Estratégia de Negociação de Curto Prazo Baseada em Reversão de Médias Móveis

Visão Geral

A Estratégia de Média Móvel Reversa é uma estratégia de negociação de curto prazo baseada na reversão de médias móveis. Ela combina múltiplos indicadores como Bandas de Bollinger, RSI e CCI para capturar mudanças de curto prazo no mercado financeiro, com o objetivo de comprar na baixa e vender na alta.

Esta estratégia é principalmente utilizada em ativos de alta liquidez, como índices, câmbio e metais preciosos. Ela busca maximizar o lucro por operação, enquanto controla a relação risco-retorno geral da negociação.

Princípio da Estratégia

-

Usar as Bandas de Bollinger para identificar zonas de desvio de preço. Quando o preço se aproxima da banda superior, considera-se vender a descoberto; quando se aproxima da banda inferior, considera-se comprar.

-

Combinar com o indicador RSI para identificar se o ativo está sobrecomprado ou sobrevendido. O RSI pode efetivamente reconhecer situações de sobrecompra e sobrevenda.

-

O indicador CCI é usado para detectar sinais de reversão de preço. O CCI é sensível a situações anômalas e pode capturar oportunidades de reversão de preço de forma eficaz.

-

Quando o preço cruza acima da média móvel de 5 períodos, compra-se; quando cruza abaixo, vende-se a descoberto. A posição da média móvel representa a principal faixa de preço atual, e a relação entre preço e média reflete possíveis mudanças de tendência.

-

Após a confirmação do sinal de entrada, fechar rapidamente a posição para obter lucro. Definir uma saída de stop loss com base no drawdown para alcançar alta taxa de acerto.

Vantagens da Estratégia

- Combinação de múltiplos indicadores, aumentando a precisão dos sinais

A Estratégia de Média Móvel Reversa utiliza simultaneamente vários indicadores como Bandas de Bollinger, RSI e CCI. Esses indicadores são sensíveis a mudanças de preço, e sua combinação pode melhorar a precisão dos sinais, reduzindo sinais falsos.

- Regras rigorosas de entrada, evitando comprar na alta e vender na baixa

A estratégia exige que os sinais dos indicadores e o preço coincidam, evitando enganos de um único indicador. Também exige que o preço já tenha revertido claramente, reduzindo riscos relacionados.

- Mecanismo eficiente de stop loss, controlando perdas por operação

Seja comprando ou vendendo a descoberto, a estratégia define linhas de stop loss rigorosas. Uma vez que o preço ultrapasse a linha de stop loss em direção desfavorável, a estratégia interrompe rapidamente a perda, evitando grandes perdas individuais.

- Take profit razoável, buscando maximizar o lucro por operação

A estratégia define dois alvos de take profit, realizando lucros em etapas. Após o take profit, utiliza-se um ajuste fino de trailing stop para ampliar o espaço de lucro de cada operação.

Análise de Risco

- Flutuação violenta de preço, acionamento do stop loss

Em caso de flutuação violenta de preço, a linha de stop loss pode ser rompida, causando perdas desnecessárias. Isso geralmente ocorre em eventos importantes que causam oscilações anormais de preço.

Pode-se lidar com esse risco ampliando a margem do stop loss e evitando operar durante eventos importantes.

- Tendência de alta muito forte, sem reversão

Quando a tendência de alta é muito forte, o preço pode subir tão rápido que não consegue reverter a tempo. Nesse caso, se insistir em vender a descoberto, pode-se enfrentar o risco de comprar na alta e vender na baixa.

Nessa situação, deve-se aguardar, entrando apenas quando a força de alta diminuir claramente.

Direções de Otimização

- Otimizar parâmetros dos indicadores para melhorar a precisão dos sinais

Pode-se testar resultados de backtest com diferentes combinações de parâmetros para escolher os melhores. Por exemplo, otimizar os parâmetros do RSI, do CCI, etc.

- Combinar indicadores de volume para determinar o momento real da reversão

Pode-se adicionar indicadores de volume, como volume de negociação ou largura das Bandas de Bollinger. Isso evita gerar sinais falsos quando o preço apenas faz pequenos ajustes.

- Otimizar estratégias de take profit e stop loss para ampliar o lucro por operação

Pode-se testar diferentes pontos de take profit e stop loss para maximizar o lucro de cada operação. Também é necessário equilibrar o risco para evitar que o stop loss seja facilmente acionado.

