선형 회귀 절편 기반 퀀트 전략

1

Follow

1802

Followers

개요

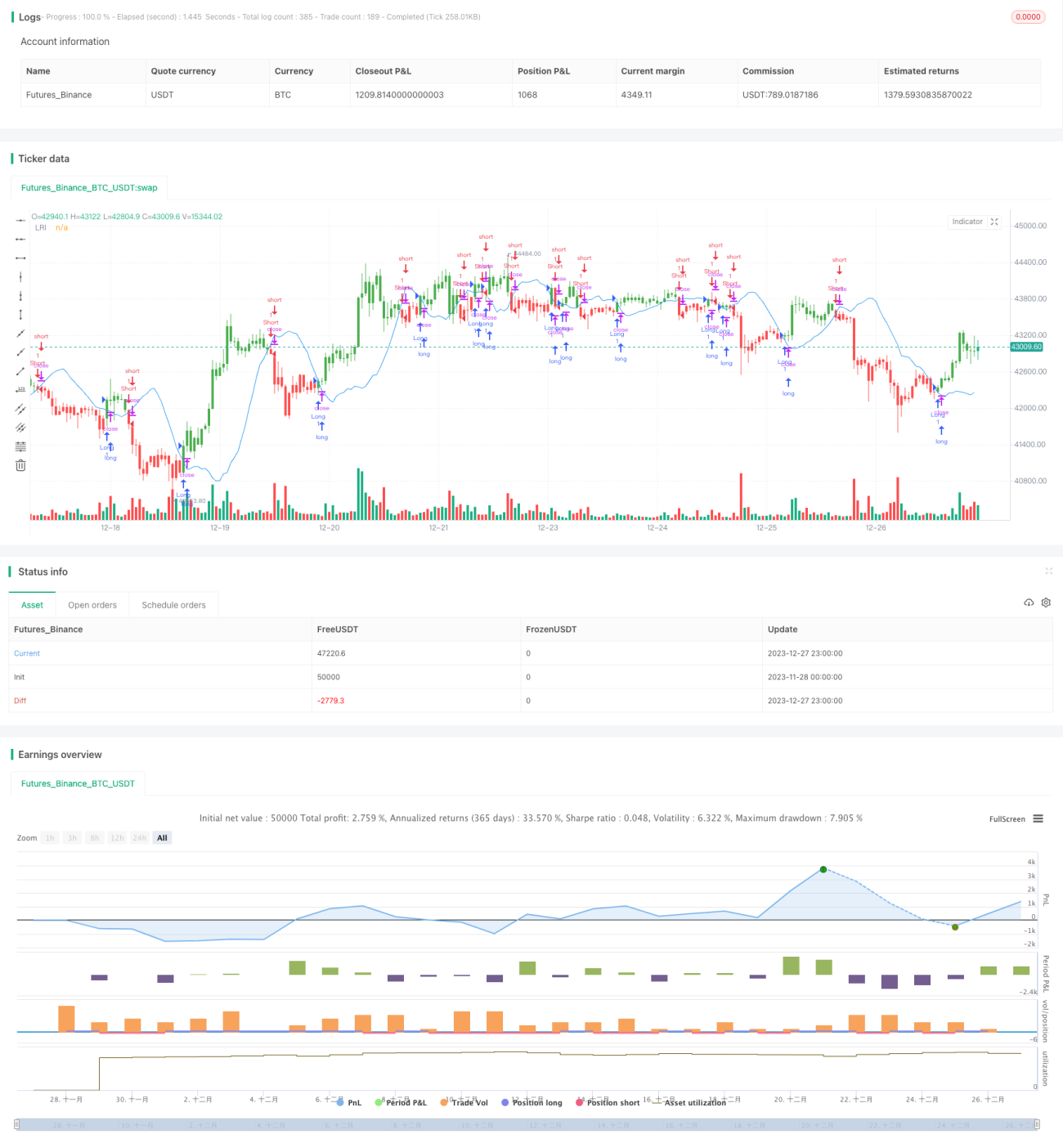

본 전략은 선형 회귀 기법을 사용하여 선형 회귀 절편점(Linear Regression Intercept)을 계산하고, 이를 매매 신호로 활용하여 퀀트 거래 전략을 구축합니다. 이 전략은 주가 시계열 데이터를 분석하여 선형 회귀 추세선을 적합하고, 선형 회귀 절편점을 사용하여 가격이 과대평가되었는지 또는 과소평가되었는지 판단하여 거래 신호를 생성합니다.

