Strategi Momentum Squeeze Beruang Malas

Ikhtisar

Strategi Momentum Squeeze Beruang Malas adalah strategi trading kuantitatif yang menggabungkan Bollinger Bands, Keltner Channels, dan indikator momentum. Strategi ini menggunakan Bollinger Bands dan Keltner Channels untuk menilai apakah pasar saat ini berada dalam kondisi squeeze, kemudian menggabungkannya dengan indikator momentum untuk menghasilkan sinyal trading.

Keunggulan utama strategi ini adalah dapat secara otomatis mengidentifikasi awal dari tren pasar, dan bersama dengan indikator momentum menentukan waktu entry. Namun, strategi ini juga memiliki risiko tertentu, sehingga perlu optimasi parameter untuk berbagai instrumen.

Prinsip Strategi

Strategi Momentum Squeeze Beruang Malas didasarkan pada tiga indikator berikut:

- Bollinger Bands: terdiri dari garis tengah, garis atas, dan garis bawah

- Keltner Channels: terdiri dari garis tengah, garis atas, dan garis bawah

- Indikator Momentum: selisih antara harga saat ini dengan harga n hari yang lalu

Ketika garis atas Bollinger Bands lebih rendah dari garis atas Keltner Channels, dan garis bawah Bollinger Bands lebih tinggi dari garis bawah Keltner Channels, kita menganggap pasar berada dalam kondisi squeeze. Ini biasanya menandakan bahwa tren pasar akan segera dimulai.

Untuk menentukan waktu entry, kita menggunakan indikator momentum untuk menilai kecepatan perubahan harga. Ketika momentum menembus rata-ratanya ke atas, sinyal beli dihasilkan; ketika momentum menembus rata-ratanya ke bawah, sinyal jual dihasilkan.

Analisis Keunggulan Strategi

Keunggulan utama strategi Momentum Squeeze Beruang Malas adalah:

- Dapat secara otomatis mengidentifikasi waktu dimulainya tren dan masuk lebih awal

- Menggabungkan berbagai indikator untuk penilaian, menghindari sinyal palsu

- Mengakomodasi baik trading tren maupun pembalikan

- Parameter dapat disesuaikan untuk optimasi pada berbagai instrumen

Analisis Risiko

Strategi Momentum Squeeze Beruang Malas juga memiliki risiko tertentu:

- Probabilitas sinyal palsu dari Bollinger Bands dan Keltner Channels cukup tinggi

- Indikator momentum tidak stabil, mungkin melewatkan titik entry terbaik

- Perlu optimasi parameter, jika tidak hasilnya kurang optimal

- Efektivitas sangat bergantung pada instrumen trading

Untuk mengurangi risiko, disarankan untuk mengoptimalkan parameter panjang Bollinger Bands dan Keltner Channels, menyesuaikan level stop loss, memilih instrumen trading dengan likuiditas yang baik, serta memverifikasi dengan indikator lain.

Arah Optimasi Strategi

Untuk lebih meningkatkan efektivitas strategi Momentum Squeeze Beruang Malas, arah optimasi utama meliputi:

- Menguji kombinasi parameter untuk berbagai instrumen dan periode

- Mengoptimasi panjang Bollinger Bands dan Keltner Channels

- Mengoptimasi panjang indikator momentum

- Merumuskan strategi stop loss dan take profit yang berbeda untuk posisi long dan short

- Menambahkan indikator lain untuk verifikasi sinyal

Melalui pengujian dan optimasi dari berbagai sisi, tingkat kemenangan dan profitabilitas strategi ini dapat ditingkatkan secara signifikan.

Kesimpulan

Strategi Momentum Squeeze Beruang Malas mengintegrasikan berbagai indikator dengan kemampuan penilaian yang kuat, dapat secara efektif mengidentifikasi awal tren. Namun, juga memiliki risiko tertentu, sehingga perlu optimasi parameter untuk berbagai instrumen trading. Melalui pengujian dan optimasi berkelanjutan, strategi ini dapat menjadi sistem trading algoritmik yang efisien.

