ウィリアムズ・フラクタルとZZインジケーターを組み合わせた定量取引戦略

概要

これは、Bill Williamsのフラクタル理論とZZインジケーターを組み合わせた定量取引戦略です。この戦略では、Williamsフラクタルを計算して市場のトレンドを判断し、ZZインジケーターを用いてサポート・レジスタンスラインを描画することで、潜在的なブレイクアウトポイントを発見し、トレンドフォロー取引を実現します。

戦略の原理

この戦略はまずWilliamsフラクタルを計算し、現在が上昇フラクタルか下降フラクタルかを判断します。上昇フラクタルの場合は上昇トレンド、下降フラクタルの場合は下降トレンドとみなします。

次に、フラクタルポイントに基づいてZZインジケーターのサポートラインとレジスタンスラインを描画します。価格が上昇フラクタルに対応するレジスタンスラインを突破した場合にロング、下降フラクタルに対応するサポートラインを突破した場合にショートとします。

この組み合わせにより、トレンドが変化したタイミングを捉え、トレンドフォロー取引を実現します。

戦略の優位性分析

この戦略は、WilliamsフラクタルとZZインジケーターという異なるテクニカル分析手法を組み合わせることで、より多くの取引機会を発掘します。

市場トレンドの変化を迅速に判断し、適切なストップロスとテイクプロフィット条件を設定することで、主要なトレンド方向を捉えるのに役立ちます。また、ZZインジケーターにより一部の偽ブレイクをフィルタリングし、不要な損失を回避できます。

総じて、この戦略はトレンド判断と具体的なエントリーポイント選択の両方を考慮し、リスクとリターンのバランスを実現しています。

戦略のリスク分析

この戦略の最大のリスクは、フラクタル判断やZZインジケーターが誤った取引シグナルを発し、不必要な損失を招く可能性があることです。例えば、レジスタンスラインを突破した後、価格がすぐに戻り、上昇が持続しない場合があります。

また、フラクタルの計算方法は、時間周期の設定が適切でないと判断ミスを引き起こす可能性があります。時間周期が短すぎると、偽ブレイクの確率が高まります。

これらのリスクを低減するには、フラクタルの計算パラメータを適切に調整したり、フィルター条件を追加して誤シグナルを減らすことが考えられます。また、ストップロスの幅を大きめに設定し、1回あたりの損失をコントロールすることも有効です。

戦略の最適化方向性

この戦略は、以下の点でさらに最適化できます。

-

モメンタム指標(MACDやボリンジャーバンドなど)をフィルターとして追加し、一部の偽ブレイクを回避する。

-

フラクタルパラメータの設定を最適化し、高値・安値の計算方法を調整、時間周期を短縮してより正確なトレンド判断を得る。

-

機械学習アルゴリズムを追加し、トレンドの正確性を判断することで、人手による設定の限界を回避する。

-

適応型ストップロス機構を追加し、市場の変動度合いに応じてストップロスの幅を調整する。

-

深層学習アルゴリズムを活用し、全体のパラメータ設定を最適化する。

まとめ

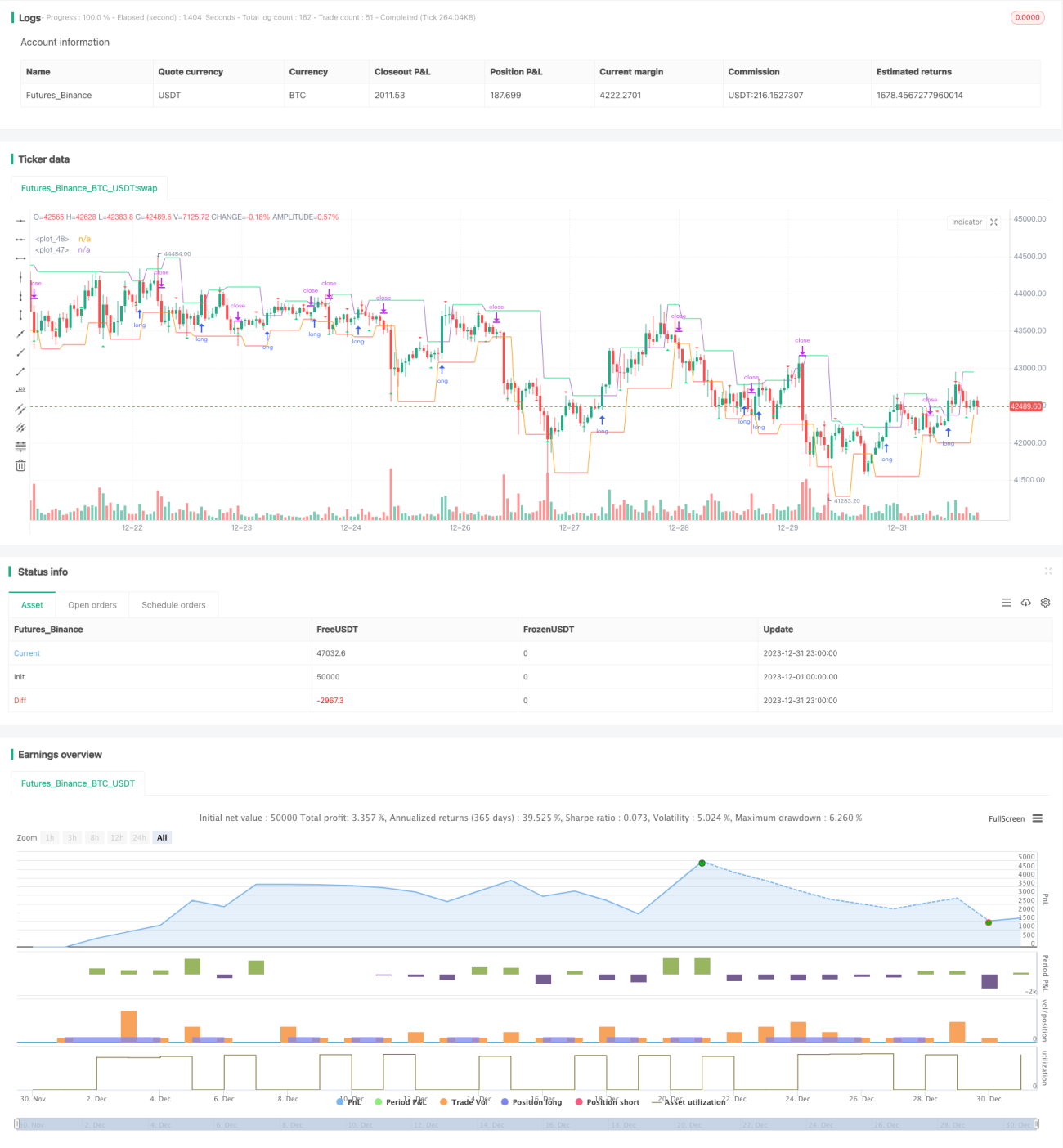

本戦略は、Williamsフラクタル理論とZZインジケーターを巧みに組み合わせることで、市場トレンドの変化を迅速に判断し捉えることを実現しています。高い勝率を維持し、長期的に安定した超過リターンが期待できます。今後、より多くのフィルター手段やAIの判断力を導入することで、戦略の安定性と収益率をさらに向上させることができるでしょう。

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "robotrading ZZ-8 fractals", shorttitle = "ZZ-8", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 100, commission_value = 0.1)

//Settings- 1