Strategi Perdagangan Kuantitatif Berdasarkan Pelbagai Penunjuk

Gambaran Keseluruhan

Strategi ini membolehkan pembukaan dan penutupan automatik kedudukan beli dan jual dengan mengintegrasikan tiga penunjuk teknikal utama: Purata Bergerak, Indeks Kekuatan Relatif (RSI) dan MACD (Moving Average Convergence Divergence). Nama strategi mengandungi "Pelbagai Penunjuk" untuk menekankan penggunaan pelbagai penunjuk dalam strategi ini.

Prinsip Strategi

Strategi ini terutamanya menentukan arah aliran dengan membandingkan hubungan antara dua purata bergerak, dan menggabungkan penunjuk RSI untuk mengelakkan terlepas peluang pembalikan. Secara khusus, strategi menggunakan EMA atau SMA untuk mengira garis cepat dan garis perlahan. Apabila garis cepat melintasi ke atas garis perlahan, ia adalah isyarat beli; apabila garis cepat melintasi ke bawah garis perlahan, ia adalah isyarat jual. Untuk menapis penembusan palsu, strategi juga menetapkan logik beli/jual penunjuk RSI; isyarat dagangan hanya akan dijana apabila penunjuk RSI juga memenuhi syarat.

Selain itu, strategi juga mengintegrasikan penunjuk MACD untuk membuat keputusan dagangan. Apabila garis perbezaan MACD melintasi ke atas garis sifar, ia adalah isyarat beli; apabila garis perbezaan melintasi ke bawah garis sifar, ia adalah isyarat jual. Ini membolehkan penggunaan penunjuk MACD untuk menilai sama ada arah aliran telah berbalik, mengelakkan isyarat palsu pada titik perubahan arah aliran.

Analisis Kelebihan

Kelebihan terbesar strategi ini ialah keupayaannya untuk menapis isyarat melalui pelbagai penunjuk, dengan berkesan mengurangkan isyarat palsu dan meningkatkan kualiti isyarat. Secara khusus, kelebihan adalah seperti berikut:

-

Gabungan garis cepat/perlahan dengan penunjuk RSI dapat mengelakkan penembusan palsu yang terhasil daripada penggunaan tunggal purata bergerak.

-

Integrasi penunjuk MACD membolehkan penentuan awal sama ada arah aliran telah berbalik, mengelakkan isyarat palsu pada titik perubahan.

-

Membolehkan pemilihan penunjuk EMA atau SMA, menjadikan parameter penunjuk lebih sesuai untuk ciri pasaran yang berbeza.

-

Membolehkan pemilihan pelan pengurusan wang untuk mengawal saiz pesanan individu dan mengurus risiko dengan berkesan.

-

Menyokong stop loss dan take profit untuk mengunci keuntungan dan mengelakkan kerugian daripada melebar.

Analisis Risiko

Strategi ini terutamanya menghadapi risiko berikut:

-

Pengoptimuman parameter yang tidak sesuai boleh menyebabkan prestasi strategi yang lemah. Masa diperlukan untuk menguji kombinasi parameter yang berbeza.

-

Kebarangkalian penunjuk menjana isyarat palsu masih wujud. Apabila ketiga-tiga penunjuk menjana isyarat palsu pada masa yang sama, ia boleh menyebabkan kerugian yang besar.

-

Prestasi pada instrumen tunggal tidak stabil dan perlu diperluaskan kepada instrumen lain.

-

Data tidak mencukupi, keberkesanan strategi akan berkurangan pada masa hadapan.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari beberapa aspek berikut:

-

Menguji kombinasi parameter penunjuk yang berbeza untuk mencari parameter optimum.

-

Menambah mekanisme stop loss bergerak (trailing stop) dalam stop loss. Apabila harga bergerak pada jarak tertentu, trailing stop boleh digunakan untuk mengunci keuntungan.

-

Menambah penunjuk untuk menilai arah aliran utama bagi mengelakkan dagangan menentang arah aliran; contohnya, integrasi penunjuk ADX.

-

Tambah modul pengurusan wang untuk pengurusan risiko yang lebih baik.

-

Tambah penapis untuk faktor asas seperti berita.

Kesimpulan

Strategi ini mencari dan menapis kedudukan beli dan jual dengan mengintegrasikan pelbagai penunjuk teknikal seperti Purata Bergerak, RSI dan MACD. Kelebihannya ialah ia dapat menapis isyarat palsu dengan berkesan dan meningkatkan kualiti isyarat. Kelemahan utama ialah pemilihan parameter dan kebarangkalian penunjuk menjana isyarat palsu masih wujud. Arah pengoptimuman masa depan termasuk pengoptimuman parameter, pengoptimuman stop loss, penapisan arah aliran, dll. Secara keseluruhan, strategi ini berkesan sebagai rangka kerja strategi pelbagai penunjuk dan perlu terus dioptimumkan dan disahkan pada masa hadapan.

