平均回帰モメンタム戦略

概要

平均回帰モメンタム戦略は、短期価格平均を追跡するトレンド取引戦略です。平均回帰指標とモメンタム指標を組み合わせることで、市場の中期的なトレンドを判断します。

戦略の原理

この戦略はまず、価格の平均回帰線と標準偏差を計算します。次に、Upper ThresholdおよびLower Thresholdパラメータで設定された閾値を用いて、価格が平均回帰線から1標準偏差の範囲を超えているかどうかを判定します。超えた場合、取引シグナルが生成されます。

買いシグナルについては、価格が平均回帰線より1標準偏差低く、終値がLENGTH期間のSMA移動平均線より低く、かつTREND SMA移動平均線より高いという3つの条件をすべて満たした場合、買い方向のポジションをオープンします。決済条件は、価格がLENGTH期間のSMA移動平均線を上抜けることです。

売りシグナルについては、価格が平均回帰線より1標準偏差高く、終値がLENGTH期間のSMA移動平均線より高く、かつTREND SMA移動平均線より低いという3つの条件をすべて満たした場合、売り方向のポジションをオープンします。決済条件は、価格がLENGTH期間のSMA移動平均線を下抜けることです。

この戦略は同時に、Percent Profit Target(利益確定率)とPercent Stop Loss(損切り率)を組み合わせて、利確・損切りの管理を行います。

Exit方式は、移動平均線のブレイクアウトまたは線形回帰のブレイクアウトを選択できます。

買いと売りの両面取引、トレンドフィルター、利確・損切りなどの組み合わせにより、市場の中期的なトレンドの判断と追跡を実現します。

戦略の利点

-

平均回帰指標は、価格が価値の中心から逸脱しているかどうかを効果的に判断できます。

-

モメンタム指標であるSMAは、短期的な市場ノイズを除去できます。

-

買いと売りの両面取引により、トレンド機会を全方位的に捉えることができます。

-

利確・損切りメカニズムにより、リスクを効果的にコントロールできます。

-

選択可能なExit方式により、市場環境に柔軟に対応できます。

-

完全なトレンド取引戦略であり、中期トレンドをうまく捉えることができます。

戦略のリスク

-

平均回帰指標はパラメータ設定に敏感であり、閾値の設定が不適切だと偽のシグナルが発生する可能性があります。

-

大幅な値動きの相場では、損切りが頻発する場合があります。

-

レンジ相場では取引頻度が高くなり、取引コストやスリッページリスクが増加する可能性があります。

-

取引対象の流動性が低い場合、スリッページのコントロールが思わしくないことがあります。

-

買いと売りの両面取引はリスクが大きいため、慎重な資金管理が必要です。

これらのリスクは、パラメータの最適化、損切り方法の調整、資金管理などの方法でコントロールできます。

戦略の最適化方向

-

平均回帰とモメンタム指標のパラメータ設定を最適化し、異なる銘柄の特性に合わせる。

-

トレンド判断指標を追加し、トレンド認識能力を高める。

-

損切り戦略を最適化し、市場の大幅な変動に対応できるようにする。

-

ポジション管理モジュールを追加し、市場状況に応じてポジションサイズを調整する。

-

最大ドローダウン制御、純資産曲線制御など、より多くのリスク管理モジュールを追加する。

-

機械学習手法を組み合わせ、戦略パラメータを自動最適化することを検討する。

まとめ

以上のように、平均回帰モメンタム戦略は、シンプルで効果的な指標設計により、中期的な価値回帰トレンドを捉えることを実現します。この戦略は適応性と汎用性が高い一方で、一定のリスクも存在します。継続的な最適化や他の戦略との組み合わせにより、より良いパフォーマンスを得ることができます。この戦略は全体的に完成度が高く、検討に値するトレンド取引手法です。

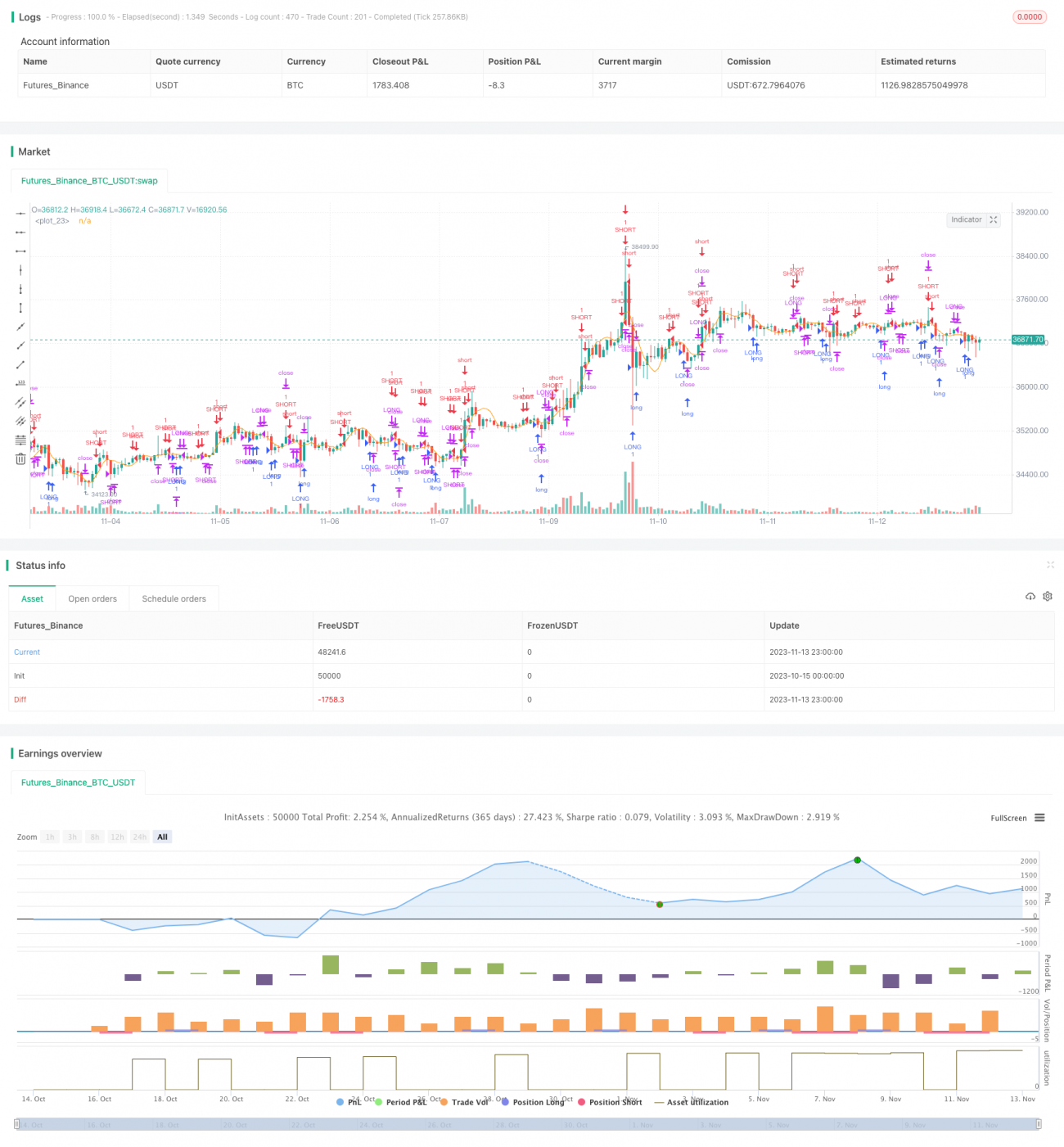

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1