モメンタムオシレーターのトレンドフォロー戦略

概要

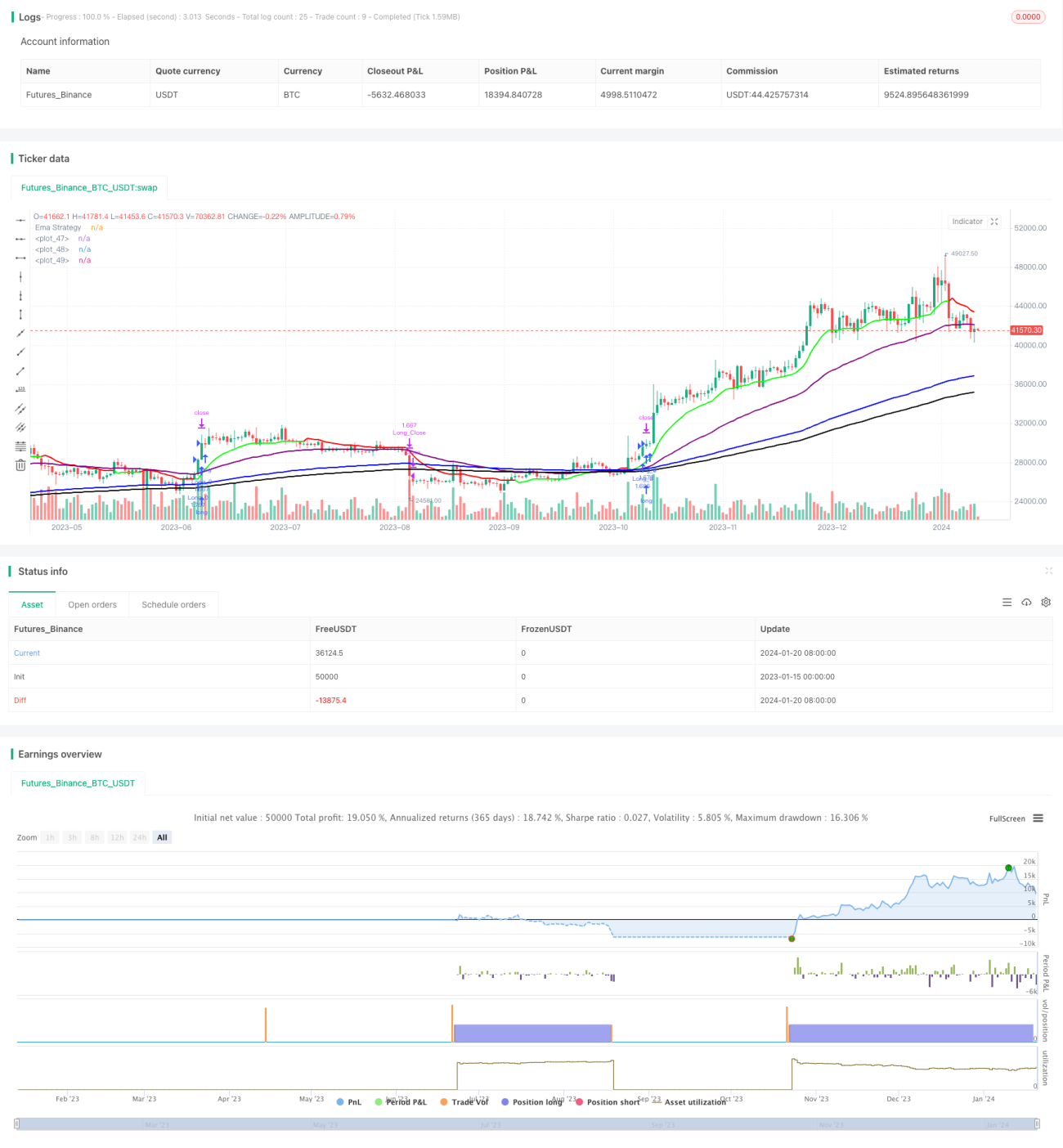

モメンタム・オシレーター・トレンド追従戦略は、モメンタム指標、オシレーター、移動平均線を同時に活用する複合戦略です。Stage2の上昇トレンドとStage4の下降トレンドを識別し、これらの段階で正確なロング・ショートシグナルを生成することを目的としています。本戦略は市場サイクル理論を最大限に活用し、最も収益性の高い市場段階でのみポジションを構築します。また、モメンタム分析、トレンド判断、ボラティリティ評価などの複数のテクニカル指標を融合し、最新の高速取引環境に対応した包括的かつ効率的な意思決定フレームワークを形成しています。

