Strategi Momentum Regresi Min

Gambaran Keseluruhan

Strategi momentum pembalikan min adalah strategi perdagangan trend yang mengesan purata harga jangka pendek. Ia menggabungkan indikator pembalikan min dan indikator momentum untuk menilai arah aliran pasaran jangka sederhana.

Prinsip Strategi

Strategi ini terlebih dahulu mengira garisan pembalikan min harga dan sisihan piawai. Kemudian, dengan menggunakan ambang yang ditetapkan oleh parameter Upper Threshold dan Lower Threshold, ia mengira sama ada harga telah melebihi satu sisihan piawai dari garisan pembalikan min. Jika melebihi, isyarat perdagangan dihasilkan.

Untuk isyarat beli (long), harga perlu berada di bawah satu sisihan piawai dari garisan pembalikan min, harga Close lebih rendah daripada purata bergerak SMA tempoh LENGTH, dan lebih tinggi daripada purata bergerak TREND SMA. Apabila ketiga-tiga syarat dipenuhi, posisi beli dibuka. Syarat penutupan adalah apabila harga menembusi ke atas purata bergerak SMA tempoh LENGTH.

Untuk isyarat jual (short), harga perlu berada di atas satu sisihan piawai dari garisan pembalikan min, harga Close lebih tinggi daripada purata bergerak SMA tempoh LENGTH, dan lebih rendah daripada purata bergerak TREND SMA. Apabila ketiga-tiga syarat dipenuhi, posisi jual dibuka. Syarat penutupan adalah apabila harga menembusi ke bawah purata bergerak SMA tempoh LENGTH.

Strategi ini turut menggabungkan Percent Profit Target dan Percent Stop Loss untuk pengurusan ambil untung dan henti rugi.

Kaedah keluar (Exit) boleh dipilih sama ada melalui penembusan purata bergerak atau penembusan regresi linear.

Melalui gabungan perdagangan dua arah (beli dan jual), penapisan trend, ambil untung dan henti rugi, strategi ini berjaya menilai dan mengikuti arah aliran pasaran jangka sederhana.

Kelebihan Strategi

-

Indikator pembalikan min dapat menilai dengan berkesan sama ada harga telah menyimpang dari nilai pusat.

-

Indikator momentum SMA dapat menapis bunyi pasaran jangka pendek.

-

Perdagangan dua arah (beli dan jual) dapat menangkap peluang trend secara menyeluruh.

-

Mekanisme ambil untung dan henti rugi dapat menguruskan risiko dengan berkesan.

-

Kaedah keluar yang boleh dipilih membolehkan penyesuaian fleksibel terhadap persekitaran pasaran.

-

Strategi perdagangan trend yang lengkap, dapat menguasai trend jangka sederhana dengan baik.

Risiko Strategi

-

Indikator pembalikan min sensitif terhadap tetapan parameter; penetapan ambang yang tidak sesuai boleh menghasilkan isyarat palsu.

-

Dalam pasaran yang sangat berombak, henti rugi mungkin kerap berlaku.

-

Semasa pasaran tidak menentu (sideways), kekerapan perdagangan mungkin terlalu tinggi, meningkatkan kos urus niaga dan risiko gelinciran harga (slippage).

-

Apabila kecairan instrumen dagangan tidak mencukupi, kawalan gelinciran mungkin tidak optimum.

-

Perdagangan dua arah membawa risiko yang lebih besar, memerlukan pengurusan modal yang berhati-hati.

Risiko ini boleh dikawal melalui pengoptimuman parameter, pelarasan kaedah henti rugi, dan pengurusan modal.

Arah Pengoptimuman Strategi

-

Mengoptimumkan tetapan parameter indikator pembalikan min dan momentum agar lebih sesuai dengan ciri-ciri instrumen yang berbeza.

-

Menambah indikator penilaian trend untuk meningkatkan keupayaan mengenal pasti arah aliran.

-

Mengoptimumkan strategi henti rugi agar lebih tahan terhadap turun naik pasaran yang besar.

-

Menambah modul pengurusan saiz posisi (position sizing) berdasarkan keadaan pasaran.

-

Menambah lebih banyak modul kawalan risiko, seperti kawalan pengeluaran maksimum (maximum drawdown), kawalan keluk ekuiti, dan lain-lain.

-

Mempertimbangkan untuk menggabungkan kaedah pembelajaran mesin bagi membolehkan pengoptimuman parameter strategi secara automatik.

