Estratégia de Negociação de Reversão TD de Momentum

Visão Geral

A Estratégia de Negociação de Reversão TD Momentum é uma estratégia quantitativa que utiliza o indicador TD Sequential para identificar sinais de reversão de preços. Baseada na análise de momentum de preços, a estratégia estabelece posições de compra ou venda após confirmar sinais de reversão.

Princípio da Estratégia

A estratégia utiliza o indicador TD Sequential para analisar as flutuações de preço e identificar padrões de reversão em 9 candles consecutivos. Especificamente, quando são identificados 9 candles consecutivos de alta seguidos por um candle de baixa, a estratégia sinaliza uma oportunidade de venda; inversamente, quando são identificados 9 candles consecutivos de baixa seguidos por um candle de alta, a estratégia sinaliza uma oportunidade de compra.

A vantagem do indicador TD Sequential é a capacidade de capturar sinais de reversão antecipadamente. Combinado com um mecanismo de acompanhamento de tendência (compra em alta, venda em baixa) presente na estratégia, é possível estabelecer posições de compra ou venda assim que a reversão é confirmada, obtendo boas entradas no início do movimento de reversão.

Análise de Vantagens

- Utiliza o indicador TD Sequential para identificar oportunidades de reversão antecipadamente

- Mecanismo de acompanhamento de tendência permite confirmação mais rápida da reversão

- Entrada durante a formação da reversão proporciona pontos de entrada mais favoráveis

Análise de Riscos

- O indicador TD Sequential pode gerar falsos rompimentos, sendo necessário confirmar com outros fatores

- É preciso controlar adequadamente o tamanho e o tempo das posições para reduzir riscos

Direções de Otimização

- Combinar com outros indicadores para confirmar sinais de reversão e evitar falsos rompimentos

- Estabelecer mecanismos de stop loss para limitar perdas individuais

- Otimizar o tamanho da posição e o período de holding para equilibrar lucro e controle de risco

Resumo

A Estratégia de Negociação de Reversão TD Momentum utiliza o indicador TD Sequential para prever reversões de preço e estabelece posições rapidamente após a confirmação. É uma estratégia muito adequada para traders de momentum. A estratégia possui a vantagem de identificar oportunidades de reversão, mas é necessário controlar os riscos para evitar perdas significativas devido a falsos rompimentos. Com otimizações adicionais, trata-se de uma estratégia de negociação com relação risco-retorno equilibrada.

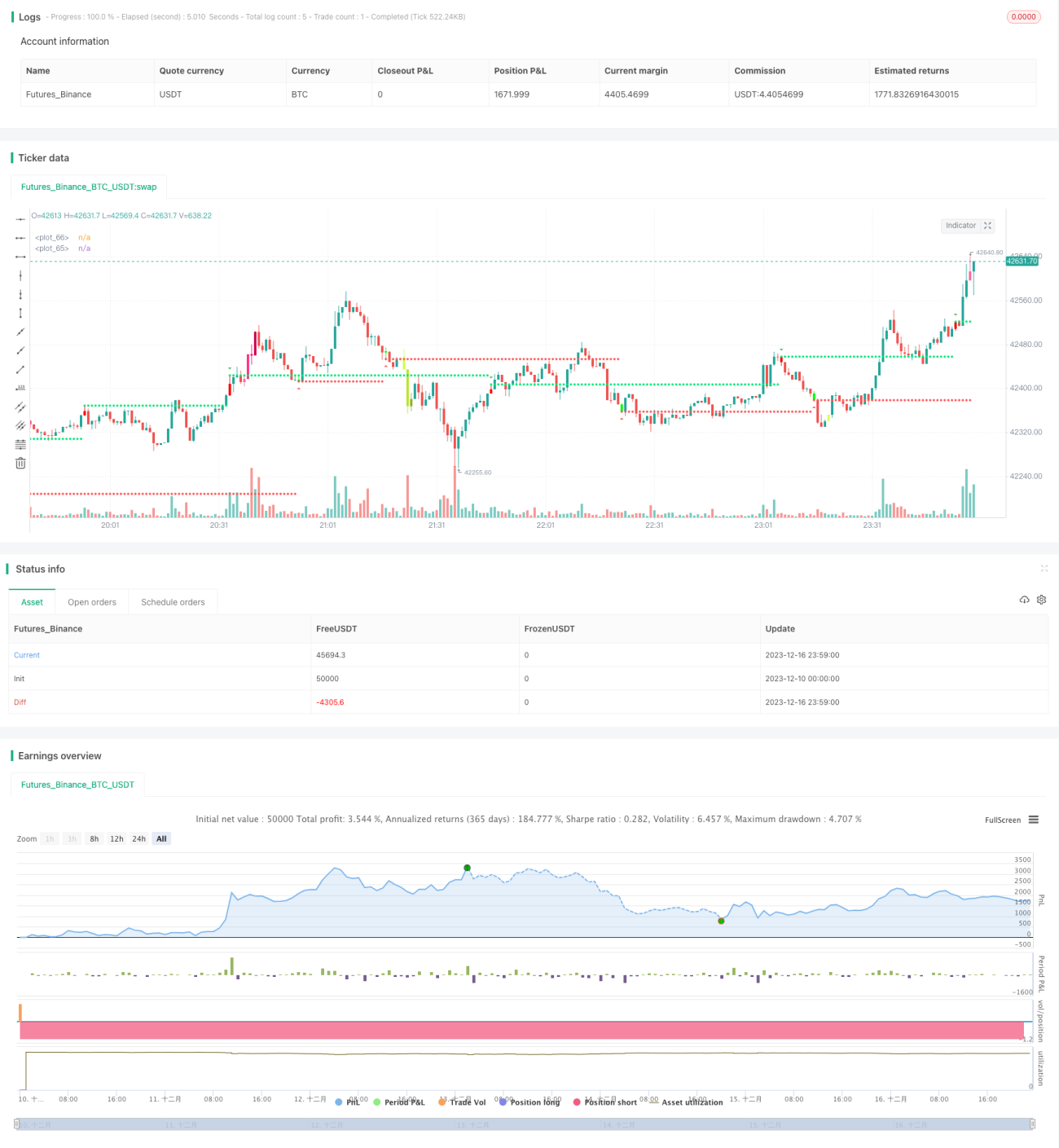

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//This strategy is based on TD sequential study from glaz.

//I made some improvement and modification to comply with pine script version 4.

//Basically, it is a strategy based on proce action, supports and resistance.- 1