モメンタムオシレーター・ストキャスティックRSI取引戦略

概要

本稿では、Stochastic RSI指標に基づくモメンタム・オシレーション取引戦略について説明します。この戦略は、比較的短い期間(例:30分)のテクニカル指標を使用し、Stochastic RSIが買われ過ぎ・売られ過ぎの領域に達したかどうかに基づいて取引判断を行います。他のモメンタム戦略と比較して、本戦略はRSIとストキャスティクスの両方の利点を組み合わせることで、市場の短期的な振動をより正確に捉えることができます。

戦略の原理

本戦略のコア指標はStochastic RSIです。Stochastic RSI指標の計算式は以下の通りです。

Stochastic RSI = (RSI - 最低RSI) / (最高RSI - 最低RSI) * 100

ここで、RSIはlengthRSIパラメータ(デフォルト12)を使用して計算され、Stochastic RSIはlengthStochパラメータ(デフォルト12)を使用して計算されます。

Stochastic RSIが紫色の塗りつぶし領域を上回った場合、買われ過ぎゾーンとなり、ここで空売りを行います。Stochastic RSIが紫色の塗りつぶし領域を下回った場合、売られ過ぎゾーンとなり、ここで買いを行います。

さらに、本戦略は移動平均線によるフィルター条件を設定しています。短期EMAが長期EMAを上回っている場合にのみ買いポジションを開き、短期EMAが長期EMAを下回っている場合にのみ空売りポジションを開くことができます。これにより、逆トレードを回避できます。

戦略の利点

単一のRSI戦略と比較して、本戦略はストキャスティクス指標を組み合わせることで、買われ過ぎ・売られ過ぎ領域をより明確に識別でき、シグナルの信頼性が向上します。

単一のストキャスティクス戦略と比較して、本戦略はRSIをストキャスティクスの入力データソースとして使用するため、一部のノイズを除去でき、シグナルがより信頼性の高いものとなります。

移動平均線フィルター条件を設定することで、逆張りでのポジション構築を効果的に回避し、不必要な損失を減らすことができます。

ポジション保有時間の遅延を設定することで、フェイクブレイクアウトによるストップアウトを回避できます。

戦略のリスク

本戦略は主に短周期の指標を使用しているため、短期売買にのみ適しており、長期では効果が薄い可能性があります。

Stochastic RSI指標自体に一定の遅延が生じるため、短期的な価格急変後のシグナルを逃す可能性があります。

レンジ相場では、Stochastic RSI指標が買われ過ぎ・売られ過ぎ領域を複数回往来することがあり、過剰な取引を引き起こし、取引コストが増加する可能性があります。

戦略の最適化方向性

- 異なるパラメータ組み合わせをテストし、Stochastic RSIの長さ、K値、D値をさらに最適化できます。

- 異なるRSI長さパラメータをテストし、より適切なRSI周期長を見つけることができます。

- 他の指標(MACD、ボリンジャーバンドなど)との組み合わせを試み、シグナルの精度をさらに高めることができます。

- 異なるポジション保有時間の遅延パラメータをテストし、より適切なエグジットタイミングを見つけることができます。

まとめ

本稿では、Stochastic RSI指標に基づくモメンタム戦略の構築原理、利点、リスク、最適化のアイデアについて詳述しました。単一指標の戦略と比較して、本戦略はRSIとストキャスティクスの両方の利点を活用し、市場の短期的な買われ過ぎ・売られ過ぎ現象をより明確かつ確実に識別し、逆転トレードを行うことができます。パラメータ最適化や指標の組み合わせにより、戦略の効果をさらに向上させることが期待されます。

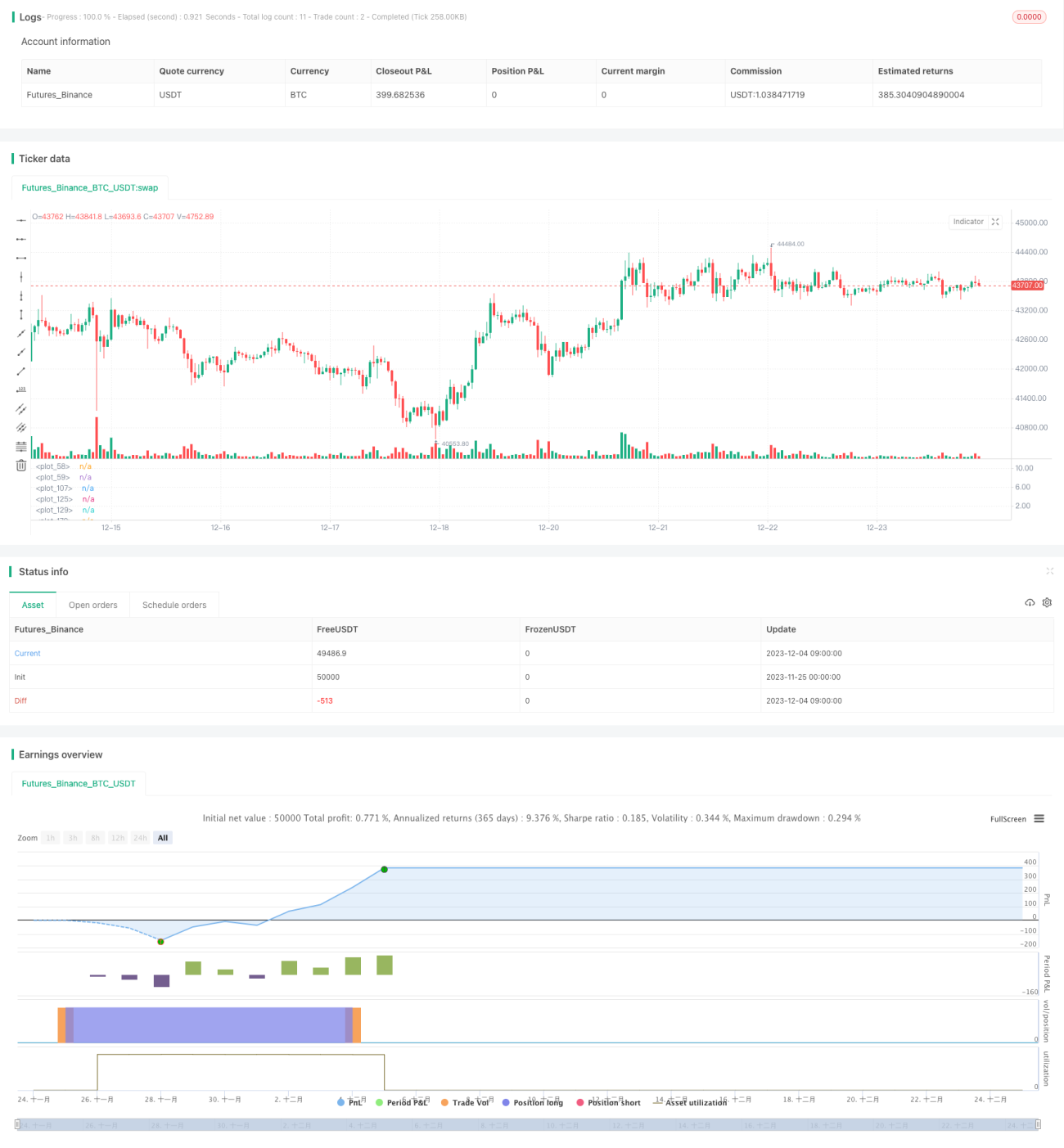

/*backtest

start: 2023-11-25 00:00:00

end: 2023-12-25 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Drun30 (Federico Magnani)

//@version=4- 1