Ringkasan

Kesimpulannya, strategi momentum pembalikan min berjaya menangkap trend pembalikan nilai jangka sederhana melalui reka bentuk indikator yang ringkas dan berkesan. Strategi ini mempunyai kebolehsuaian dan kebolehgunaan yang tinggi, namun turut mengandungi risiko tertentu. Melalui pengoptimuman berterusan dan penggabungan dengan strategi lain, prestasi yang lebih baik boleh dicapai. Secara keseluruhan, strategi ini agak lengkap dan merupakan kaedah perdagangan trend yang patut dipertimbangkan.

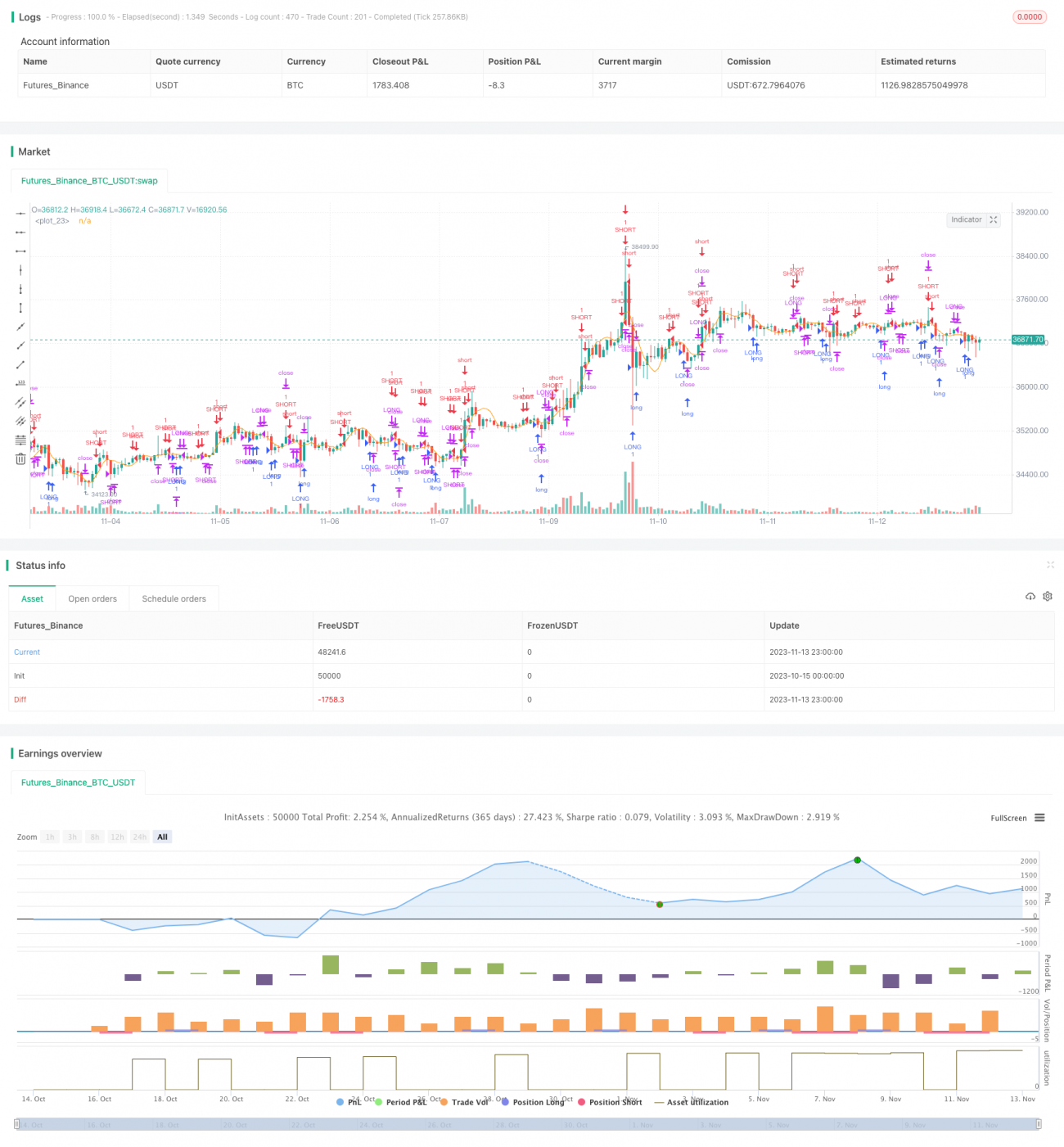

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1