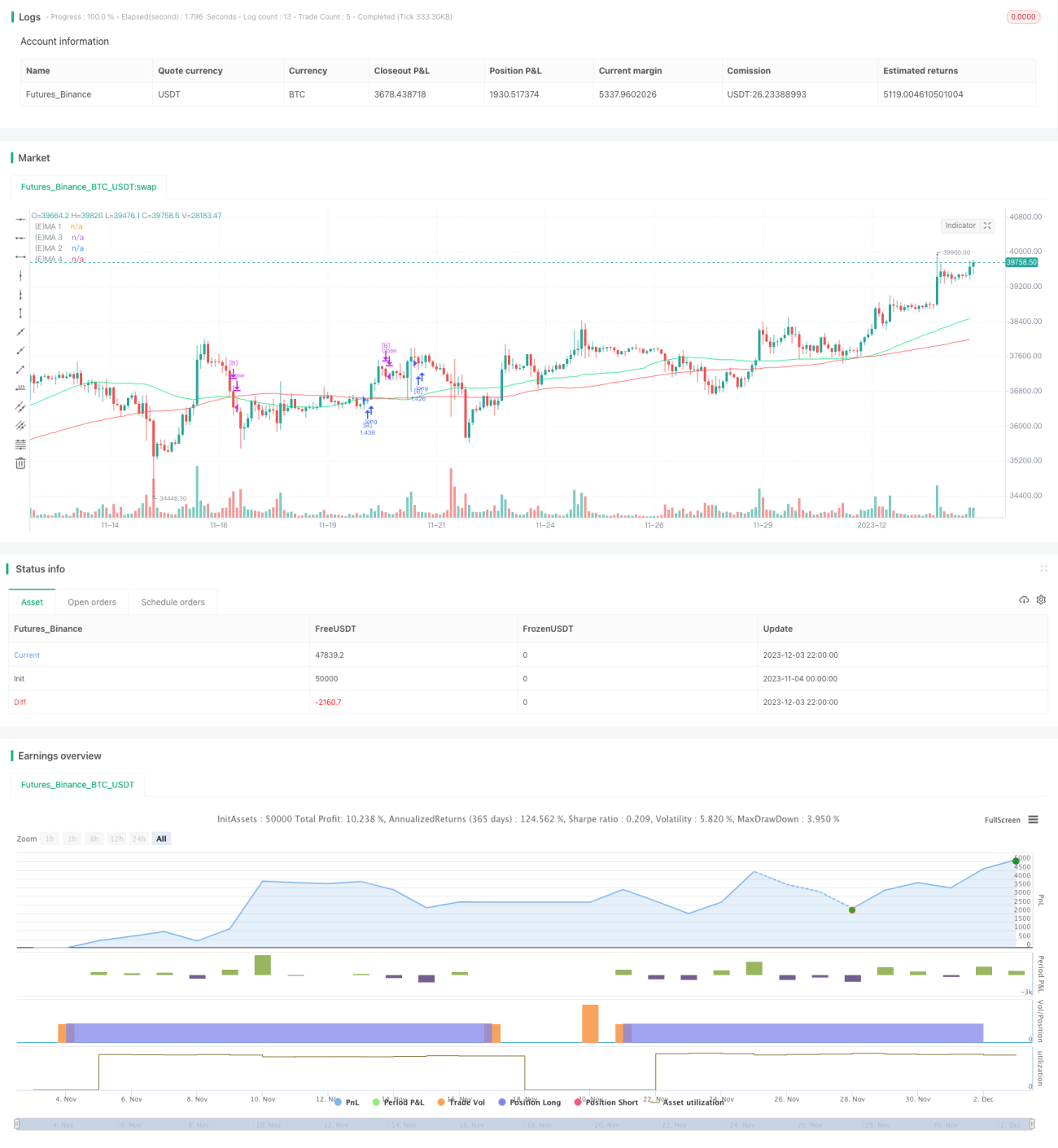

Estratégia de trading quantitativo baseada em múltiplos indicadores

Visão Geral

Esta estratégia realiza a abertura e fechamento automáticos de posições longas e curtas através da integração de três indicadores técnicos principais: Médias Móveis, Índice de Força Relativa (RSI) e MACD (Moving Average Convergence Divergence). O nome da estratégia contém "múltiplos indicadores" para destacar o uso de vários indicadores.

