Estratégia de momentum com reversão à média

Visão Geral

A estratégia de momentum com regressão à média é uma estratégia de negociação de tendência que acompanha a média de curto prazo dos preços. Ela combina indicadores de regressão à média e de momentum para avaliar a tendência de médio prazo do mercado.

Princípio da Estratégia

A estratégia primeiro calcula a linha de regressão à média dos preços e o desvio padrão. Em seguida, combina os parâmetros de Limite Superior e Limite Inferior (Upper Threshold e Lower Threshold) predefinidos para verificar se o preço ultrapassou a linha de regressão à média por um desvio padrão. Se isso ocorrer, um sinal de negociação é gerado.

Para um sinal de compra, são necessárias três condições: o preço deve estar um desvio padrão abaixo da linha de regressão à média, o preço de fechamento (Close) deve estar abaixo da média móvel SMA do período LENGTH e acima da SMA de tendência (TREND SMA). Quando essas três condições são atendidas, uma posição longa é aberta. A condição de saída da posição longa é quando o preço cruza para cima a SMA do período LENGTH.

Para um sinal de venda, são necessárias três condições: o preço deve estar um desvio padrão acima da linha de regressão à média, o preço de fechamento (Close) deve estar acima da SMA do período LENGTH e abaixo da SMA de tendência (TREND SMA). Quando essas três condições são atendidas, uma posição curta é aberta. A condição de saída da posição curta é quando o preço cruza para baixo a SMA do período LENGTH.

A estratégia também combina Percentual de Lucro Alvo e Percentual de Stop Loss para gerenciar o take profit e o stop loss.

O método de saída pode ser escolhido entre a ruptura da média móvel ou a ruptura da regressão linear.

Através da combinação de negociações de ambos os lados (compra e venda), filtro de tendência, take profit e stop loss, a estratégia consegue avaliar e acompanhar a tendência de médio prazo do mercado.

Vantagens da Estratégia

-

O indicador de regressão à média pode avaliar efetivamente se o preço se desviou do valor central.

-

O indicador de momentum SMA pode filtrar o ruído de curto prazo do mercado.

-

Negociações de ambos os lados (long e short) permitem capturar oportunidades de tendência de forma abrangente.

-

O mecanismo de take profit e stop loss pode controlar efetivamente o risco.

-

O método de saída opcional permite adaptar-se de forma flexível às condições do mercado.

-

Estratégia de negociação de tendência completa, capaz de capturar adequadamente as tendências de médio prazo.

Riscos da Estratégia

-

O indicador de regressão à média é sensível à configuração de parâmetros; uma definição inadequada dos limites pode gerar sinais falsos.

-

Em mercados com grandes oscilações, o stop loss pode ser acionado com muita frequência.

-

Em mercados laterais (sem tendência clara), a frequência de negociações pode ser muito alta, aumentando os custos de transação e o risco de slippage.

-

Quando o ativo negociado tem baixa liquidez, o controle de slippage pode não ser ideal.

-

As negociações de ambos os lados apresentam maior risco, exigindo uma gestão de capital cuidadosa.

Esses riscos podem ser controlados através da otimização de parâmetros, ajuste das regras de stop loss e gerenciamento de capital.

Direções de Otimização da Estratégia

-

Otimizar os parâmetros dos indicadores de regressão à média e momentum para que se adequem melhor às características de diferentes ativos.

-

Adicionar indicadores de julgamento de tendência para melhorar a capacidade de identificar tendências.

-

Otimizar a estratégia de stop loss para que se adapte melhor a grandes flutuações do mercado.

-

Adicionar um módulo de gestão de posição para ajustar o tamanho da posição conforme as condições do mercado.

-

Adicionar mais módulos de controle de risco, como controle de rebaixamento máximo, controle do gráfico de patrimônio líquido, etc.

-

Considerar a combinação com métodos de aprendizado de máquina para otimizar automaticamente os parâmetros da estratégia.

Resumo

Em resumo, a estratégia de momentum com regressão à média utiliza um design de indicadores simples e eficaz para capturar a tendência de retorno ao valor médio no médio prazo. A estratégia possui boa adaptabilidade e universalidade, mas também apresenta certos riscos. Através de otimização contínua e combinação com outras estratégias, é possível obter um desempenho ainda melhor. A estratégia como um todo é bastante completa e representa um método de negociação de tendência que vale a pena considerar.

