지수 이동평균선 폐쇄 돌파 전략

개요

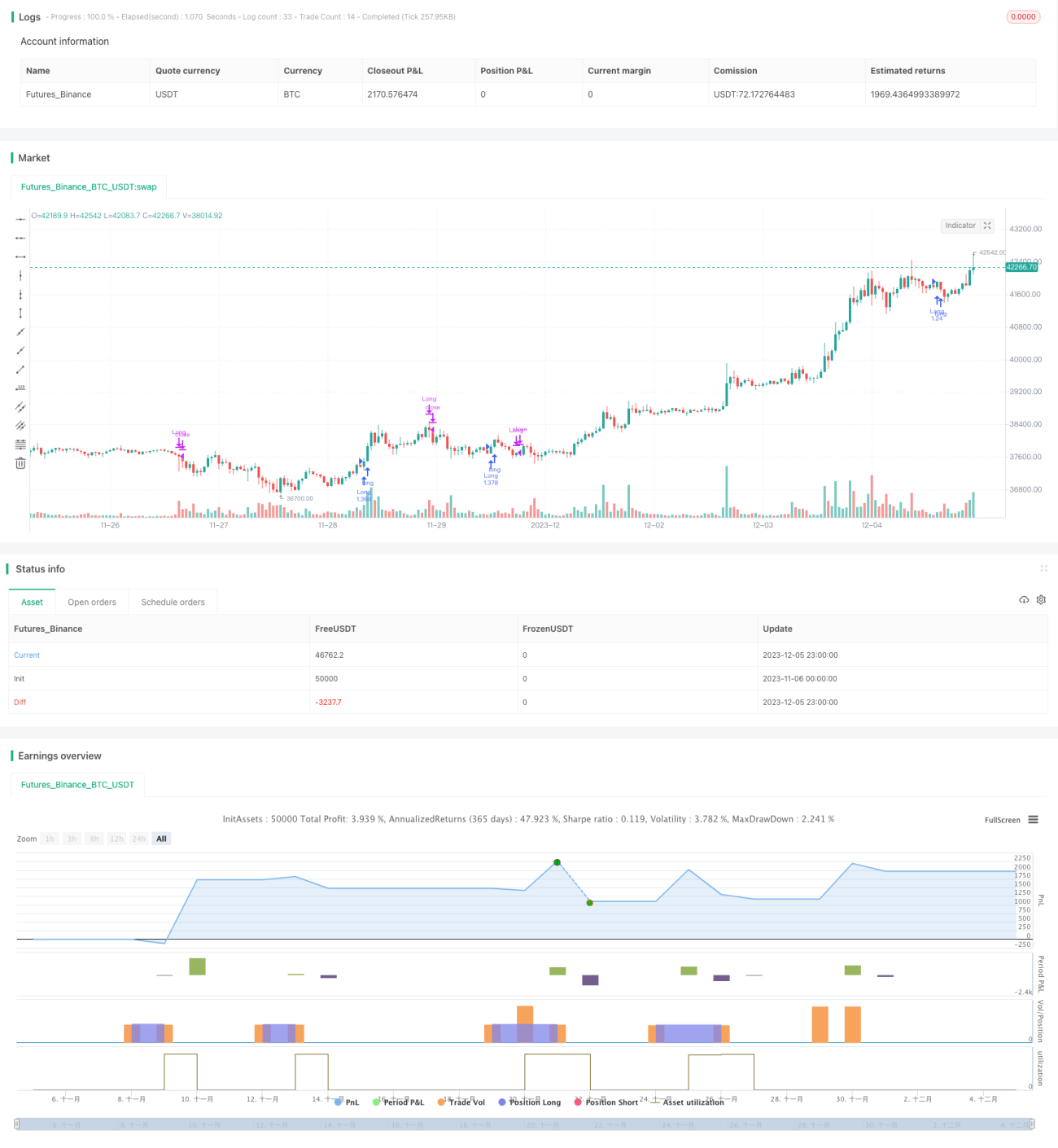

본 전략은 지수 이동 평균선의 방향을 판단하여 매수/매도 방향을 결정합니다. 양봉이 대체로 음봉을 잡아먹는 형태(양봉 대음봉)가 나타나고 거래량이 증가할 때 매수 진입합니다. 지수 이동 평균선의 방향이 전환되거나 음봉이 대체로 양봉을 잡아먹는 형태(음봉 대양봉)가 나타날 때 청산합니다.

전략 원리

-

서로 다른 파라미터를 가진 두 개의 지수 이동 평균선(EMA)을 사용하여 시장 추세 방향을 판단합니다. 단기 EMA가 장기 EMA 위에 있으면 상승장, 그 반대는 하락장으로 간주합니다.

-

시장이 상승장 상태일 때, 양봉이 이전 캔들을 대체로 잡아먹는 형태가 나타나고, 거래량이 이전 캔들보다 1.2배 이상이면 매수 신호가 발생합니다. 이 형태는 상승 힘이 강력하다는 것을 보여주며 추격 매수할 수 있습니다.

-

시장 추세가 전환되어 단기 EMA가 장기 EMA 아래로 하향 돌파하면 상승 힘이 약해진 것을 의미하므로 청산합니다. 또는 음봉이 대체로 양봉을 잡아먹는 형태가 나타나면 하락 힘이 강하게 유입되었음을 의미하므로 적극적으로 손절 청산합니다.

장점 분석

-

이중 EMA를 사용하여 시장 구조를 판단하므로 상승장/하락장 상태를 비교적 정확하게 판단할 수 있습니다.

-

잡아먹는 형태(Engulfing Pattern)는 한쪽 방향의 힘이 갑자기 강하게 유입되었음을 보여주므로 큰 움직임을 포착할 수 있습니다. 거래량 증가 필터를 결합하여 가짜 돌파로 인한 손실을 줄입니다.

-

손절 메커니즘이 있습니다. 손절가를 설정하지 않고 시장 구조 전환을 이용하여 손절하므로 불필요한 손절로 인한 슬리피지 손실을 줄일 수 있습니다.

리스크 분석

-

이중 EMA로 시장 구조를 판단할 때 오판하여 기회를 놓치거나 무분별하게 매수 진입할 수 있습니다. EMA 주기 파라미터를 적절히 조정할 수 있습니다.

-

잡아먹는 형태는 횡보장에서 오해를 불러일으키기 쉽습니다. 추가 필터 조건을 추가하여 오거래를 피할 수 있습니다.

-

손절가 설정이 없으면 더 큰 손실이 발생할 수 있습니다. 손익분기점(Break Even) 손절 등의 방법을 시도해 볼 수 있습니다.

최적화 방향

-

MACD, OBV(Energy Tide) 등 더 많은 지표를 결합하여 상승/하락을 판단할 수 있습니다.

-

적절한 폭의 손절가를 추가할 수 있습니다.

-

거래 상품 특성에 따라 EMA 주기 파라미터를 최적화할 수 있습니다.

요약

본 전략은 전체적인 아이디어가 명확하고 이해하기 쉽습니다. 지수 이동 평균선을 사용하여 구조를 판단하고, 잡아먹는 형태로 돌파를 포착합니다. 장점은 판단 로직이 단순하고 거래 신호가 명확하다는 점입니다. 하지만 갇힐 위험(손실 확대 위험)도 존재합니다. 추가 최적화를 통해 좋은 수익을 기대할 수 있습니다.

/*backtest

start: 2023-11-06 00:00:00

end: 2023-12-06 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// @version=5

// # ========================================================================= #

// # | STRATEGY |

// # ========================================================================= #- 1