懒熊モメンタムスクイーズ戦略

概要

ラクダモメンタムスクイーズ戦略は、ボリンジャーバンド、ケルトナーチャネル、モメンタムインジケーターを組み合わせたアルゴリズム取引戦略です。ボリンジャーバンドとケルトナーチャネルを用いて市場がスクイーズ状態にあるかどうかを判断し、その後モメンタム指標と組み合わせて取引シグナルを生成します。

本戦略の主な利点は、トレンド性相場の開始を自動的に識別し、モメンタム指標を組み合わせてエントリーのタイミングを判断できることです。しかし、一定のリスクも存在し、商品ごとにパラメーターの最適化が必要です。

戦略の仕組み

ラクダモメンタムスクイーズ戦略は、以下の3つの指標に基づいて判断を行います。

- ボリンジャーバンド:ミドルバンド、アッパーバンド、ロワーバンドで構成

- ケルトナーチャネル:ミドルバンド、アッパーバンド、ロワーバンドで構成

- モメンタム指標:現在の価格とn日前の価格の差

ボリンジャーバンドのアッパーバンドがケルトナーチャネルのアッパーバンドを下回り、かつボリンジャーバンドのロワーバンドがケルトナーチャネルのロワーバンドを上回る場合、市場はスクイーズ状態にあると判断します。これは通常、トレンド性相場がまもなく開始することを意味します。

エントリータイミングを決定するために、モメンタム指標を使用して価格変動の速度を判断します。モメンタムがその平均値を上抜けた場合に買いシグナルを生成し、モメンタムがその平均値を下抜けた場合に売りシグナルを生成します。

戦略のメリット分析

ラクダモメンタムスクイーズ戦略の主なメリットは以下の通りです。

- トレンド開始のタイミングを自動的に識別し、早期にエントリーできる

- 複数の指標を組み合わせて判断するため、偽シグナルを回避できる

- トレンドと反転の両方の取引スタイルに対応

- パラメーターをカスタマイズでき、商品ごとに最適化が可能

リスク分析

ラクダモメンタムスクイーズ戦略には、以下の一定のリスクも存在します。

- ボリンジャーバンドやケルトナーチャネルが偽シグナルを発する確率が比較的高い

- モメンタム指標のパフォーマンスが不安定で、最適なエントリーポイントを逃す可能性がある

- パラメーターの最適化が必要で、最適化が不十分だと効果が上がらない

- 取引商品との相関性が高い

リスクを低減するためには、ボリンジャーバンドとケルトナーチャネルの期間パラメーターを最適化し、ストップロス水準を調整し、流動性の高い取引商品を選択し、他の指標と組み合わせて検証することを推奨します。

戦略の最適化方向性

ラクダモメンタムスクイーズ戦略の効果をさらに高めるための主な最適化方向性は以下の通りです。

- 異なる商品・時間足でのパラメーター組み合わせをテストする

- ボリンジャーバンドとケルトナーチャネルの期間を最適化する

- モメンタム指標の期間を最適化する

- 買いエントリーと売りエントリーで異なるストップロス・テイクプロフィット戦略を策定する

- 他の指標を追加してシグナルの検証を行う

多方面からのテストと最適化により、本戦略の勝率と収益性を大幅に向上させることができます。

まとめ

ラクダモメンタムスクイーズ戦略は、複数の指標を統合して高い判断力を持ち、トレンド開始のタイミングを効果的に識別できます。しかし、一定のリスクも存在し、取引商品ごとにパラメーターの最適化が必要です。継続的なテストと最適化により、本戦略は効率的なアルゴリズム取引システムになり得ます。

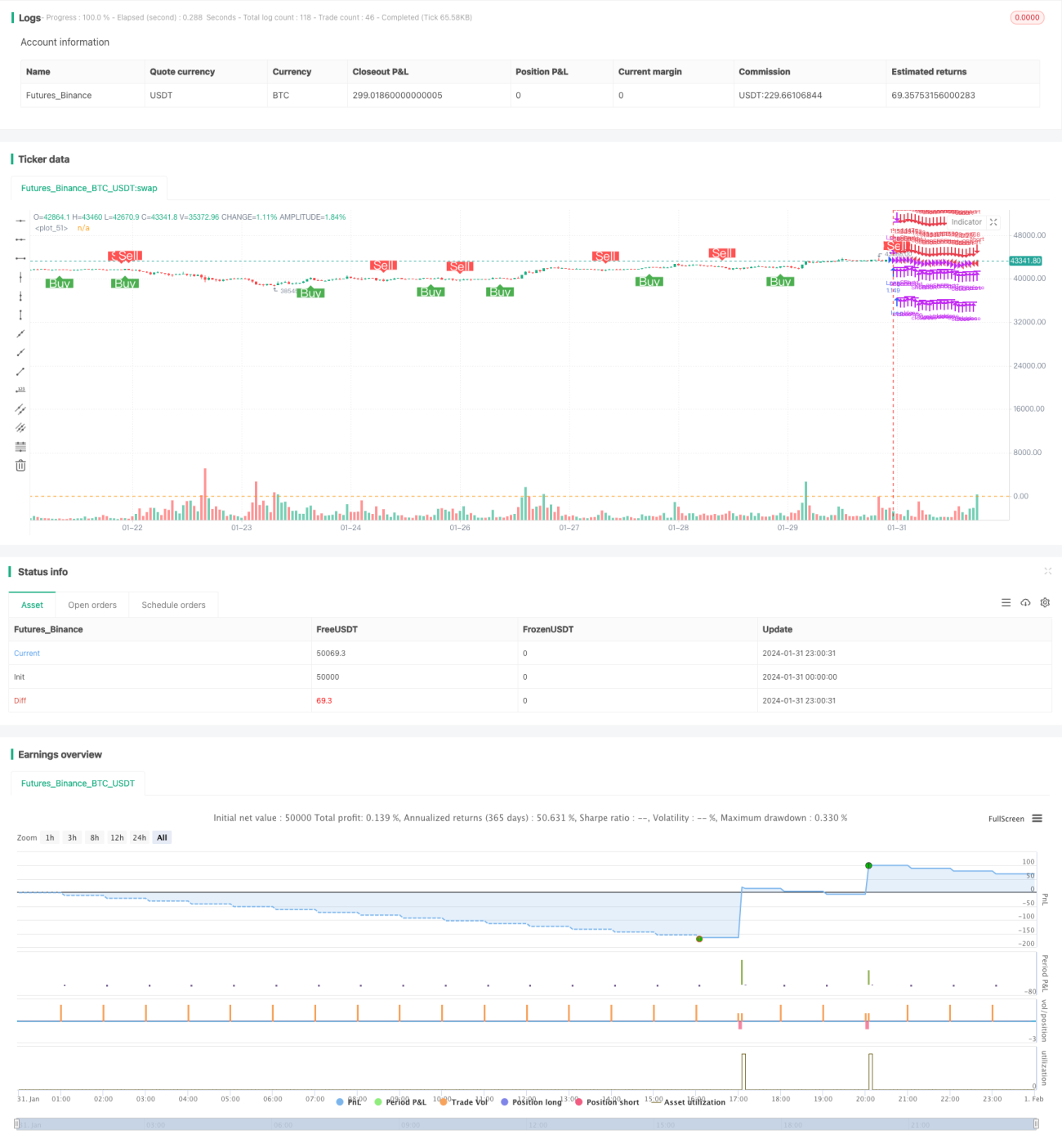

/*backtest

start: 2024-01-31 00:00:00

end: 2024-02-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © mtahreemalam original strategy by LazyBear

- 1