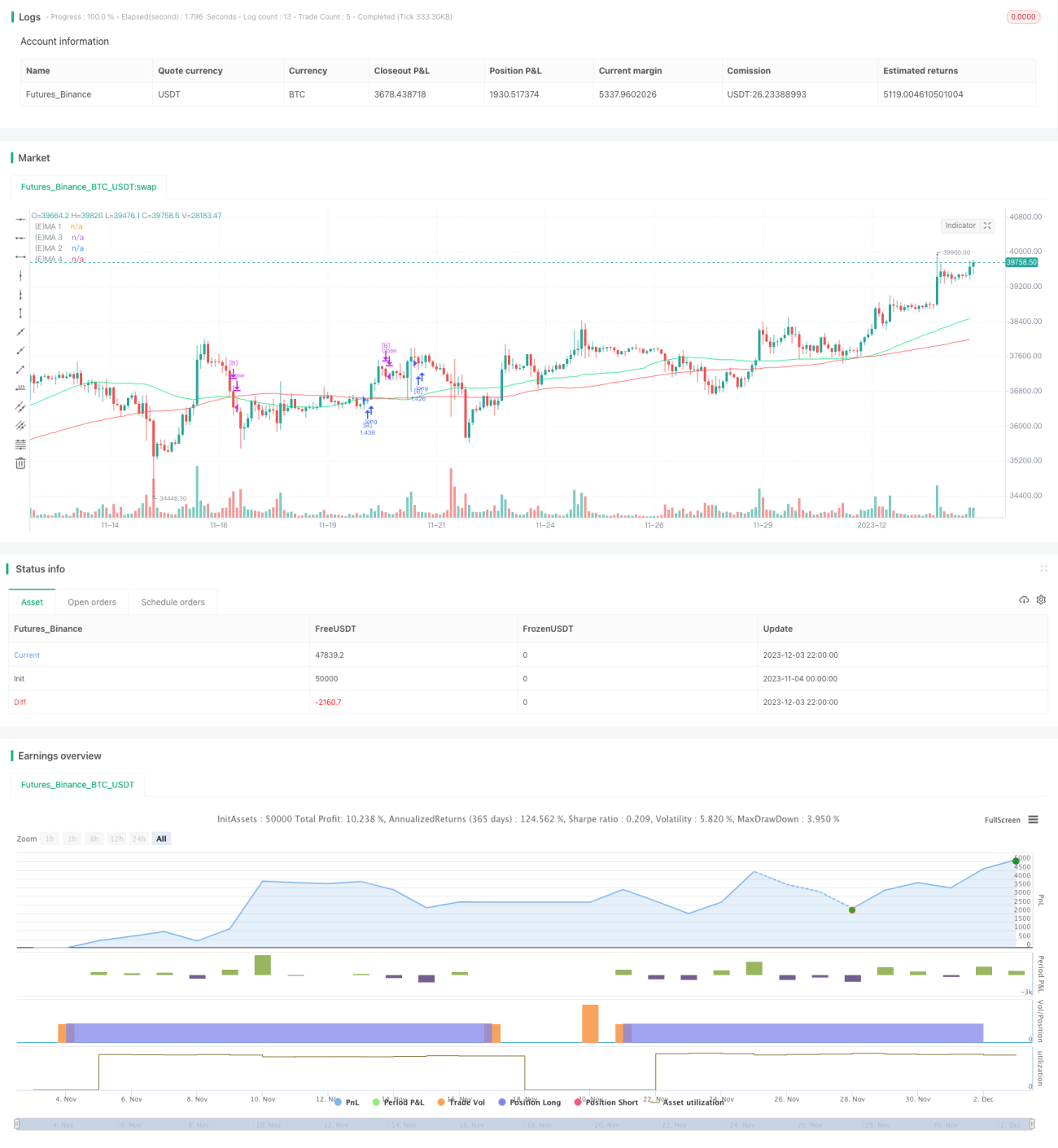

/*backtest

start: 2023-11-04 00:00:00

end: 2023-12-04 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fikira

//@version=4

strategy("Strategy Tester EMA-SMA-RSI-MACD", shorttitle="Strat-test", overlay=true, max_bars_back=5000, - 1