RSIとボリンジャーバンドの二重戦略

1

Follow

1802

Followers

概要

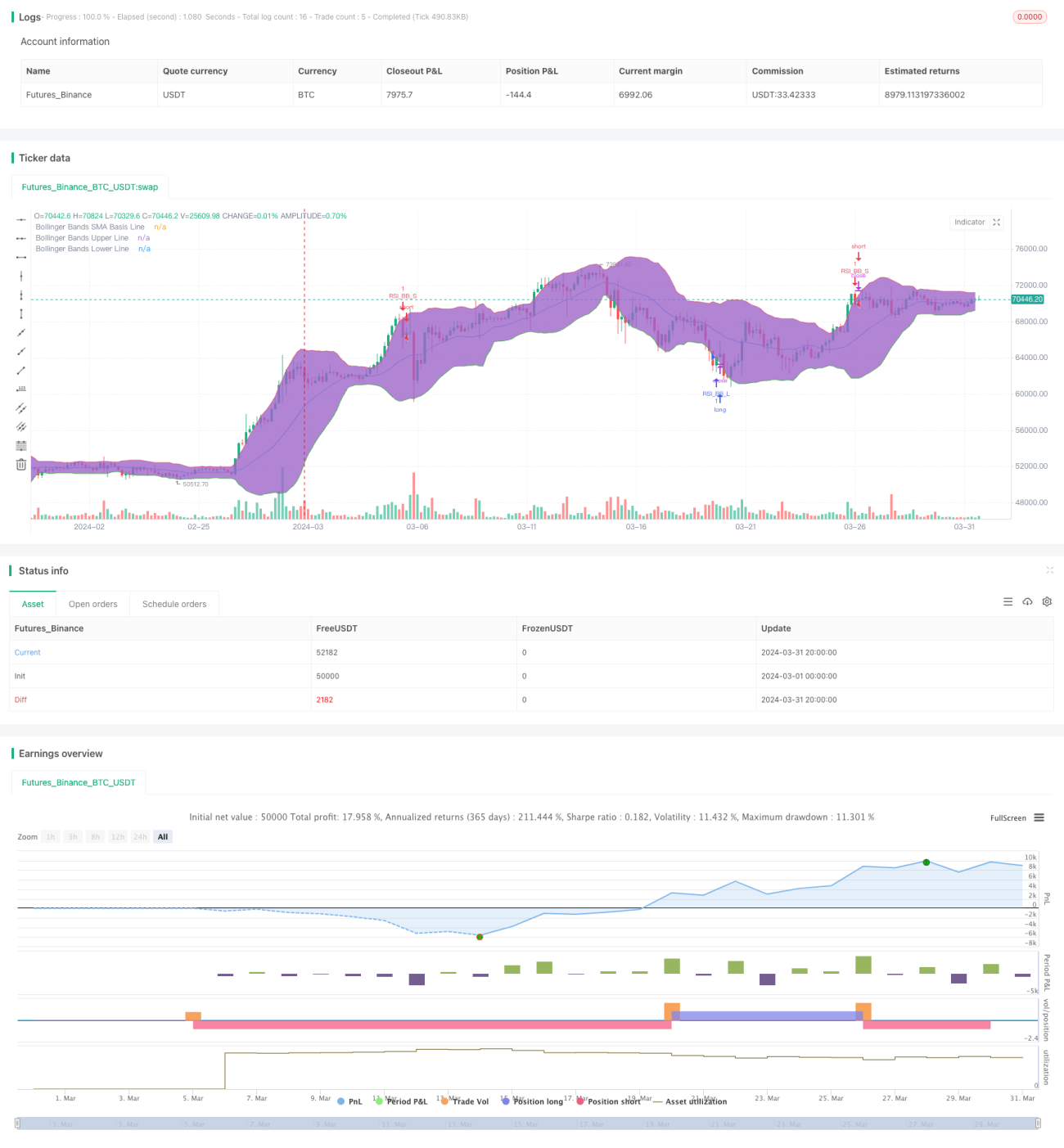

本戦略は、相対力指数(RSI)とボリンジャーバンド(Bollinger Bands)の2つのテクニカル指標を組み合わせたもので、価格がボリンジャーバンドの下限を下回ったときに買いシグナル、上限を上回ったときに売りシグナルを生成します。RSI指標とボリンジャーバンド指標が同時に売られ過ぎまたは買われ過ぎの状態にある場合にのみ取引シグナルがトリガーされます。

戦略の原理

- 設定されたRSIパラメータに基づいてRSI値を計算します。

- ボリンジャーバンドの計算式を用いて、中央値、上限、下限を算出します。

- 現在の終値がボリンジャーバンドの上限または下限を突破したかどうかを判定します。

- 現在のRSI値が買われ過ぎの閾値を上回っているか、売られ過ぎの閾値を下回っているかを判定します。

- ボリンジャーバンドとRSIの両指標が同時に買いまたは売りの条件を満たした場合、対応する取引シグナルを生成します。

戦略の利点

- トレンドとモメンタムの2つのテクニカル指標を組み合わせることで、より総合的に市場の状態を判断できます。

- 2つの指標をフィルター条件として同時に使用することで、偽シグナルの発生確率を効果的に低減します。

- コードのロジックが明確で、パラメータ設定も柔軟なため、様々な市場環境や取引スタイルに適応できます。

戦略のリスク

- レンジ相場では、本戦略で多くの損失取引が発生する可能性があります。

- パラメータの設定が適切でないと戦略のパフォーマンスが低下するため、実際の状況に応じた最適化が必要です。

- 本戦略にはストップロスが設定されていないため、大きなドローダウンリスクに直面する可能性があります。

戦略の最適化方向

- 市場の特性や個人の好みに応じて、RSIとボリンジャーバンドのパラメータを最適化できます。

- MACDや移動平均線などの他のテクニカル指標を導入し、シグナルの信頼性を高めます。

- 適切なストップロスとテイクプロフィットを設定し、一取引あたりのリスクをコントロールします。

- レンジ相場では、判断条件を追加したりポジションサイズを小さくすることで、頻繁な取引によるコストを低減することを検討できます。

まとめ

RSIとボリンジャーバンドのダブル戦略は、トレンドとモメンタム指標を組み合わせることで、市場の状態を比較的総合的に判断し、対応する取引シグナルを提供します。ただし、レンジ相場でのパフォーマンスが低下する可能性があり、リスク管理措置が設定されていないため、実運用には注意が必要です。パラメータの最適化、他の指標の導入、適切なストップロスとテイクプロフィットの設定などにより、本戦略の安定性と収益性をさらに向上させることができます。

Source

Pine

/*backtest

start: 2024-03-01 00:00:00

end: 2024-03-31 23:59:59

period: 4h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("Bollinger + RSI, Double Strategy (by ChartArt) v1.1", shorttitle="CA_-_RSI_Bol_Strat_1.1", overlay=true)

// ChartArt's RSI + Bollinger Bands, Double Strategy - UpdateStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1