Estratégia de Seguimento de Tendência com Bandas de Bollinger e Momentum

Visão Geral

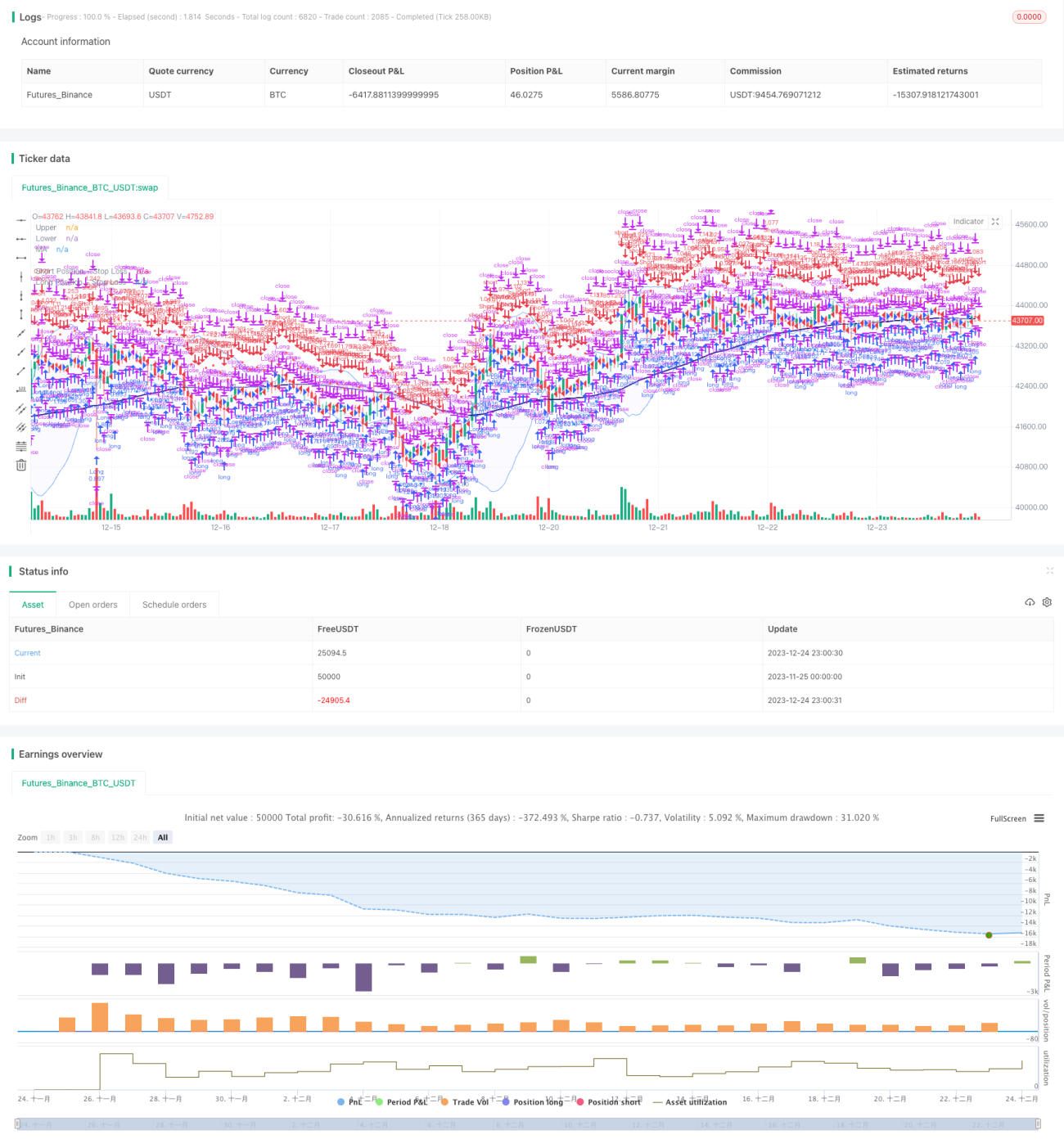

Esta estratégia implementa um robusto sistema de acompanhamento de tendências baseado nas Bandas de Bollinger, médias móveis e análise de volume. O objetivo é capturar possíveis reversões de tendência e aproveitar o momentum do mercado para obter lucros.

