Estratégia Arco-Íris de Médias Móveis para Trading Automatizado Completo

Visão Geral

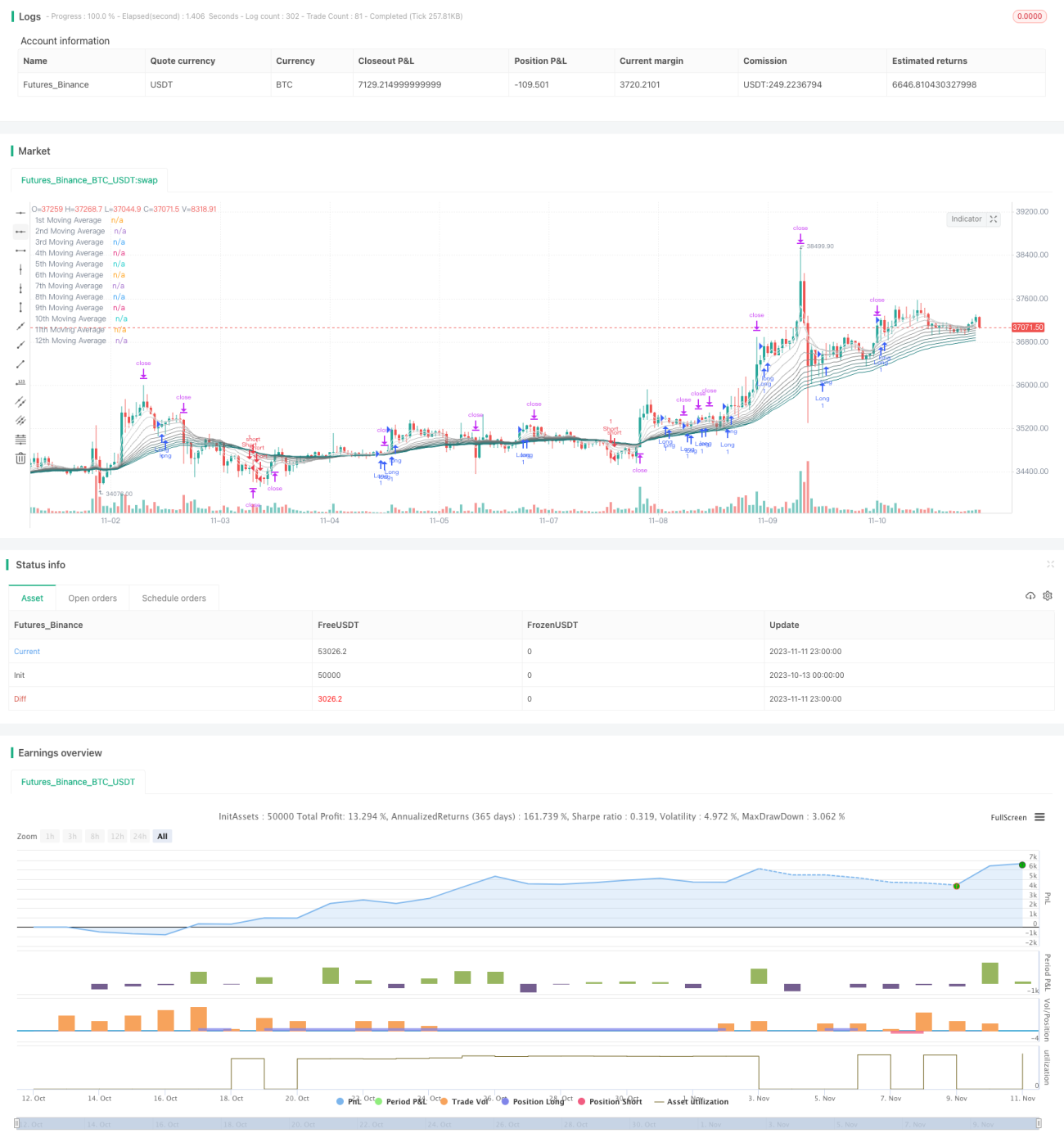

A Estratégia Arco-Íris de Médias Móveis para Negociação Automática Abrangente é uma estratégia típica de combinação de médias móveis de múltiplos períodos de tempo. Ela utiliza 12 médias móveis de diferentes períodos e determina a direção do movimento do mercado, bem como as condições de abertura de posição, stop loss e take profit com base na ordenação das médias móveis e na relação com o preço, permitindo a negociação automática. Esta estratégia pode identificar tendências automaticamente e possui um mecanismo completo de stop loss para controlar riscos.

