極端なNoroトレンド移動平均線戦略

概要

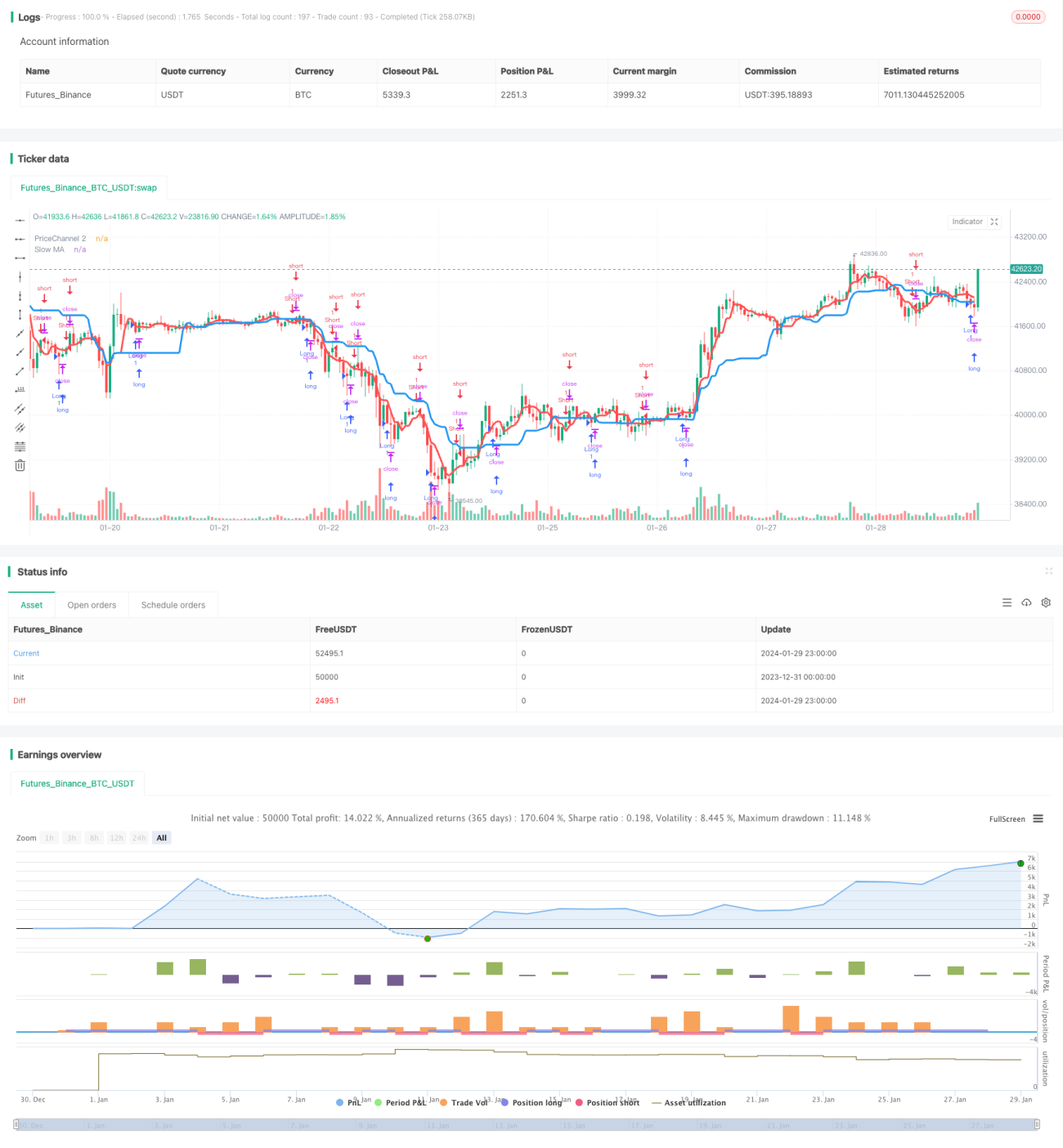

本戦略は、2つの移動平均線インジケーターを使用してトレンドの方向性や買い・売りのタイミングを特定します。そのうち、低速移動平均線(青線)は全体のトレンド方向を判断するために用いられ、高速移動平均線(赤線)は価格チャネルと組み合わせて買い・売りのタイミングを発見するために使われます。

戦略の原理

-

高速と低速の2つの移動平均線を計算します。低速移動平均線の期間は21で、全体のトレンドを判断します。高速移動平均線の期間は5で、価格チャネルと組み合わせて取引のタイミングを発見します。

-

現在の価格が前の期間の価格チャネルを突破したかどうかを計算します。価格がチャネルを突破した場合、それを取引機会とみなします。

-

ローソク足の方向と本数を計算します。直近N本のローソク足がすべて陰線であれば買いのタイミング、すべて陽線であれば売りのタイミングとなる可能性があります。Nの本数はBarsパラメータで設定します。

-

以上の要素を総合して買い・売りのシグナルを発生させます。相場が低速移動平均線の方向と一致し、かつ高速移動平均線または価格チャネルがシグナルを出し、さらにローソク足の条件も満たす場合に取引シグナルを発生させます。

戦略のメリット

-

二重移動平均線システムを使用することで、トレンド方向を効果的に追跡できます。

-

高速移動平均線と価格チャネルの組み合わせにより、ブレイクアウトポイントを早期に発見し、取引タイミングを捉えることができます。

-

シグナル発生時にローソク足の方向と本数も考慮するため、逆転相場による損失を回避できます。

-

移動平均線のパラメータは自由に調整可能で、異なる銘柄や時間足に適用できます。

戦略のリスクと解決方法

-

二重移動平均線は、レンジ相場において誤ったシグナルを出しやすいです。価格差インジケーターやATRインジケーターを補助的に使用して判断することで、ボラティリティの低い相場での取引を回避できます。

-

異常な相場では損失を被る可能性があります。適切なストップロスポイントを設定して、1回の損失を最小限に抑えます。

-

逆転による損失を完全に回避することはできません。引き続きメカニズムとパラメータを最適化し、戦略をより安定させます。

戦略の最適化方向性

-

ADXやMACDなどの補助インジケーターを追加して判断し、レンジ相場での誤取引を回避します。

-

ストップロスポイントを動的に調整します。ATRに基づいてリスク見込みを計算し、適切なストップロス比率を設定できます。

-

パラメータの自己適応能力を最適化します。機械学習手法を用いて、システムが自動的にパラメータを最適化できるようにします。

-

銘柄の特性に応じてパラメータを微調整します。例えば、暗号通貨はより短い期間のパラメータが適しています。

まとめ

本戦略は全体的にトレンド相場の追跡に非常に適しています。また、一定のブレイクアウト取引機会も追加されています。適切な最適化により、より多くの市場で安定して稼働させることができます。引き続き改善を重ね、商業レベルの高品質な定量戦略に育てていきます。

/*backtest

start: 2023-12-31 00:00:00

end: 2024-01-30 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

strategy(title = "Noro's Trend MAs Strategy v1.9 Extreme", shorttitle = "Trend MAs str 1.9 extreme", overlay=true, default_qty_type = strategy.percent_of_equity, default_qty_value=100.0, pyramiding=0)

//Settings- 1