Princípios da Estratégia

Bandas de Bollinger

-

Utiliza as Bandas de Bollinger para identificar condições de sobrecompra e sobrevenda no mercado. A visualização clara das bandas superior e inferior auxilia na tomada de decisões.

-

O princípio básico das Bandas de Bollinger é calcular as bandas superior e inferior com base no preço médio e no desvio padrão durante um determinado período. Quando o preço ultrapassa a banda superior, há um sinal de sobrecompra; quando rompe a banda inferior, há um sinal de sobrevenda.

Filtro de Média Móvel

-

Implementa um filtro de média móvel para reforçar a identificação da tendência. O utilizador pode escolher diferentes tipos de médias móveis, como Média Móvel Simples, Média Móvel Exponencial e Média Móvel Ponderada.

-

Quando o preço cruza acima (abaixo) da média móvel, gera-se um sinal de compra (venda).

Análise de Volume

-

Permite integrar a análise de volume na estratégia para confirmação dos sinais. Barras de volume com cores diferentes indicam se o volume está acima ou abaixo da média.

-

Um volume que ultrapassa a média pode ser utilizado para confirmar os sinais de preço.

Análise de Vantagens

Estratégia Robusta de Acompanhamento de Tendências

-

Identifica reversões de tendência com base nas Bandas de Bollinger, médias móveis e volume.

-

É capaz de captar rapidamente a tendência dos preços e lucrar com o seu acompanhamento.

Flexibilidade e Personalização

-

O utilizador pode otimizar os parâmetros das Bandas de Bollinger, o tipo e o comprimento da média móvel.

-

As posições longas e curtas podem ser controladas separadamente.

Visualização e Confirmação

-

Duplo mecanismo de sinal: confirmação dos sinais de preço das Bandas de Bollinger através da média móvel e do volume.

-

Exibição intuitiva de sinais de negociação, como médias móveis e níveis de stop-loss.

Gestão de Risco

-

Calcula o nível de stop-loss com base no ATR. É possível personalizar o período do ATR e o multiplicador do stop-loss.

-

Ajusta o tamanho da posição de acordo com a percentagem de risco da posição. Controla eficazmente a perda por operação.

Análise de Riscos

Risco do Período de Backtest

- Diferentes períodos históricos podem influenciar o desempenho da estratégia. Devem ser realizados backtests em diferentes períodos para garantir a robustez da estratégia.

Risco de Reversão de Tendência

- Em mercados laterais, os stops podem ser acionados com frequência. Este risco pode ser reduzido através da otimização dos parâmetros da média móvel.

Risco de Sobre-otimização

- A otimização de múltiplos parâmetros pode levar a um sobre-ajuste. Devem ser utilizadas várias combinações de parâmetros e realizados testes de robustez.

Risco de Atraso dos Indicadores Técnicos

- O cálculo dos indicadores pode ter algum atraso. É necessário combinar com a ação do preço, não dependendo exclusivamente dos indicadores.

Direções de Otimização

Otimização de Parâmetros

- Otimizar os parâmetros das Bandas de Bollinger, o tipo de média móvel e os parâmetros do ATR para se adaptar a diferentes ativos e períodos.

Otimização da Posição

- Testar diferentes níveis de percentagem de risco da posição e otimizar o multiplicador do stop-loss.

Otimização dos Sinais

- Testar a adição de outros indicadores auxiliares para filtrar sinais, como KD, MACD, etc.

Otimização do Código

- Melhorar a lógica de decisão dos sinais para reduzir aberturas de posições desnecessárias. Utilizar programação orientada a objetos para aumentar a escalabilidade.

Resumo

Esta estratégia integra as Bandas de Bollinger, médias móveis e análise de volume para construir um sistema mecânico de acompanhamento de tendências. As principais vantagens são o mecanismo robusto de confirmação de sinais e o controlo de risco eficaz. Através da otimização de parâmetros e sinais, é possível melhorar a estabilidade e a rentabilidade da estratégia. Esta abordagem pode servir como referência metodológica para investidores que procuram surfar as tendências do mercado.

- 1