モメンタム追跡とトレンド戦略に基づく

1

Follow

1802

Followers

概要

本戦略の核となる考え方は、スーパートレンド指標と平均方向性指数(ADX)を組み合わせることで、トレンドの判断と追跡を実現することです。スーパートレンド指標は現在の価格トレンドの方向を識別するために使用され、ADXはトレンドの強さを判断するために用いられ、強いトレンド下でのみ取引を行います。さらに、ローソク足の実体の色や出来高指標なども確認に利用し、比較的完成度の高い取引ルールを形成しています。

全体的に、本戦略はトレンドフォロー戦略に分類され、中長期的な明確なトレンドを捉えることを目的とし、レンジ相場やもみ合いによるノイズを回避します。

戦略の原理

- スーパートレンド指標を使用して価格トレンドの方向を判断します。価格がスーパートレンドを上抜けた場合はロングシグナル、下抜けた場合はショートシグナルとなります。

- ADXを使用してトレンドの強さを判断します。ADXが設定した閾値を超えた場合のみ取引シグナルを生成することで、方向感の乏しいレンジ相場をフィルタリングします。

- ローソク足の実体の色で現在が上昇局面か下落局面かを判断し、スーパートレンド指標と組み合わせて確認を行います。

- 出来高の増加も確認シグナルとして利用します。出来高が上昇している場合にのみポジションを構築します。

- ストップロスとテイクプロフィットを設定し、利益を確定するとともにリスクを管理します。

- 設定した取引時間の終了前に全てのポジションを決済します。

戦略の利点

- 中長期的な明確なトレンドを追跡し、もみ合い相場を回避することで、高い勝率を得られます。

- 戦略のパラメータが少なく、理解と実装が容易です。

- リスク管理が適切に行われており、ストップロスとテイクプロフィットが設定されています。

- 複数の指標で確認を行うため、偽のシグナルを低減できます。

戦略のリスク

- 市場全体の大幅な調整時に大きな損失が発生する可能性があります。

- 個別銘柄の業績変化により急激な反転が生じる可能性があります。

- 政策面での大きな変化(ブラックスワンイベント)が発生する可能性があります。

リスクへの対応方法

- ADXのパラメータを適切に調整し、強いトレンド下でのみ取引するようにします。

- ストップロスの幅を広げ、1回の損失をコントロールします。

- 政策や重要イベントを常に注視し、必要に応じて自主的にストップロスを実行します。

戦略の最適化方向性

- 異なるスーパートレンドのパラメータ組み合わせをテストし、より安定したシグナルを生成するパラメータを選択できます。

- ADXの異なるパラメータをテストし、最適なパラメータの組み合わせを決定できます。

- ボラティリティやボリンジャーバンドなどの他の指標を追加して確認を行うことで、偽シグナルをさらに低減できます。

- ブレイクアウト戦略などと組み合わせ、トレンドが崩れた際に迅速にストップロスを実行できます。

まとめ

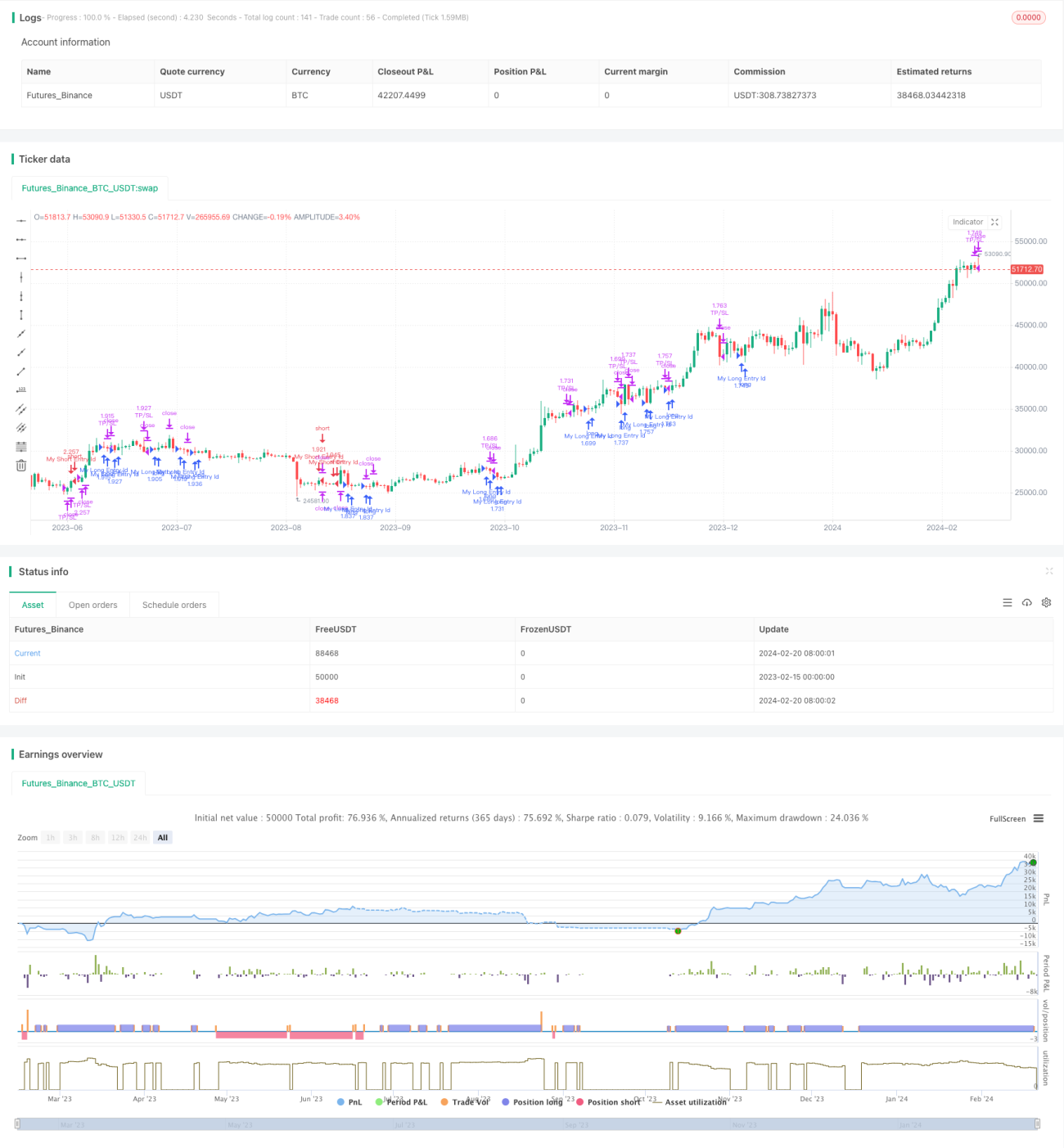

本戦略は全体的な考え方が明確であり、スーパートレンドで価格トレンドの方向を判断し、ADXでトレンドの強さを判断し、強いトレンド下でトレンドフォローを行います。同時にストップロスとテイクプロフィットを設定してリスクを管理します。戦略のパラメータが少なく、最適化が容易です。シンプルで効果的なトレンド戦略を学ぶための良い例となります。今後はパラメータ最適化やシグナルフィルタリングなどの方法でさらに改善することができます。

Source

Pine

/*backtest

start: 2023-02-15 00:00:00

end: 2024-02-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//Intraday Strategy Template

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © vikrisStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1