短期トレンドフォロー反転戦略

概要

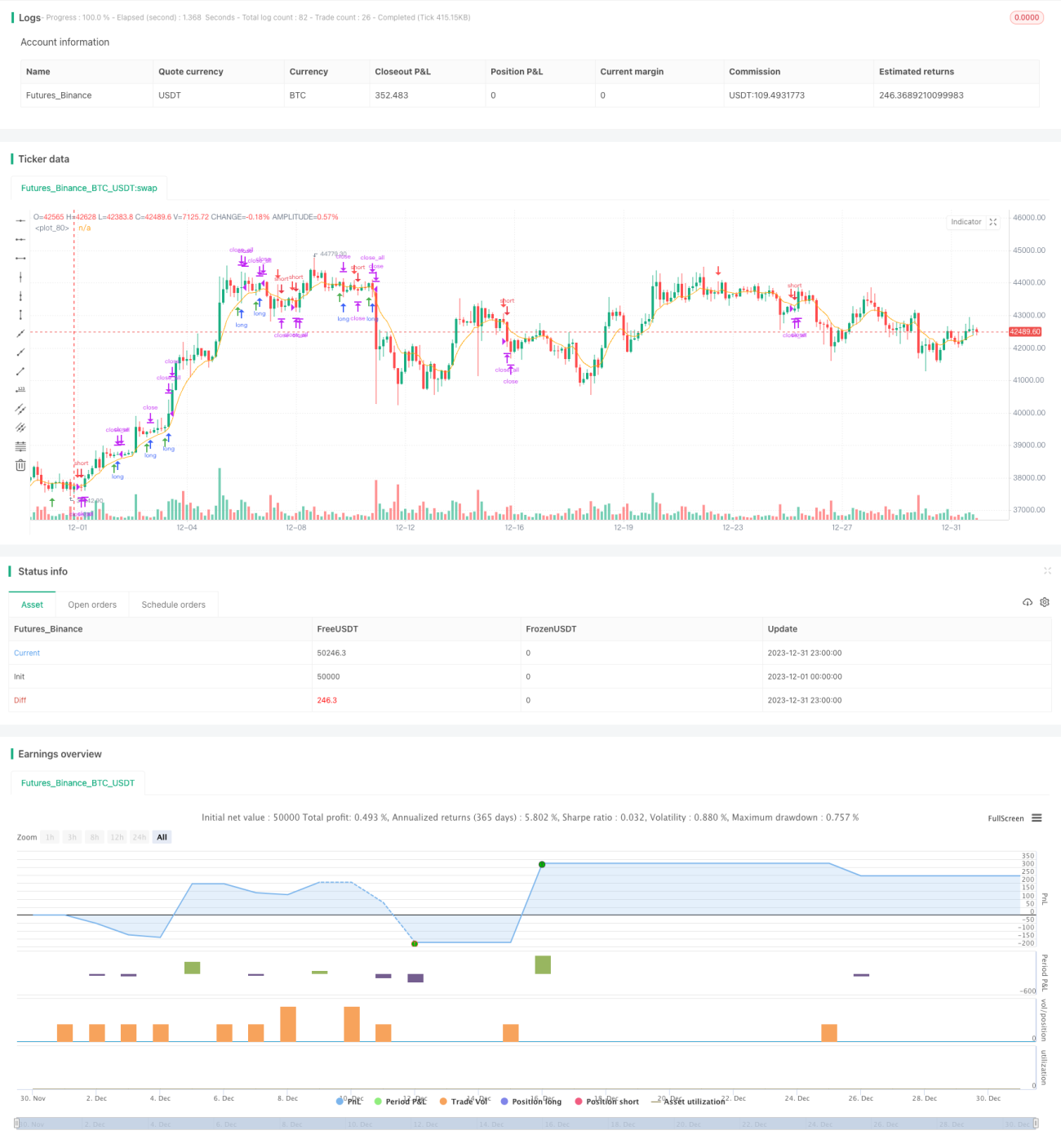

トレンド追跡反転戦略は、15分NQ先物をベースとした短期トレンド取引戦略です。トレンドフィルターと反転パターンの識別を通じて取引機会を探します。この戦略はシンプルで効果的であり、短期間で活発に取引するトレーダーに適しています。

戦略の原理

この戦略は主に以下の原理に基づいて動作します:

-

8周期のEMAを主要なトレンドフィルター指標として使用し、EMAより上は強気、EMAより下は弱気と判断します。

-

特定のローソク足反転パターンをエントリーシグナルとして識別します。これには、長い陽線の後の短い陰線による強気シグナルと、長い陰線の後の短い陽線による弱気シグナルが含まれ、これらのパターンはトレンドが反転し始める可能性を示唆します。

-

エントリーポイントは反転ローソク足の高値または安値付近に設定し、ストップロスは反転ローソク足自体の高値・安値に設定することで、効率的なリスクリターン比を実現します。

-

ローソク足の実体関係を利用して反転シグナルの有効性を判断します。例えば、陰線の始値が前のローソク足の実体より高い、実体が完全に含まれているなどのルールでノイズをフィルタリングします。

-

特定の取引時間帯のみで戦略を実行し、市場の主要な限月交代などの特殊な時間帯を避けることで、異常な相場による不要な損失を防ぎます。

優位性分析

この戦略には以下の主な利点があります:

-

戦略シグナルはシンプルで効果的であり、習得・実装が容易です。

-

トレンドと反転の判断に基づくため、強気相場と弱気相場の両方で二重の損害を受けることを回避します。

-

リスク管理が行き届いており、ストップロス設定が合理的で、資金管理に役立ちます。

-

データ量が少なくて済むため、様々なソフトウェアやプラットフォームで使用できます。

-

取引頻度が比較的高く、短期間で活発な取引を好む投資家に適しています。

リスクと対策

この戦略にはいくつかのリスクも存在し、主な問題は以下の通りです:

-

反転パターンの機会が不足し、シグナルが少ない。反転判断ルールを適度に緩和することで対応可能です。

-

偽のブレイクアウトが時々発生する。より多くのフィルター指標を追加して共同判断することで対応可能です。

-

夜間取引や非主流時間帯では不安定さがある。米国の取引時間帯のみで運用する設定が可能です。

-

パラメータ最適化の余地が限られている。機械学習などの技術を試してより良いパラメータを探すことができます。

最適化の方向性

この戦略にはまだ一定の最適化の余地があり、主な方向性は以下の通りです:

-

より長い周期のEMAパラメータをテストし、トレンド判断を改善する。

-

株式市場の主要指数を追加のトレンドフィルター指標として使用する。

-

機械学習などの技術を利用してエントリーポイントとストップロスポイントを自動最適化する。

-

ボラティリティに基づくポジションサイズとストップロスの動的調整メカニズムを追加する。

-

複数の銘柄でのアービトラージを試み、単一銘柄のシステムリスクをさらに分散させる。

まとめ

トレンド追跡反転戦略は全体として非常に実用的な短期戦略の考え方であり、シンプルでパラメータが少なく、実践にも取り組みやすく、個人リスクをうまくコントロールできるため、株フォーラムの活発な短期トレーダーに適しています。この戦略には一定の最適化の余地があり、一定の研究開発努力を投入すれば、中長期的な資金でのプログラム運用にも適応可能となり、発展の可能性が高いです。

- 1