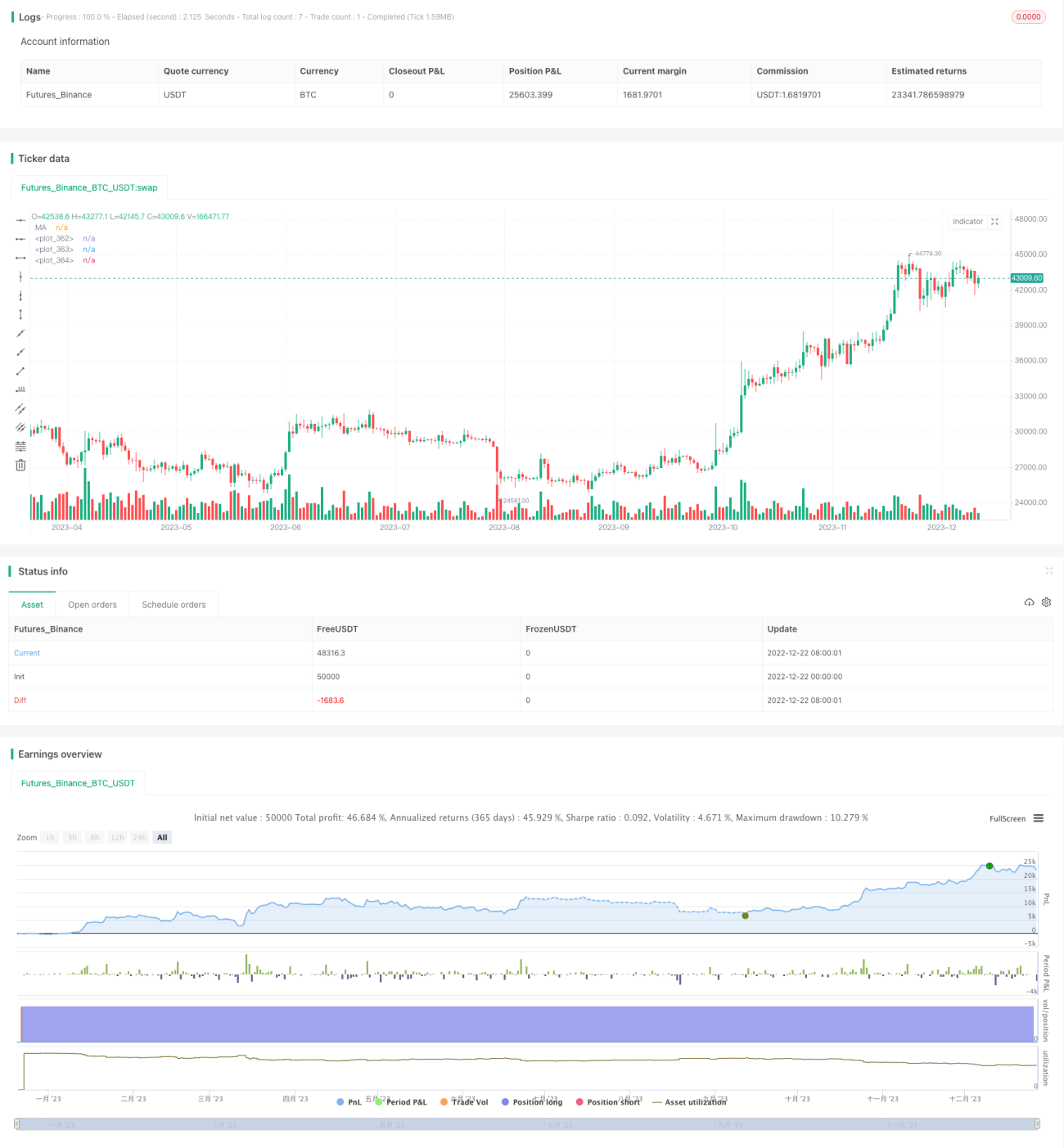

移動平均線リバーサルに基づく短期取引戦略

概要

リバーサル移動平均線戦略は、移動平均線の反転に基づく短期取引戦略です。ボリンジャーバンド、RSI、CCIなどの複数の指標を組み合わせ、金融市場の短期的な相場変動を捉え、安値で買い高値で売るというトレード目標を実現します。

