평균 회귀 모멘텀 전략

개요

평균회귀 모멘텀 전략은 단기 가격 평균을 추적하는 추세 추종 거래 전략입니다. 평균회귀 지표와 모멘텀 지표를 결합하여 시장의 중기 추세를 판단합니다.

전략 원리

이 전략은 먼저 가격의 평균회귀선과 표준편차를 계산합니다. 그런 다음 Upper Threshold와 Lower Threshold 매개변수로 설정된 임계값을 결합하여 가격이 평균회귀선에서 표준편차 하나 범위를 벗어났는지 계산합니다. 벗어나면 거래 신호가 생성됩니다.

매수 신호의 경우 가격이 평균회귀선보다 표준편차 하나 아래에 있어야 하며, 종가가 LENGTH 기간의 SMA 이평선 아래에 있고 TREND SMA 이평선 위에 있어야 합니다. 이 세 가지 조건을 모두 충족하면 매수 포지션을 진입합니다. 청산 조건은 가격이 LENGTH 기간의 SMA 이평선을 상향 돌파하는 것입니다.

매도 신호의 경우 가격이 평균회귀선보다 표준편차 하나 위에 있어야 하며, 종가가 LENGTH 기간의 SMA 이평선 위에 있고 TREND SMA 이평선 아래에 있어야 합니다. 이 세 가지 조건을 모두 충족하면 매도 포지션을 진입합니다. 청산 조건은 가격이 LENGTH 기간의 SMA 이평선을 하향 돌파하는 것입니다.

이 전략은 Percent Profit Target과 Percent Stop Loss를 동시에 결합하여 이익 실현 및 손절 관리를 구현합니다.

청산 방식은 이동평균선 돌파 또는 선형 회귀 돌파 중에서 선택할 수 있습니다.

매수 및 매도 양방향 거래, 추세 필터링, 이익 실현 및 손절 등의 조합을 통해 시장의 중기 추세를 판단하고 추적합니다.

전략 장점

-

평균회귀 지표는 가격이 가치 중심에서 이탈했는지 효과적으로 판단할 수 있습니다.

-

모멘텀 지표 SMA는 단기 시장 잡음을 필터링할 수 있습니다.

-

매수 및 매도 양방향 거래로 추세 기회를全方位로 포착할 수 있습니다.

-

이익 실현 및 손절 메커니즘으로 리스크를 효과적으로 관리할 수 있습니다.

-

선택 가능한 청산 방식으로 시장 환경에 유연하게 대응할 수 있습니다.

-

완전한 추세 거래 전략으로 중기 추세를 잘 포착합니다.

전략 리스크

-

평균회귀 지표는 매개변수 설정에 민감하며, 임계값 설정이 부적절하면 허위 신호가 발생할 수 있습니다.

-

큰 변동성 장세에서는 손절이 너무 빈번하게 발생할 수 있습니다.

-

횡보 추세에서는 거래 빈도가 너무 높아져 거래 비용과 슬리피지 리스크가 증가할 수 있습니다.

-

거래 종목의 유동성이 부족하면 슬리피지 관리가 이상적이지 않을 수 있습니다.

-

양방향 거래는 리스크가 크므로 신중한 자금 관리가 필요합니다.

매개변수 최적화, 손절 방식 조정, 자금 관리 등의 방법으로 이러한 리스크를 통제할 수 있습니다.

전략 최적화 방향

-

평균회귀 및 모멘텀 지표의 매개변수 설정을 최적화하여 다양한 종목 특성에 더 잘 맞도록 합니다.

-

추세 판단 지표를 추가하여 추세 식별 능력을 향상시킵니다.

-

손절 전략을 최적화하여 시장의 큰 변동에 더 잘 대응할 수 있도록 합니다.

-

포지션 관리 모듈을 추가하여 시장 조건에 따라 포지션 규모를 조정합니다.

-

최대 손실 제어, 순자산 곡선 제어 등 더 많은 리스크 관리 모듈을 추가합니다.

-

머신러닝 방법을 결합하여 전략 매개변수를 자동 최적화하는 방안을 고려합니다.