Resumo

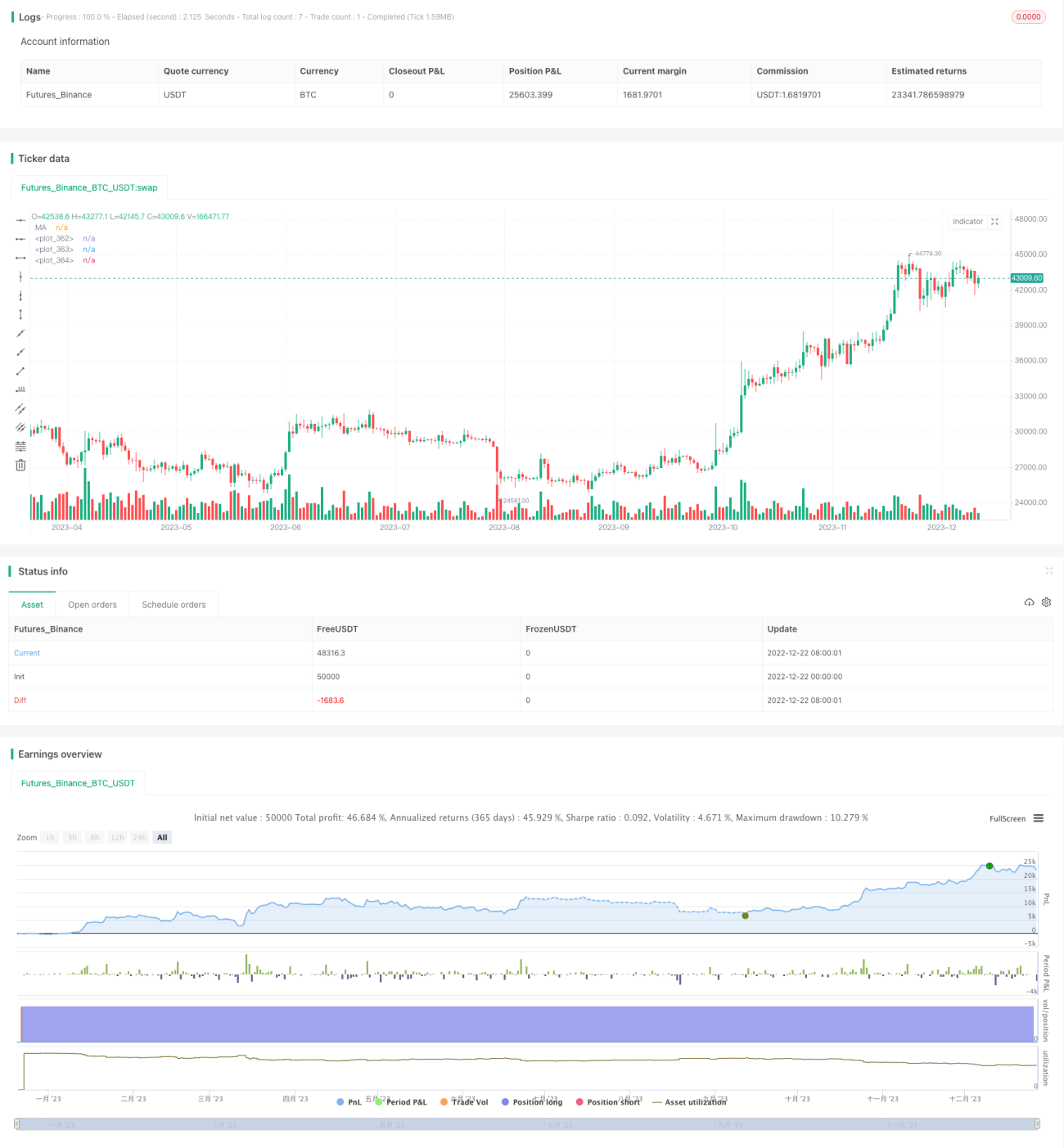

A Estratégia de Média Móvel Reversa utiliza de forma abrangente múltiplos indicadores para julgar, tendo características de sinais precisos, operação padronizada e risco controlável. É adequada para ativos com alta sensibilidade a mudanças de mercado e forte liquidez, capaz de capturar oportunidades de reversão entre as Bandas de Bollinger e a média móvel chave, alcançando o objetivo de comprar na baixa e vender na alta.

Na aplicação prática, ainda é necessário prestar atenção à otimização dos parâmetros dos indicadores, combinando indicadores de volume para julgar o momento real da reversão. Além disso, deve-se gerenciar bem o risco em flutuações violentas de preço. Se usado corretamente, a estratégia pode obter retornos Alpha relativamente estáveis.

- 1