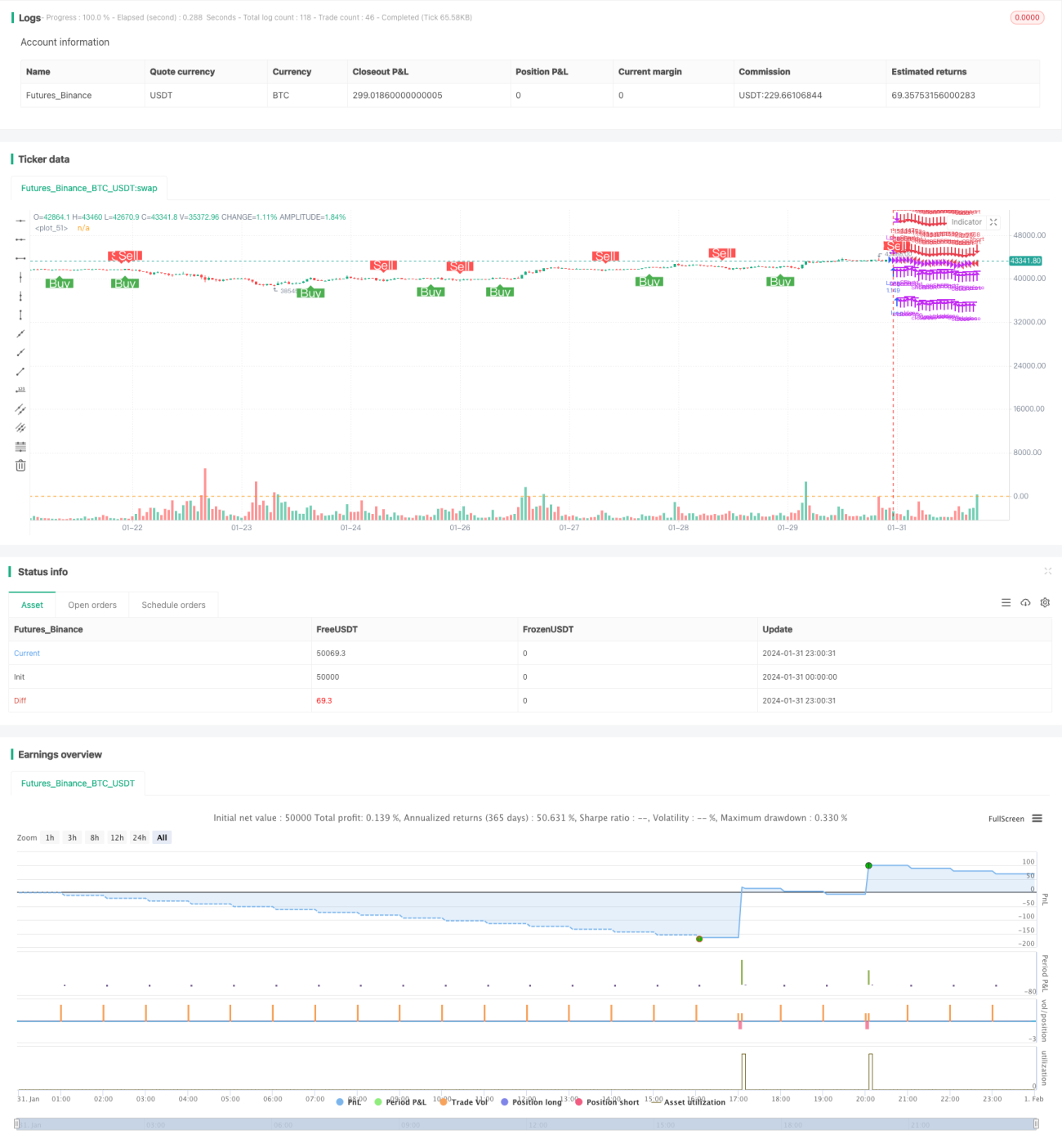

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1