スーパートレンド指標と単純移動平均線に基づく戦略

概要

スーパートレンドデュアル移動平均線戦略は、スーパートレンド指標と単純移動平均線をベースにした定量取引戦略です。この戦略はスーパートレンド指標を用いて市場のトレンド方向を判断し、200日単純移動平均線でフィルターをかけ、大きなトレンド方向に沿ってロング・ショートのポジションを取ります。

戦略の原理

この戦略では以下の2つの指標を使用します。

-

スーパートレンド指標:真のレンジ(ATR)と乗数に基づいて上限線と下限線を計算します。終値が上限線を上回れば強気、下限線を下回れば弱気と判断します。

-

200日単純移動平均線:直近200日の終値の算術平均を取ります。終値がこの線を上回れば大きなトレンドは強気、下回れば弱気と判断します。

戦略のロジック:

-

スーパートレンド指標が強気(値が0より大きい)かつ終値が200日移動平均線を上回る場合、ロングエントリーします。

-

スーパートレンド指標が弱気(値が0より小さい)かつ終値が200日移動平均線を下回る場合、ショートエントリーします。

-

スーパートレンド指標が前のシグナルと逆転した場合、ポジションをクローズします。

-

ストップロスは25%に設定します。

優位性分析

この戦略はスーパートレンド指標による短期トレンド判断と200日移動平均線による長期トレンド判断を組み合わせることで、偽のブレイクアウトを効果的にフィルタリングし、取引頻度を減らしながら勝率を高めます。大きな相場ではトレンドが明確であり、ストップロスの幅が大きく、利益も大きくなります。

リスク分析

この戦略の主なリスクはストップロスの幅が大きいことで、高レバレッジ時には強制決済のリスクが高まります。また、相場がレンジ相場の場合、スーパートレンド指標が余分なシグナルを発生させ、取引頻度とコストが増加します。

ATR期間や乗数パラメータ、ストップロス幅を適切に調整することでリスクを軽減できます。

最適化の方向性

この戦略は以下の点で最適化が可能です。

-

ATR期間と乗数パラメータを調整し、スーパートレンド指標のパラメータを最適化する。

-

EMAやVIDYAなど他の移動平均線指標に置き換えて試す。

-

ボリンジャーバンドやストキャスティクスなど補助指標を追加し、シグナルをさらにフィルタリングする。

-

ストップロス戦略を最適化する。例えば、損益分岐点への移動や大きなトレンドのストップロスに合わせるなど。

まとめ

本戦略は全体的に非常に実用的であり、短期トレンド判断と長期トレンド判断の両方を考慮し、ストップロス設定も比較的妥当です。パラメータ調整と最適化によりさらに効果を高めることができ、実運用での検証と活用に値します。

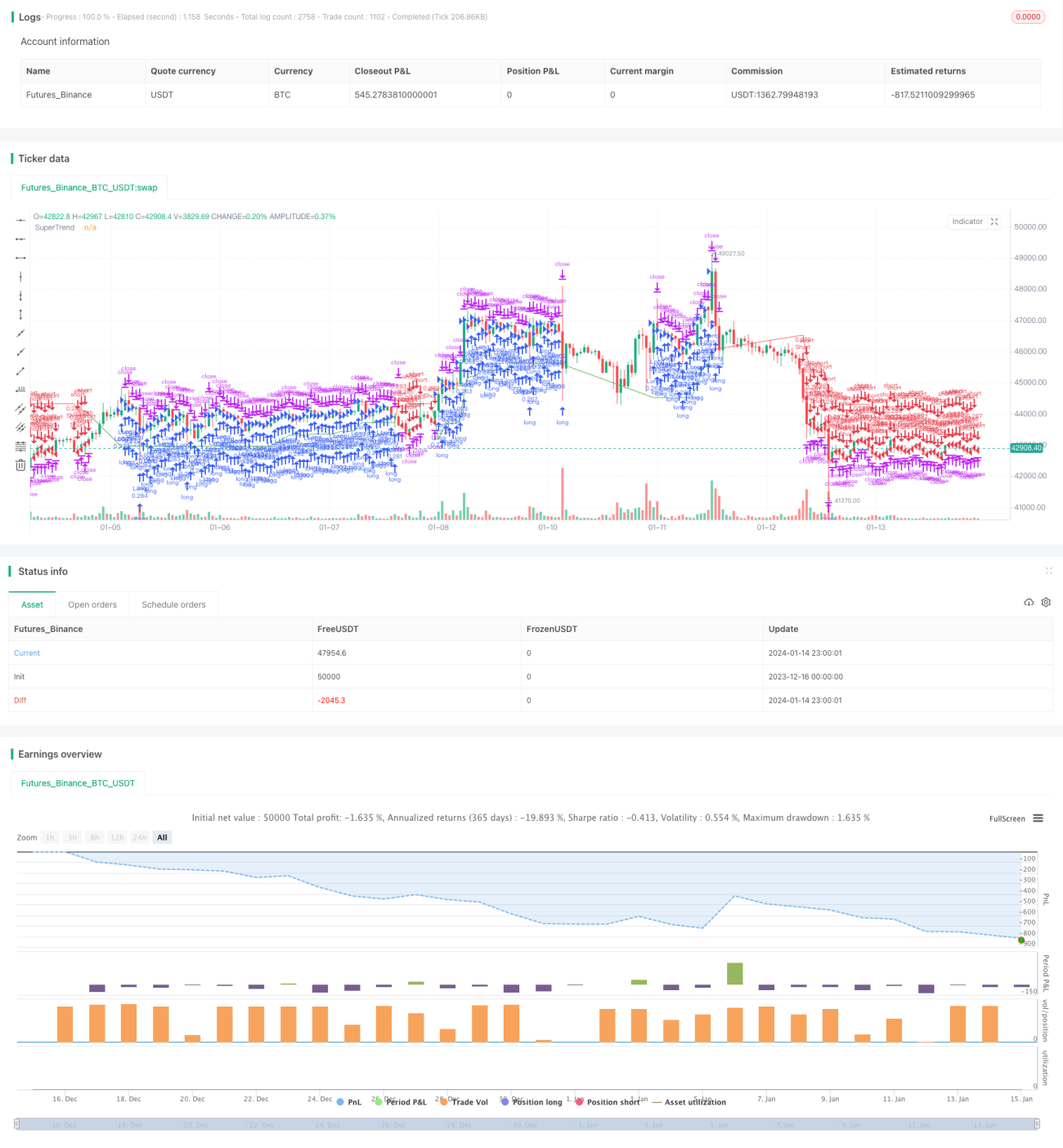

/*backtest

start: 2023-12-16 00:00:00

end: 2024-01-15 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This work is licensed under a Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) https://creativecommons.org/licenses/by-nc-sa/4.0/

// © wielkieef

//@version=5- 1