本戦略は主に株価指数、外国為替、貴金属などの流動性の高い銘柄に適用されます。1回の取引ごとの利益を最大化しつつ、全体の取引のリスク・リターン比をコントロールすることを目指します。

戦略の原理

-

ボリンジャーバンドを使用して価格の逸脱領域を判断します。価格が上部バンドに近づいたら売りを検討し、下部バンドに近づいたら買いを検討します。

-

RSIインジケーターを組み合わせて、買われすぎ・売られすぎを判断します。RSIは買われすぎ・売られすぎの状況を効果的に識別できます。

-

CCIインジケーターで価格反転シグナルを判断します。CCIは異常な状況に敏感で、価格反転の機会を効果的に捉えることができます。

-

価格が5日移動平均線を上抜けたら買い、下抜けたら売りとします。移動平均線の位置は現在の価格の主要レンジを表し、価格と移動平均線の関係は潜在的なトレンド変化を反映します。

-

エントリーシグナルが確認された後、迅速にポジションをクローズして利益を確保します。逆行状況に応じてストップロスを設定して退出し、高い勝率を実現します。

戦略の優位性

- 複数の指標を組み合わせることでシグナルの精度が向上

リバーサル移動平均線戦略は、ボリンジャーバンド、RSI、CCIなどの複数の指標を同時に使用します。これらの指標はいずれも価格変動に敏感であり、組み合わせて使用することでシグナルの精度を高め、誤ったシグナルを減らすことができます。

- 厳格なエントリールールにより、高値追いや安値売りを回避

戦略はインジケーターシグナルと価格が同時に発生することを要求し、単一の指標による誤った判断を防ぎます。また、価格が明確に反転したことを要求することで、関連するリスクを軽減します。

- 効率的なストップロスメカニズムにより、1回の損失を抑制

買いでも売りでも、戦略は厳格なストップロスラインを設定します。価格が不利な方向にストップロスラインを突破した場合、迅速にストップロスを実行し、大きな損失を防ぎます。

- 適切な利益確定により、1回の取引ごとの利益を最大化

戦略は2つの利益確定目標を設定し、段階的に利益を確定します。また、利益確定後は小さな調整でトレーリングストップを適用し、1回の取引の利益幅を拡大します。

リスク分析

- 価格の急激な変動によりストップロスが発動される

価格が急激に変動する状況では、ストップロスラインが突破され、不必要な損失が発生する可能性があります。このような状況は通常、重要なイベントによる異常な価格変動で発生します。

ストップロスの幅を広げることでこのリスクに対処でき、また重要なイベントの発生期間中の取引を避けることも有効です。

- 上昇が激しすぎて反転できない

上昇が激しすぎる場合、価格は急騰しすぎて、すぐに反転できません。このような状況で無理に売りを仕掛けると、高値追いや安値売りのリスクに直面する可能性があります。

この場合、一時的に様子を見て、価格の上昇勢いが明らかに弱まってから売り介入を検討すべきです。

最適化の方向性

- インジケーターのパラメータを最適化し、シグナル精度を向上

異なるパラメータ組み合わせでのバックテスト結果を検証し、最適なパラメータを選択できます。例えば、RSIのパラメータやCCIのパラメータなどを最適化できます。

- 出来高インジケーターを組み合わせ、真の反転タイミングを判断

出来高やボリンジャーバンドの幅などの出来高インジケーターを追加できます。これにより、価格が小幅な調整だけのときに誤ったシグナルが発生するのを防げます。

- 利益確定・ストップロス戦略を最適化し、1回の取引利益を拡大

異なる利益確定・ストップロスポイントをテストし、1回の取引の利益を最大化します。同時にリスクバランスを考慮し、ストップロスが簡単に発動されないようにします。

まとめ

リバーサル移動平均線戦略は、複数の指標を総合的に活用し、シグナルの正確性、操作の規律性、リスクのコントロール性を備えています。市場変動への感応度が高く、流動性が強い銘柄に適しており、価格がボリンジャーバンドと重要な移動平均線の間で反転する機会を捉え、安値買い高値売りのトレード目標を実現します。

実際の適用では、インジケーターパラメータの最適化に注意を払うとともに、出来高インジケーターを組み合わせて真の反転タイミングを判断する必要があります。また、価格の急激な変動に対してはリスク管理を徹底する必要があります。適切に運用すれば、本戦略は比較的安定したアルファ収益を得ることができます。

- 1