki kemampuan tertentu dalam mengidentifikasi tren naik yang berkelanjutan, sehingga dapat menangkap sebagian peluang dalam tren.

Analisis Risiko

Strategi ini juga memiliki risiko sebagai berikut:

-

Tidak dapat mengidentifikasi pasar yang sedang turun atau sideways, sehingga berpotensi menyebabkan drawdown yang besar;

-

Tidak dapat memanfaatkan peluang short, sehingga tidak bisa melakukan lindung nilai terhadap tren menurun, dan mungkin melewatkan peluang profit yang baik;

-

Indikator volume kurang efektif untuk data frekuensi tinggi, perlu penyesuaian parameter;

-

Stop loss dapat digunakan untuk mengendalikan risiko.

Arah Optimasi

Strategi ini dapat dioptimasi dari beberapa aspek berikut:

-

Menambahkan peluang trading short, sehingga dapat melakukan perdagangan dua arah (long dan short), memanfaatkan tren menurun untuk arbitrase;

-

Menggunakan indikator yang lebih canggih seperti MACD, RSI, dan kombinasinya untuk meningkatkan kemampuan dalam mengidentifikasi tren;

-

Mengoptimalkan logika stop loss untuk mengurangi risiko drawdown;

-

Menyesuaikan parameter, menguji data pada periode yang berbeda, untuk menemukan kombinasi parameter terbaik.

Kesimpulan

Secara keseluruhan, strategi ini merupakan strategi pelacakan tren yang sangat sederhana, yang menentukan waktu masuk melalui indikator SMA, EMA, dan volume. Keunggulannya adalah kesederhanaan dan kemudahan implementasi, cocok untuk pembelajaran awal. Namun, strategi ini tidak dapat mengidentifikasi tren sideways dan menurun, sehingga memiliki risiko tertentu. Perbaikan dapat diperoleh dengan memperkenalkan posisi short, mengoptimalkan indikator, dan stop loss.

- 1