SMA、EMA、および出来高に基づくシンプルなモメンタム戦略

1

Follow

1802

Followers

概要

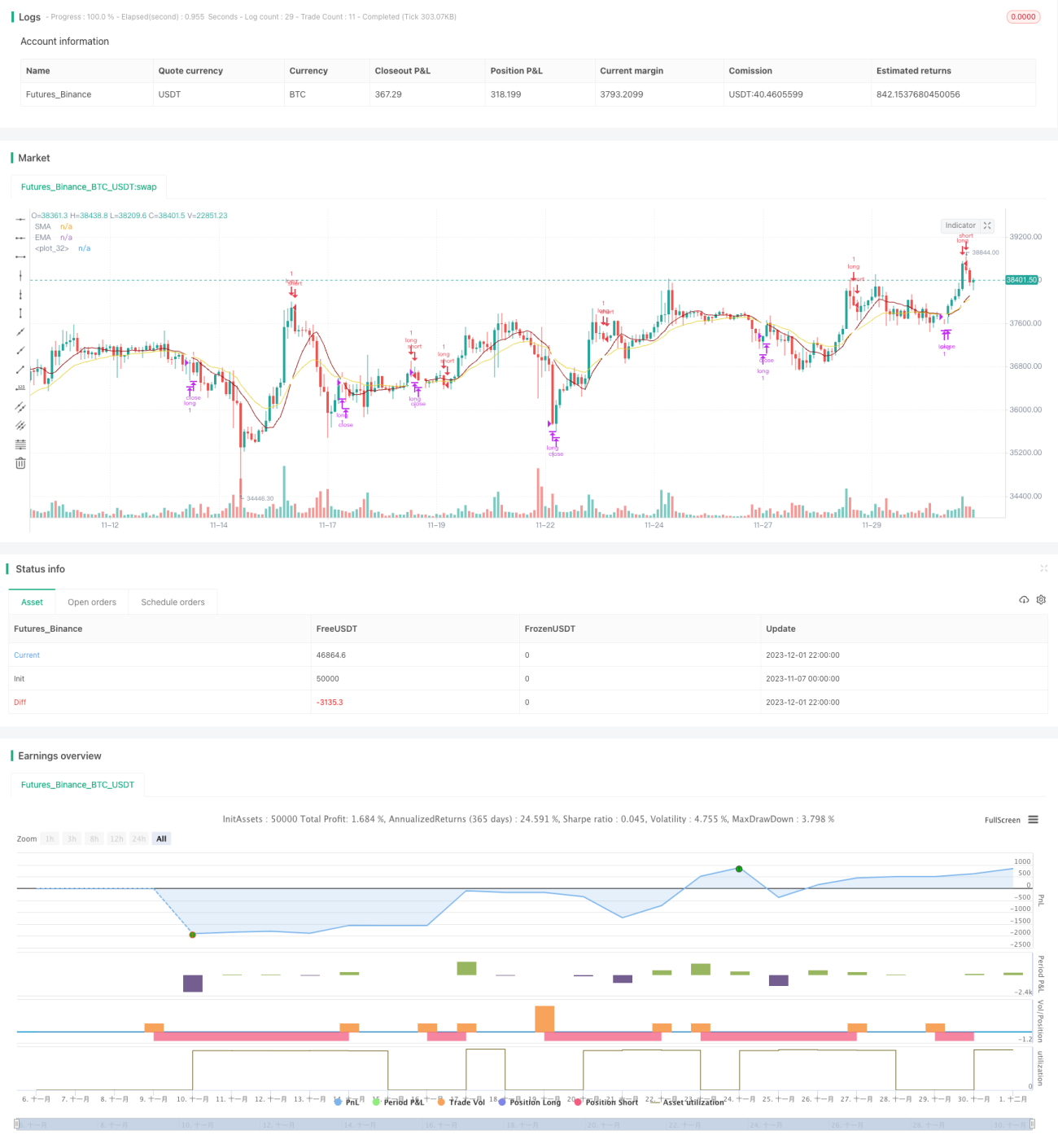

本戦略は、非空売り(ロングのみ、ショートなし)のシンプルなデイリー・モメンタム戦略です。SMA、EMA、および出来高指標を用いて、最適なタイミング(価格とモメンタムが同時に上昇する時)で市場に参入することを目指します。利点はシンプルで実装が容易であり、トレンドをある程度識別できる点です。

戦略の原理

本戦略のエントリーシグナル生成ロジックは、SMA指標がEMA指標を上回っていることと、連続する3本または4本のローソク足が上昇トレンドを形成し、かつ中間のローソク足の最安値が上昇開始ローソク足の始値よりも高い場合に、エントリーシグナルを生成します。

エグジットシグナル生成ロジックは、SMA指標がEMA指標を下回った場合にエグジットシグナルを生成します。

本戦略はロングのみでショートは行いません。そのエントリーとエグジットのロジックは、持続的な上昇トレンドをある程度識別できます。

優位性分析

本戦略には以下の優位性があります。

- 戦略ロジックがシンプルで理解と実装が容易。

- SMA、EMA、出来高などの一般的なテクニカル指標を利用しており、パラメータ調整が柔軟。

- 持続的な上昇トレンドをある程度識別でき、トレンド中の一部の機会を捉えられる。

リスク分析

本戦略には以下のリスクも存在します。

- 下落またはレンジ相場を識別できず、大きなドローダウンをもたらす可能性がある。

- ショートの機会を活用できず、衰退トレンドに対してヘッジできないため、収益機会を逃す可能性がある。

- 出来高指標は高頻度データに対して効果が低く、パラメータ調整が必要。

- ストップロスを用いてリスクを管理できる。

最適化の方向性

本戦略は以下の点から最適化が可能です。

- ショートの取引機会を追加し、ロング・ショート双方向取引を実現し、衰退トレンドを利用した裁定取引を行う。

- MACD、RSIなどのより高度な指標を組み合わせた戦略を利用し、トレンド判断能力を向上させる。

- ストップロスロジックを最適化し、ドローダウンリスクを低減する。

- パラメータを調整し、異なる期間のデータをテストし、最適なパラメータ組み合わせを探す。

まとめ

本戦略は全体的に非常にシンプルなトレンド追跡戦略であり、SMA、EMA、出来高指標を用いてエントリーのタイミングを判断します。利点はシンプルで実装が容易な点であり、初心者の学習に適していますが、レンジ相場や下降トレンドを識別できず、一定のリスクが存在します。ショートの導入、指標の最適化、ストップロスなどの手段により改善が可能です。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1