Princípio

A estratégia utiliza 12 médias móveis, incluindo períodos de 3, 5, 8 até 55. Os tipos de média móvel podem ser selecionados entre EMA, SMA, RMA, etc. Primeiro, a estratégia avalia a relação de ordenação entre as médias móveis de curto prazo (linhas de 1 a 4 períodos) e as de longo prazo (linhas de 5 a 8 períodos). Se as de curto prazo estiverem acima, considera-se um ambiente de tendência de alta; se estiverem abaixo, um ambiente de tendência de baixa.

Em uma tendência de alta, se o preço ultrapassar a média móvel correspondente ao fundo anterior, considera-se um sinal de abertura de posição, realizando uma posição comprada. O stop loss é colocado na média móvel correspondente ao fundo anterior, e o take profit é definido a 1,6 vezes a distância do stop loss. Em uma tendência de baixa, se o preço ultrapassar a média móvel correspondente ao topo anterior, considera-se um sinal de abertura de posição, realizando uma posição vendida. O stop loss é colocado na média móvel correspondente ao topo anterior, e o take profit é definido a 1,6 vezes a distância do stop loss.

A estratégia também possui uma função de detecção de reversão de tendência. Durante a manutenção da posição, se a ordenação das médias móveis de curto prazo mudar e o preço ultrapassar o topo ou fundo mais recente, considera-se que pode ter ocorrido uma reversão de tendência. Nesse caso, a posição atual é encerrada e inverte-se para a posição oposta, utilizando o novo topo ou fundo como referência para stop loss e take profit.

Vantagens

-

A estratégia utiliza análise de múltiplos períodos de tempo de forma integrada, permitindo uma boa identificação da direção da tendência.

-

A estratégia incorpora a avaliação da ordenação convergente e divergente das médias móveis, evitando ser enganada por mercados oscilantes.

-

A estratégia possui um mecanismo completo de stop loss, capaz de controlar eficazmente o risco de cada operação.

-

A função de detecção de reversão de tendência permite capturar oportunidades de reversão em tempo hábil, reduzindo o risco sistêmico.

-

Os parâmetros da estratégia são flexíveis, permitindo personalizar períodos e tipos de médias móveis.

-

A estratégia utiliza stop loss móvel (trailing stop), garantindo a maximização dos lucros.

Riscos

-

A estratégia de combinação de múltiplas médias móveis tem seu desempenho afetado pela configuração dos parâmetros, necessitando de testes de otimização.

-

Em mercados oscilantes, as médias móveis podem gerar sinais falsos, sendo necessário ajustar os parâmetros ou evitar operar temporariamente.

-

Existe certo atraso, podendo haver o risco de perder oportunidades próximas aos pontos de reversão da tendência.

-

É necessário observar outros indicadores técnicos para evitar abrir posições vendidas próximas a níveis de suporte importantes.

-

O risco sistêmico deve ser monitorado, pois o mecanismo de detecção de reversão não o elimina completamente.

-

É necessário adicionar mecanismos extras para controle de drawdown, como o gerenciamento dinâmico de posição.

Direções de Otimização

-

Testar diferentes tipos de médias móveis e configurações de parâmetros para encontrar a melhor combinação.

-

Otimizar o mecanismo de detecção de reversão, definindo condições de ativação mais precisas.

-

Adicionar um mecanismo de gerenciamento dinâmico de posição, reduzindo o tamanho da posição quando o drawdown for excessivo.

-

Considerar a inclusão de algoritmos de aprendizado de máquina para treinar a identificação de pontos-chave com grandes volumes de dados.

-

Combinar sinais de outros indicadores para uma avaliação mais abrangente, melhorando a precisão das decisões.

-

Criar um portfólio de negociação com múltiplos ativos, utilizando correlações não relacionadas para diversificar o risco.

Conclusão

A Estratégia Arco-Íris de Médias Móveis para Negociação Automática Abrangente é, no geral, uma estratégia sólida de acompanhamento de tendências, com forte capacidade de identificação de tendências e controle de risco. Com otimizações adicionais, como ajuste de parâmetros e gerenciamento dinâmico de posição, pode se tornar uma estratégia de negociação quantitativa muito prática. Seu conceito é claro e de fácil compreensão, e ao mesmo tempo oferece flexibilidade, merecendo estudo aprofundado, uso e otimização contínua.

- 1