KDJ陽線突破買い戦略

概要

KDJ陽線突破買い戦略は、KDJ指標に基づく量的取引戦略です。この戦略は主にKDJ指標のJ線とD線のゴールデンクロスを買いシグナルとして利用し、J線がD線を上抜けた際に買いポジションを取ります。この戦略は比較的シンプルで実装が容易であり、量的取引の初心者に適しています。

戦略の原理

この戦略で使用される主なテクニカル指標はKDJ指標です。KDJ指標はK線、D線、J線で構成されています。それぞれの計算式は以下の通りです。

K値 = (当日の終値 - N日間の最安値) ÷ (N日間の最高値 - 最安値) × 100

D値 = K値のM日移動平均

J値 = 3K - 2D

KDJ指標の定義に基づき、J値がD値を上抜けた場合、株価が反転上昇していると判断し、買いポジションを取ることができます。逆に、J値がD値を下抜けた場合、株価が反転下落していると判断し、売りポジションを取ることができます。

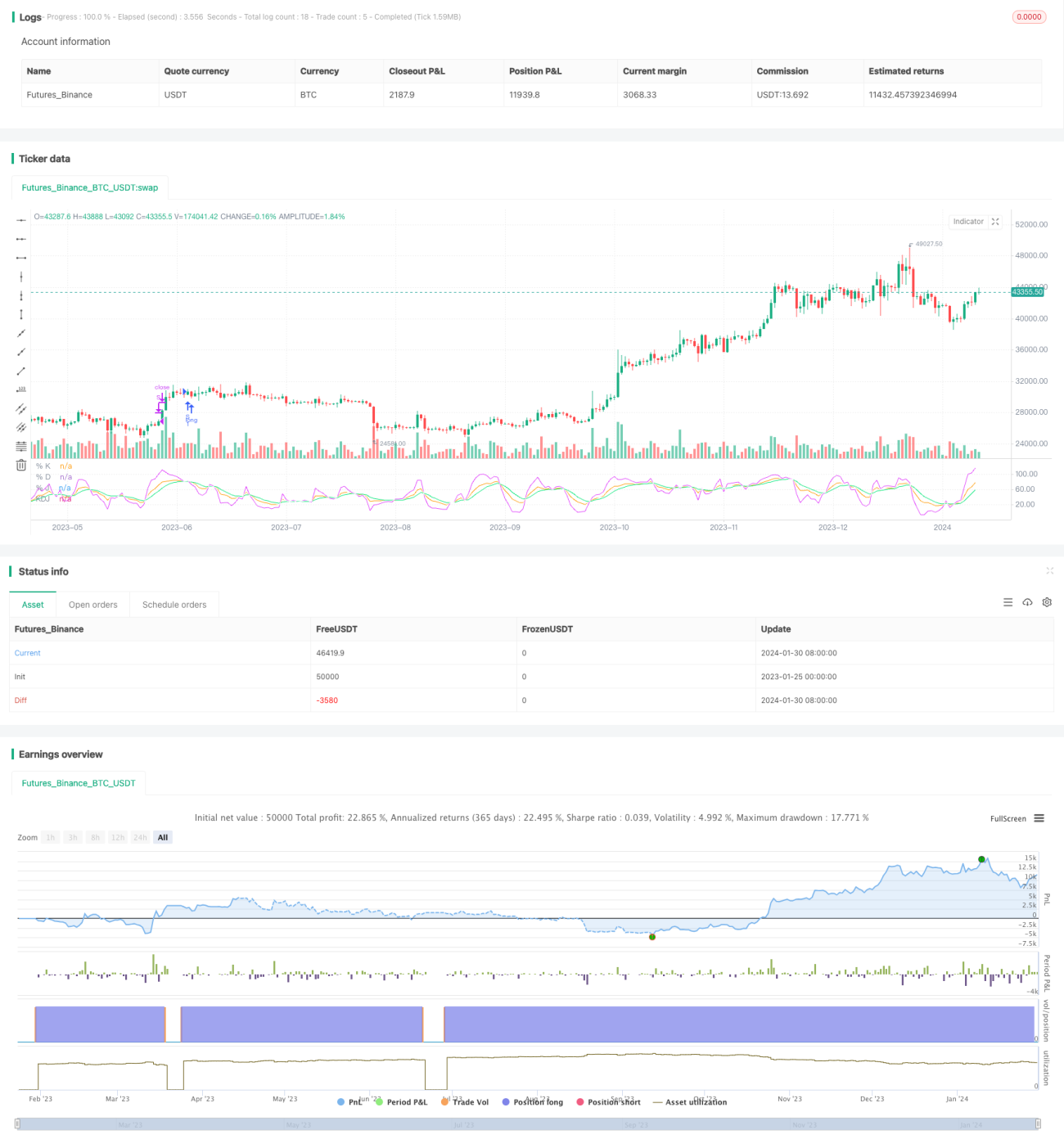

本戦略は上記のルールを利用し、J線がD線を上抜けた時、すなわちゴールデンクロスが形成された時を買いシグナルと判断し、買いエントリーを行います。エグジットシグナルは、J線が100を超えた時点で買いポジションを手仕舞います。

戦略の優位性

-

KDJ指標を使用して買いのタイミングを判断しており、この指標は株価の上昇・下落情報を総合的に考慮しているため、比較的信頼性が高い。

-

戦略のシグナル判断ルールはシンプルで明確であり、理解と実装が容易で、量的取引の初心者に適している。

-

利確・損切りの戦略を採用しており、リスクを効果的に管理できる。

-

戦略のパラメータ最適化の余地が大きく、柔軟な実装が可能。

戦略のリスク

-

KDJ指標は偽のシグナルを形成しやすく、損失につながる可能性がある。

-

買いエントリー後の短期的な市場調整により、損切りが発生し、大きなトレンドを捉えられないことがある。

-

パラメータ設定が不適切だと、取引頻度が高くなったり、シグナルが不明瞭になったりする可能性がある。

-

取引コストが全体の収益に与える影響に注意する必要がある。

主なリスク管理方法:パラメータの適切な最適化、指数強化の追跡、損切り幅の適度な緩和など。

最適化の方向性

-

KDJのパラメータを最適化し、最適なパラメータの組み合わせを探す。

-

フィルター条件を追加し、偽のシグナルを回避する。他の指標やパターンと組み合わせてフィルタリング可能。

-

市場のタイプ(強気相場・弱気相場)に応じて異なるパラメータ設定を選択する。

-

損切り幅を適度に緩和し、損切りによる手仕舞いの確率を減らす。

-

出来高などの指標を組み合わせて分析し、嵌まるリスクを回避する。

まとめ

KDJ陽線突破買い戦略は全体的にシンプルで実用的であり、初心者でも容易に実装できるため、特に量的取引の初心者に適しています。この戦略には一定の取引上の優位性がありますが、いくつかのリスクも存在するため、戦略の価値を最大限に発揮するには、対象を絞った最適化が必要です。総じて、本戦略は重点的に研究・応用する価値があります。

- 1