전략 원리

선형 회귀 절편점은 시간 시리즈 X 값이 0일 때 Y 값(일반적으로 가격)의 예측값을 나타냅니다. 이 전략은 사전에 설정된 매개변수 Length를 사용하여 종가를 소스 시퀀스로 삼아 최근 Length일 동안의 선형 회귀 절편점(xLRI)을 계산합니다. 종가가 xLRI보다 높으면 매수하고, 종가가 xLRI보다 낮으면 매도합니다.

구체적인 계산 공식은 다음과 같습니다:

xX = Length *(Length - 1)* 0.5

xDivisor = xX *xX - Length* Length *(Length - 1) *(2 * Length - 1) / 6

xXY = Σ(i * 종가[i]), i는 0부터 Length-1까지

xSlope = (Length *xXY - xX* Σ(종가, Length))/ xDivisor

xLRI = (Σ(종가, Length) - xSlope * xX) / Length

이러한 계산을 통해 최근 Length일의 선형 회귀 절편점 xLRI를 얻을 수 있습니다. 전략은 이를 바탕으로 가격의 고저를 판단하여 거래 신호를 생성합니다.

전략 장점

본 전략은 다음과 같은 장점을 가지고 있습니다:

- 선형 회귀 기법을 사용하여 가격에 대한 일정한 예측 능력과 추세 판단 능력을 제공합니다.

- 매개변수가 적고 모델이 단순하여 이해하고 구현하기 쉽습니다.

- 매개변수 Length를 사용자 정의하여 전략의 유연성을 조정할 수 있습니다.

위험 및 해결 방법

본 전략에는 몇 가지 위험도 존재합니다:

- 선형 회귀 적합은 단순히 과거 데이터를 기반으로 한 통계적 적합이므로, 미래 가격 움직임에 대한 예측 능력이 제한적입니다.

- 회사의 펀더멘털에 큰 변화가 발생할 경우 선형 회귀 적합 결과가 유효하지 않을 수 있습니다.

- 매개변수 Length 설정이 부적절하면 과적합이 발생할 수 있습니다.

대응 방안:

- 매개변수 Length를 적절히 줄여 과적합을 방지합니다.

- 회사의 펀더멘털 변화를 주시하고, 필요한 경우 수동으로 개입하여 포지션을 청산합니다.

- 적응형 매개변수 Length를 사용하여 시장 상황에 따라 동적으로 조정합니다.

전략 최적화 방향

본 전략은 다음과 같은 측면에서 추가로 최적화할 수 있습니다:

- 손절매 메커니즘을 추가하여 단일 손실을 제어합니다.

- 다른 지표와 결합하여 복합 전략을 구성하고 안정성을 높입니다.

- 매개변수 적응 최적화 모듈을 추가하여 Length 매개변수가 동적으로 변화하도록 합니다.

- 포지션 크기 제어 모듈을 추가하여 과도한 거래를 방지합니다.

요약

본 전략은 선형 회귀 절편점을 기반으로 간단한 퀀트 거래 전략을 구축했습니다. 전반적으로 이 전략은 일정한 경제적 가치를 지니지만, 주의해야 할 몇 가지 위험도 존재합니다. 지속적인 최적화를 통해 전략의 안정성과 수익성을 더욱 개선할 수 있을 것으로 기대됩니다.

Source

Pine

/*backtest

start: 2023-11-28 00:00:00

end: 2023-12-28 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 21/03/2018

// Linear Regression Intercept is one of the indicators calculated by using the Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1