1

Follow

1802

Followers

概要

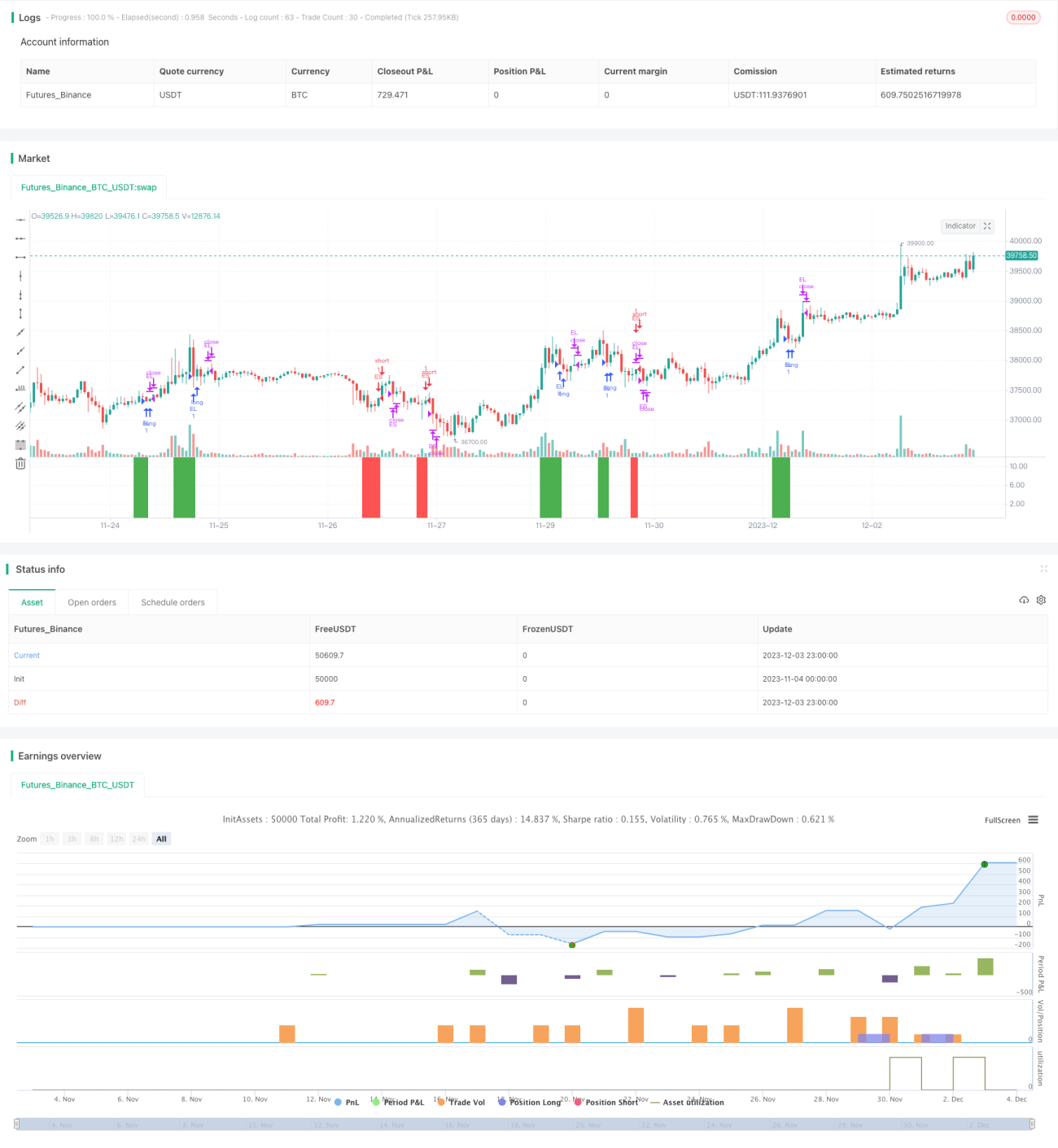

本戦略は、価格が8日連続で5日単純移動平均線を上回るまたは下回った後に反転する特性を利用し、中短期のモメンタム効果を捉えます。価格が8日連続で5日線を下回った後、最初の日の終値が再び5日線を上抜けたときに買い建てます。価格が8日連続で5日線を上回った後、最初の日の終値が再び5日線を下抜けたときに売り建てます。

戦略の原理

- 5日単純移動平均線(SMA)を計算します。

- 強気トレンドTrendUpを終値がSMA以上、弱気トレンドTrendDownを終値がSMA以下と定義します。

- トレンド反転の条件:8日連続で終値がSMAを下回った後、翌日の終値が強気(SMAを上抜け)になったときに買いシグナルが発生します。8日連続で終値がSMAを上回った後、翌日の終値が弱気(SMAを下抜け)になったときに売りシグナルが発生します。

- エントリー:買い条件Buyは、前日に買いシグナルTriggerBuyが発生し、現在が弱気トレンドの場合に買い建てます。売り条件Sellは、前日に売りシグナルTriggerSellが発生し、現在が強気トレンドの場合に売り建てます。

- エグジット:買いポジションのストップは終値がSMAを下抜けたときに手仕舞い。売りポジションのストップは終値がSMAを上抜けたときに手仕舞い。

優位性分析

- 価格反転の特性を利用し、中短期のモメンタムを捉えるのに適しています。

- 8日連続でSMAを突破してトレンドが形成されるケースが多く、取引機会が増えます。

- 5日線のパラメータが適切で、偽のブレイクアウトに惑わされるのを防ぎます。

- リスクが管理可能で、明確なストップポイントがあります。

リスク分析

- 相場がもみ合う場合、ストップポイントが頻繁にトリガーされる可能性があります。

- ブレイクアウト継続日数を長く設定しすぎると、最適なエントリーのタイミングを逃す可能性があります。

- 長期の一方向トレンドが発生した場合、本戦略では利益を得にくくなります。

SMAのパラメータを適宜調整し、エントリー条件を最適化して偽のブレイクアウトを防ぎ、トレンド判断指標と組み合わせることで効果を強化できます。

最適化の方向性

- パラメータ最適化:異なる期間のSMAパラメータをテストし、より良いパラメータを探します。

- エントリー最適化:出来高指標を追加して偽のブレイクアウトを回避、または陽線・陰線の判断を加えてもみ合い相場を避けます。

- エグジット最適化:終値が一定の割合で下落した後にストップをかけるなど、ストップにバッファを設けることを検討します。

- リスク管理最適化:1日のストップ回数を設定し、過度な損失を防ぎます。

- 他のインジケーターとの組み合わせ:RSIやMACDなどのトレンド判断指標を追加し、トレンドの勢いを識別します。

まとめ

本戦略は、価格の動きの状態を判断することで、中短期的な価格のブレイクアウトから反転までのプロセスを捉え、もみ合いを回避しトレンドに沿った取引を行うものです。鍵となるのは、パラメータ設定とエントリー判断を厳格に行い、ノイズに惑わされないようにすること、そしてエグジットのストップを適切に設定して過大な損失を防ぐことです。さらにトレンド判断指標を補助として用いれば、より優れた効果が得られます。本戦略はロジックが明確で理解しやすく、コードも簡潔であり、研究して最適化する価値があります。

Source

Pine

Related strategies

Comment

All comments (0)

No data

- 1