Princípio da Estratégia

A estratégia determina a direção da tendência comparando a relação entre duas médias móveis, combinando o RSI para evitar perder oportunidades de reversão. Especificamente, a estratégia calcula uma linha rápida e uma linha lenta usando EMA ou SMA. O cruzamento da linha rápida acima da linha lenta é um sinal de compra, e o cruzamento abaixo é um sinal de venda. Para filtrar falsos rompimentos, a estratégia também define a lógica de long/short do RSI: um sinal de negociação só é gerado quando o RSI também atende às condições.

Além disso, a estratégia integra o indicador MACD para decisões de negociação. Quando a linha de diferença do MACD cruza acima do eixo zero, é um sinal de compra; quando cruza abaixo, é um sinal de venda. Isso permite usar o MACD para identificar mudanças de tendência, evitando sinais errados em pontos de reversão.

Análise de Vantagens

A maior vantagem desta estratégia é a integração de múltiplos indicadores para filtrar sinais, reduzindo efetivamente sinais falsos e melhorando a qualidade dos sinais. Especificamente, as vantagens são:

-

A combinação de linhas rápida/lenta com o RSI evita falsos rompimentos gerados pelo uso isolado de médias móveis.

-

A integração do MACD permite identificar precocemente reversões de tendência, evitando sinais errados em pontos de inflexão.

-

Permite escolher entre EMA ou SMA, adaptando-se melhor a diferentes condições de mercado.

-

Oferece opções de gerenciamento de capital, controlando o tamanho de cada ordem e gerenciando riscos de forma eficaz.

-

Suporta stop loss e take profit, permitindo travar lucros e evitar ampliação de perdas.

Análise de Riscos

Os principais riscos enfrentados por esta estratégia são:

-

A otimização inadequada de parâmetros pode levar a resultados insatisfatórios. É necessário testar diferentes combinações de parâmetros.

-

A probabilidade de sinais errados dos indicadores ainda existe. Quando os três indicadores emitem sinais errados simultaneamente, podem ocorrer perdas significativas.

-

O desempenho em um único ativo não é estável, sendo necessário expandir para outros ativos.

-

Dados insuficientes podem fazer com que a eficácia da estratégia diminua no futuro.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

-

Testar diferentes combinações de parâmetros dos indicadores para encontrar os parâmetros ótimos.

-

Adicionar trailing stop no mecanismo de stop loss. Quando o preço se mover por uma certa distância, pode-se usar um trailing stop para travar lucros.

-

Adicionar indicadores de tendência de maior prazo para evitar negociações contra a tendência, como integrar o ADX.

-

Adicionar módulos de gerenciamento de capital para melhor gerenciamento de risco.

-

Adicionar filtros de fatores fundamentais, como notícias.

Resumo

Esta estratégia realiza a busca e filtragem de posições longas e curtas através da integração de múltiplos indicadores técnicos, como médias móveis, RSI e MACD. Sua vantagem está na filtragem eficaz de sinais falsos, melhorando a qualidade dos sinais. As principais desvantagens são a escolha de parâmetros e a probabilidade de sinais errados dos indicadores. As direções futuras de otimização incluem ajuste de parâmetros, otimização de stop loss, filtragem de tendência, etc. No geral, esta estratégia, como um framework de múltiplos indicadores, é eficaz e requer otimização e validação contínuas.

/*backtest

start: 2023-11-04 00:00:00

end: 2023-12-04 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fikira

//@version=4

strategy("Strategy Tester EMA-SMA-RSI-MACD", shorttitle="Strat-test", overlay=true, max_bars_back=5000, - 1