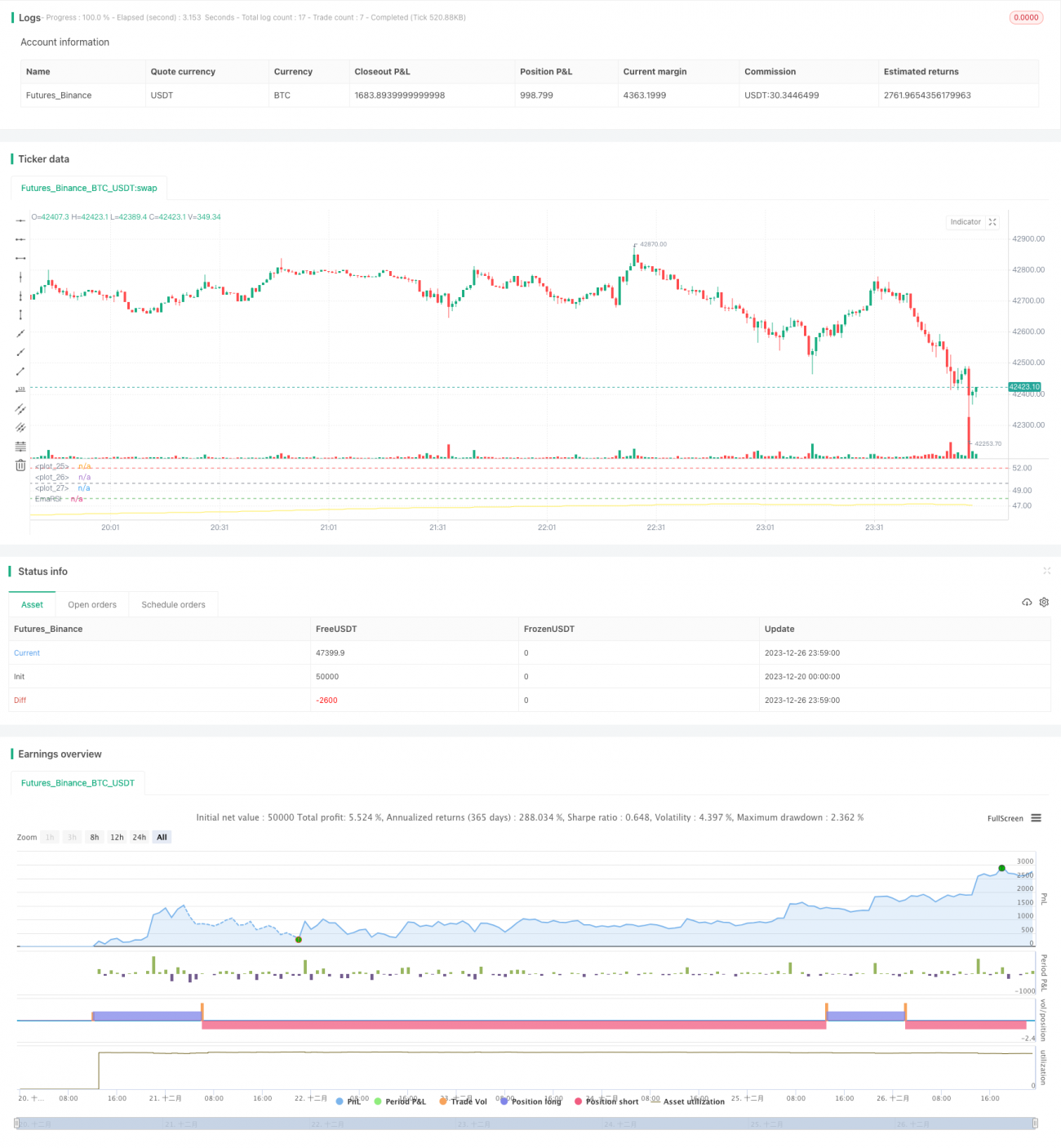

슬로우 RSI 과매수 과매도 전략

1

Follow

1802

Followers

개요

느린 RSI 과매수/과매도 전략은 RSI의 되돌아보기(回看) 기간을 연장하여 RSI 곡선의 변동성을 낮춤으로써 새로운 거래 기회를 창출합니다. 이 전략은 MACD 등 다른 기술적 지표에도 동일하게 적용 가능합니다.

전략 원리

이 전략의 핵심 아이디어는 RSI의 되돌아보기 기간을 기본 500주기로 연장한 후, SMA를 통해 RSI 곡선을 평활화하는 것입니다(기본 주기 250). 이를 통해 RSI 곡선의 변동성을 크게 낮추고 RSI의 반응 속도를 늦춰 새로운 거래 기회를 만들어냅니다.

너무 긴 되돌아보기 주기는 RSI 곡선의 변동성을 약화시키므로, 과매수/과매도 판단 기준도 조정이 필요합니다. 전략은 사용자 정의 과매수선 52와 과매도선 48을 설정합니다. 가중 RSI가 아래에서 과매도선을 돌파하면 매수 신호가 발생하고, 위에서 과매수선을 하향 돌파하면 매도 신호가 발생합니다.

전략 장점

- 혁신성이 뛰어나며, 주기 연장을 통해 새로운 거래 아이디어를 제시

- 허위 신호를 크게 줄이고 안정성을 높일 수 있음

- 과매수/과매도 임계값을 사용자 정의하여 다양한 시장에 대응 가능

- 포지션 분할 추가(播种加仓)를 통해 수익률 향상 가능

전략 위험

- 주기가 너무 길면 단기 기회를 놓칠 수 있음

- 진입 기회를 기다리는 인내심이 필요함

- 과매수/과매도 임계값 설정이 부적절하면 손실 증가 가능

- 차익거래(被套利) 위험이 존재함

해결 방법:

- 주기를 적절히 단축하여 거래 빈도 증가

- 분할 매수 방식으로 위험 분산

- 임계값 매개변수 최적화로 다양한 시장 환경에 대응

- 손절매 지점을 설정하여 큰 손실 방지

전략 최적화 방향

- RSI 매개변수 최적화를 통한 최적 주기 조합 탐색

- 다양한 SMA 평활화 주기 매개변수 테스트

- 과매수/과매도 매개변수 최적화로 다양한 시장에 적합하도록 조정

- 손절매 전략 추가로 단일 거래 손실 통제

요약

느린 RSI 과매수/과매도 전략은 주기 연장과 이동평균을 통한 변동성 억제 방식을 활용하여 성공적으로 새로운 거래 아이디어를 창출했습니다. 이 전략은 매개변수 최적화와 위험 관리가 적절히 이루어질 경우 안정적이고 효율적인 초과 수익을 기대할 수 있습니다. 전반적으로 이 전략은 높은 혁신성과 활용 가치를 지니고 있습니다.

Source

Pine

/*backtest

start: 2023-12-20 00:00:00

end: 2023-12-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// Wilder was a very influential man when it comes to TA. However, I'm one to always try to think outside the box.

// While Wilder recommended that the RSI be used only with a 14 bar lookback period, I on the other hand think there is a lot to learn from RSI if one simply slows down the lookback period

// Same applies for MACD.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1