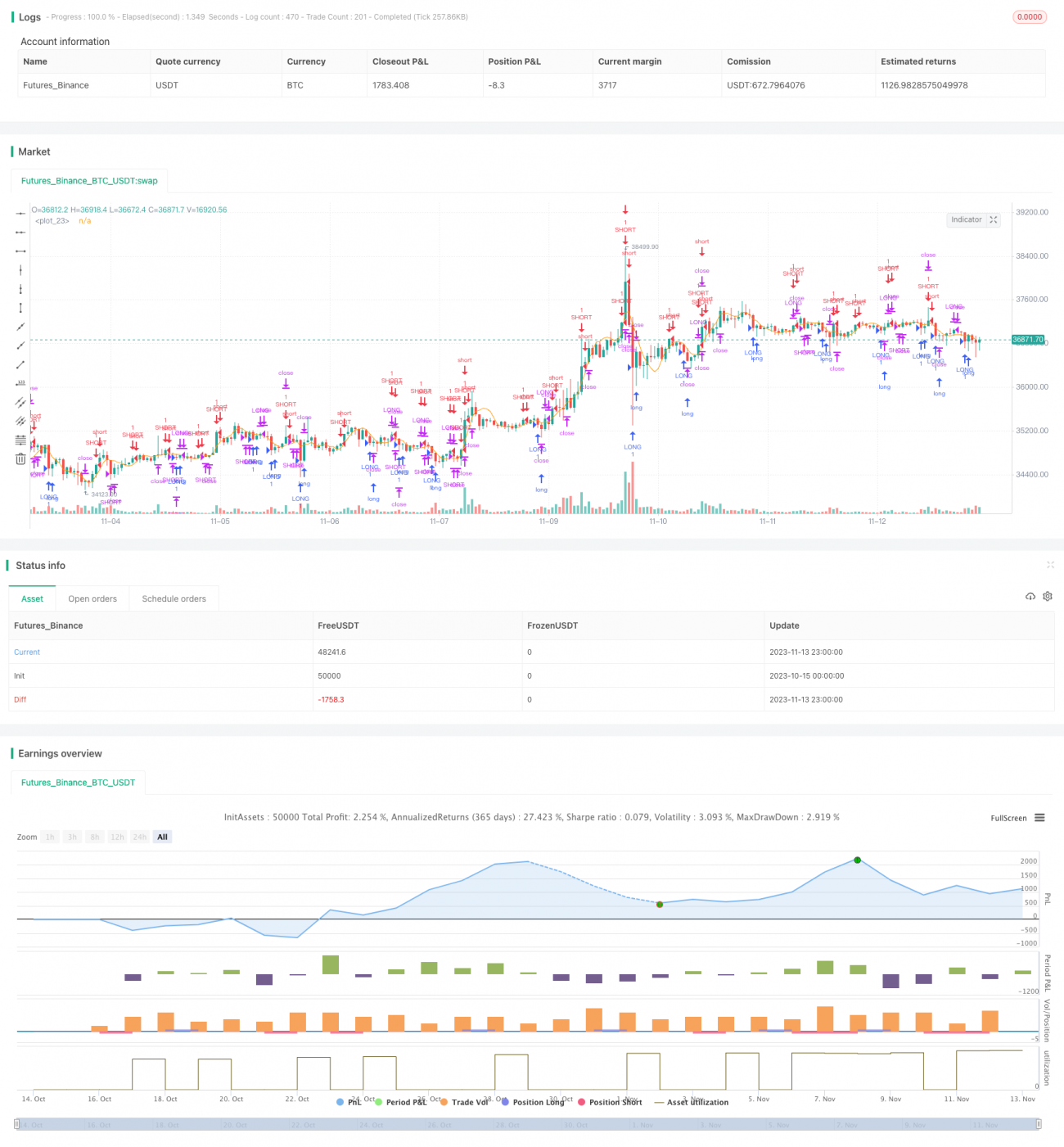

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1