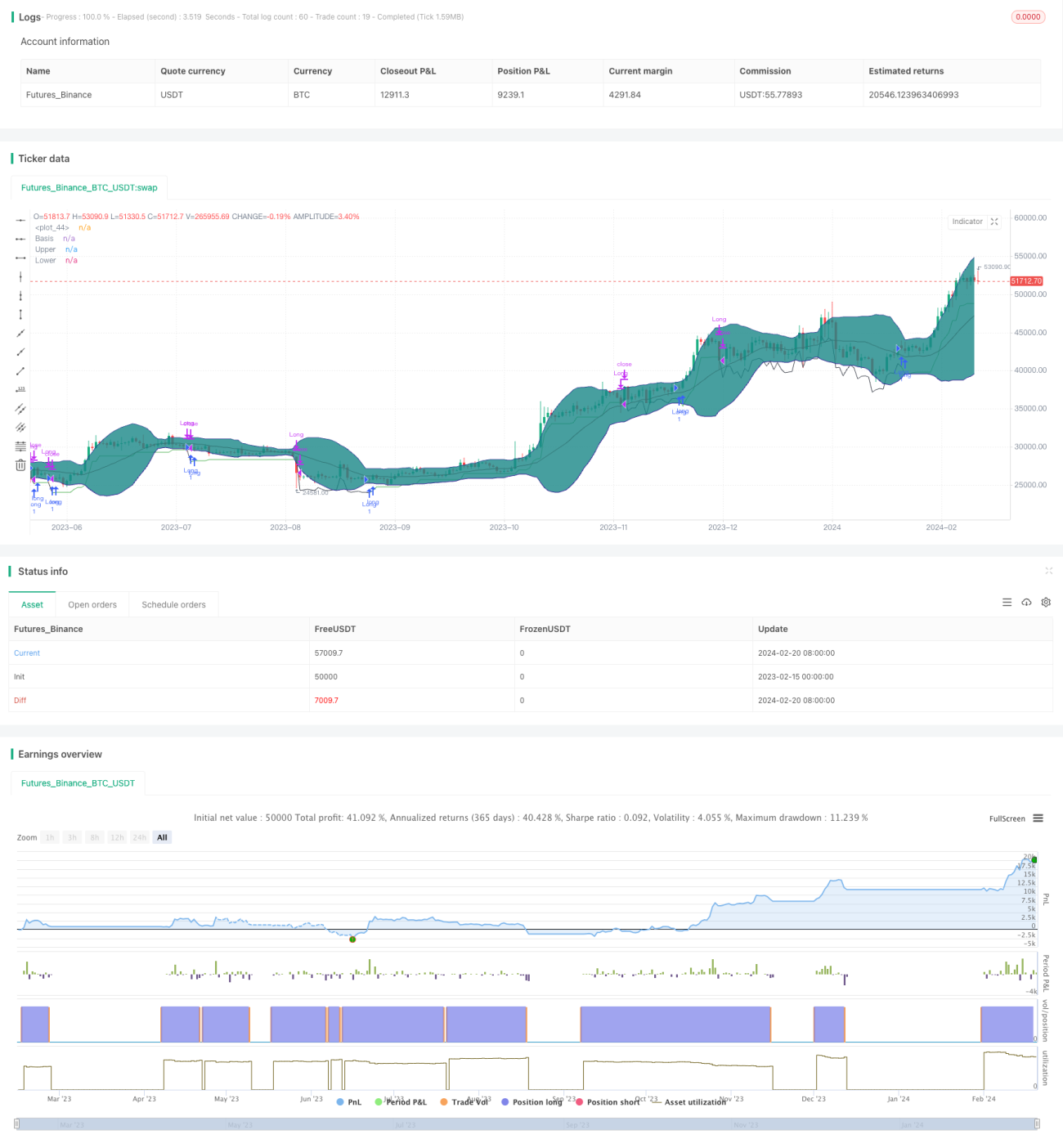

概要

ブロードバンド・レンジ・ロック戦略は、ボリンジャーバンドを用いて市場のボラティリティ低下を判断する長期ブレイクアウト戦略です。相場が揉み合い(レンジ相場)に入るとボリンジャーバンドの上限線と下限線が収縮します。このタイミングをエントリーチャンスと見なします。同時に、平均真実レンジ(ATR)を使用して価格のボラティリティ低下を確認します。

戦略の原理

本戦略は主にボリンジャーバンドを用いて価格が低ボラティリティのレンジ相場に入ったかどうかを判断します。ボリンジャーバンドの中央線は終値の移動平均線であり、上限線と下限線はそれぞれ中央線から標準偏差の2倍分上下にシフトしています。価格のボラティリティが低下すると、上限線と下限線の間隔が顕著に狭まります。ボリンジャーバンドの収縮を最初に判断する際、現在のATR値がボリンジャーバンドの上限線と下限線の間の標準偏差よりも小さいかどうかをチェックします。これは、価格がちょうどレンジ相場に入ったことを示します。

ボラティリティ低下をさらに確認するため、ATR値の移動平均線が下降トレンドを示しているかどうかを確認します。平均ATRの値が低下していることも、ボラティリティが低下していることを裏付けます。上記2つの条件が同時に満たされた場合、ボリンジャーバンドが明らかに収縮したと判断し、絶好の買いタイミングとみなします。

買いエントリー後は、ATR値の2倍を損切り幅とするトレーリングストップ戦略を採用します。これにより損失を効果的に制御できます。

優位性分析

本戦略の最大の利点は、市場が低ボラティリティのレンジ相場に入ったタイミングを正確に判断し、最適な買いタイミングを特定できる点にあります。他の長期戦略と比較して、ブロードバンド・レンジ・ロック戦略は利益を得る確率が高くなります。

次に、本戦略はトレーリングストップを活用してリスクを積極的に管理します。これにより、相場が不利に動いた場合でも損失を最小限に抑えることができます。これは多くの長期戦略に欠けている点です。

リスク分析

主なリスクは、ボリンジャーバンドが価格のボラティリティ変化を100%正確に判断できるわけではないことです。ボリンジャーバンドがボラティリティ低下を誤って判断した場合、買いタイミングが不利になる可能性があります。その際にはトレーリングストップが重要な役割を果たし、早期に損切りして撤退できます。

また、戦略における各種パラメータの設定も結果に影響を与えます。戦略をより堅牢にするためには、大量のバックテストを通じてパラメータを最適化する必要があります。

最適化の方向性

ボリンジャーバンドの収縮時に、トレンド系指標にも転換の兆しが現れたことを確認するための他の指標を追加することを検討できます。例えば、ボリンジャーバンドが収縮する際に、MACDの差がプラスからマイナスに転換したことや、RSIが買われ過ぎゾーンから下降したことなどを同時に要求することで、買いタイミングの精度をさらに高めることができます。

もう一つの方向性は、ボリンジャーバンドの期間、ATRの期間、トレーリングストップ倍率など、さまざまなパラメータが結果に与える影響をテストすることです。ステップ最適化を用いて最適なパラメータセットを見つける必要があります。

まとめ

ブロードバンド・レンジ・ロック戦略は、ボリンジャーバンドを用いて価格のボラティリティ低下のタイミングを判断し、トレーリングストップでリスクを効果的に管理する、比較的安定した長期ブレイクアウト戦略です。戦略の堅牢性を高めるためには、さらなるパラメータ最適化や他の指標の組み合わせが必要です。

- 1