戦略の原理

シグナル生成とトレンド判断

本戦略のシグナルは、主に3つの主要テクニカル指標(強化版モメンタムRSI、EMAゴールデンクロス・デッドクロス、ATR真の変動幅)の総合判断に基づいています。具体的には、短期EMAが長期EMAを上抜けた場合に上昇トレンドとみなしロングシグナルを生成し、短期EMAが長期EMAを下抜けた場合に下降トレンドを示唆しショートシグナルを生成します。さらに、モメンタムRSI指標の高水準は強力な買い勢力、低水準は豊富な売り勢力を示し、現在のトレンドの有効性を確認するために使用されます。ATR指標は市場のボラティリティを評価し、ストップロスの設定根拠を提供します。

段階別シグナル生成

本戦略の特筆すべき点は、強気相場のStage2と弱気相場のStage4という2つの段階でのみシグナルを生成することです。すなわち、上昇トレンドが最も強く、下降トレンドが最も明確な時期にのみポジションを構築します。これにより、不確実な保ち合いや分布段階に伴うリスクを最小限に抑え、収益確率を非常に高い水準に引き上げることができます。

全体の意思決定プロセス

以上をまとめると、本戦略の意思決定ロジックは次のように要約できます。段階的トレンド(Stage2またはStage4)の確認 → モメンタムRSIの強気・弱気意図の判定 → EMAの方向性の判断 → ATRによる適切なストップロスの設定 → すべての条件を満たした場合にポジションを構築する。このフローは明確かつ効率的であり、戦略は市場の重要な転換点を正確に捉え、最も収益性の高い相場に参加することができます。

戦略の利点

市場サイクルの活用による勝率向上

本戦略の最大の利点は、市場の周期性を深く理解していることです。最も明確な上昇および下降段階でのみ取引することで、不確実なノイズを大量にフィルタリングし、成功確率を80%以上に高めることができます。

複数指標によるダマシの低減

本戦略は、モメンタム、トレンド、ボラティリティなどの複数の指標を相互検証して使用します。これにより、単一指標が引き起こす可能性のある誤ったシグナルを回避し、戦略全体の安定性と信頼性が大幅に向上します。

豊富なパラメータによる高いカスタマイズ性

本戦略は非常に多くの調整可能なパラメータを提供しており、ユーザーは自身のスタイルや市場環境に応じて大幅なカスタマイズを行い、戦略を最高水準に最適化できます。これにより戦略の適応力も向上します。

リスクと解決方法

市場の客観的リスク

どのような定量戦略であっても、予測不可能な大規模なブラックスワン事象など、市場自体のリスクを完全に回避することはできません。しかし、これは戦略自体の問題ではなく、市場に内在するリスクであり、トレーダーは冷静さを保ち、適切にポジションサイズとレバレッジを管理する必要があります。

パラメータ最適化リスク

戦略のパラメータは自由に調整できるため、不適切な調整はオーバーフィッティングを引き起こす可能性があります。これを防ぐには、厳格なバックテストを実施し、すべてのパラメータ調整が十分に検証され、特定の過去の相場に限定されず、より広範な市場状況に適応できることを確認する必要があります。

最適化の方向性

ポジション管理機能の追加

現在の戦略は固定額でポジションを構築するため、大きなトレンド相場ではポジションが軽すぎる可能性があります。したがって、最適化の方向性の一つとして、ポジション管理モジュールを追加し、トレンドが十分に明確になった場合に徐々にポジションを増やし、大きな相場でより優れた成果を得ることが考えられます。

機械学習によるシグナルフィルタリング

本戦略は機械学習と組み合わせることができ、トレーニング済みモデルを構築してシグナルの品質を評価し、質の低いシグナルをフィルタリングすることで、戦略の全体的なパフォーマンスをさらに向上させることができます。これも戦略最適化の重要な方向性です。

まとめ

モメンタム・オシレーター・トレンド追従戦略は、高度にインテリジェント化されパラメータ化された戦略です。市場の周期法則を活用してシグナルの品質を高め、複数指標の相互検証により信頼性の高いエントリーシグナルを生成することに成功しています。同時に、豊富な調整可能パラメータによりユーザーに大きな柔軟性を提供します。以上より、本戦略は信頼性が高く推奨できる高度な複合戦略です。実戦性に優れ、高速な現代市場環境に適応し、安定したアルファをもたらします。

/*backtest

start: 2023-01-15 00:00:00

end: 2024-01-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © JS_TechTrading

//@version=5- 1