요약

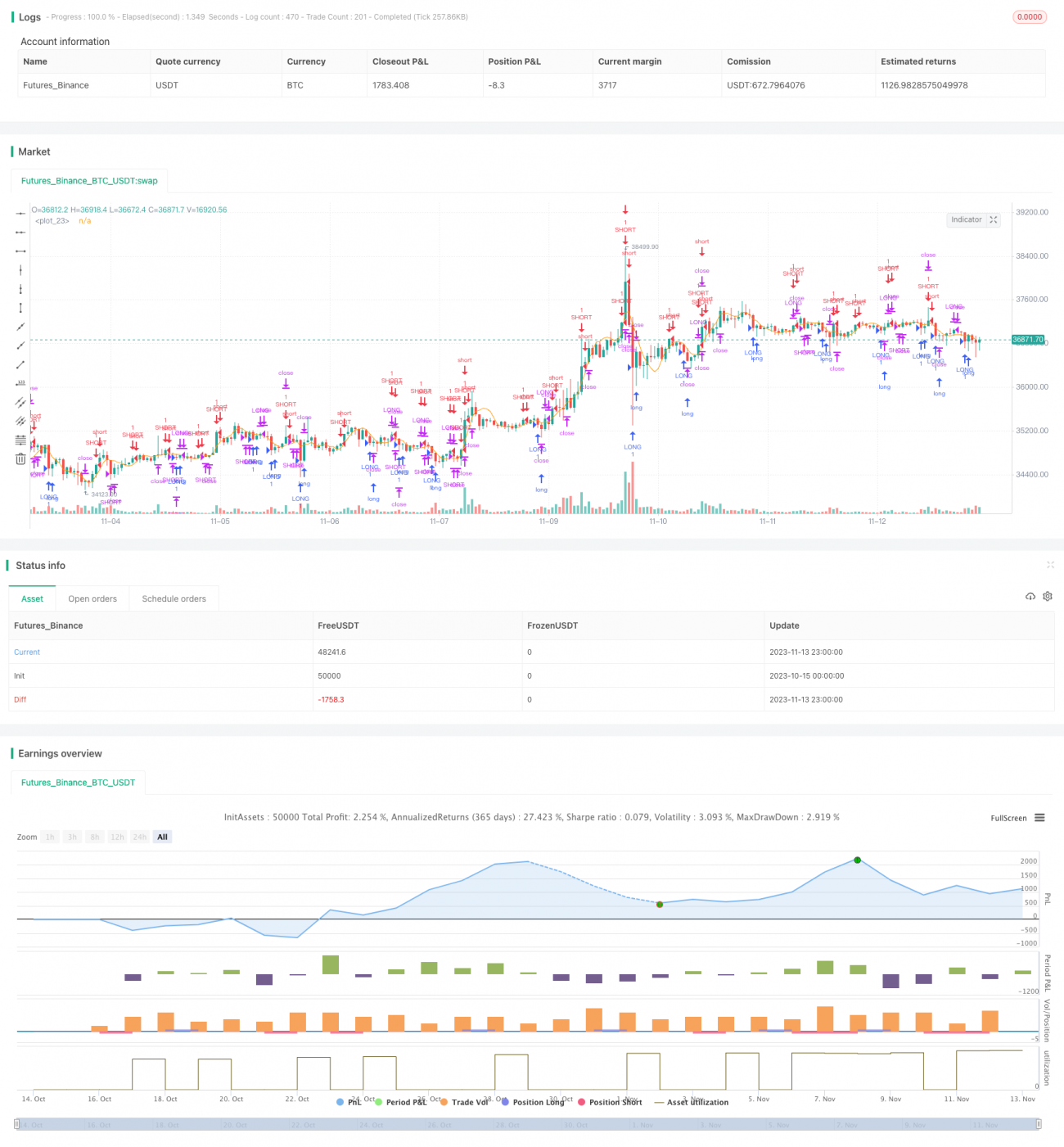

종합하면, 평균회귀 모멘텀 전략은 간단하고 효과적인 지표 설계를 통해 중기 가치 회귀 추세를 포착합니다. 이 전략은 적응성과 보편성이 높지만 일정한 리스크도 존재합니다. 지속적인 최적화와 다른 전략과의 결합을 통해 더 나은 성과를 얻을 수 있습니다. 이 전략은 전체적으로 완성도가 높으며 고려해볼 만한 추세 거래 방법입니다.

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1