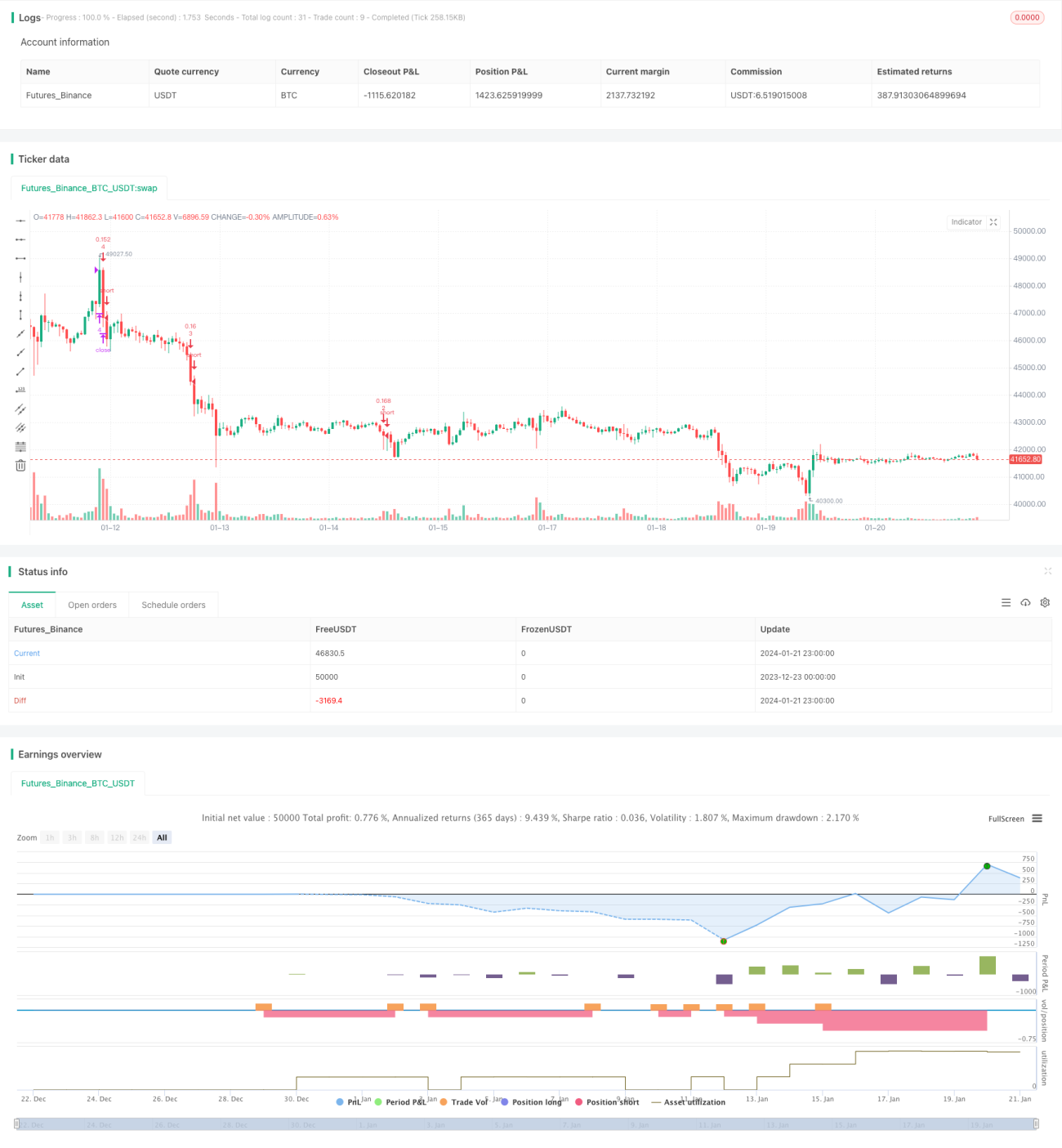

Baseado em estratégia de trading de grade dinâmica

1

Follow

1802

Followers

Visão Geral

Esta estratégia realiza trading em grade colocando múltiplas ordens de compra e venda paralelas dentro de uma faixa de preços, ajustando a faixa da grade e as linhas de acordo com a volatilidade do mercado para obter lucros.

Princípio da Estratégia

- Definir os limites superior e inferior da grade, que podem ser definidos manualmente ou calculados automaticamente com base nos preços mais altos e mais baixos do período recente.

- Calcular a largura do intervalo da grade de acordo com o número de grades definido.

- Gerar um array de preços com o número correspondente de linhas de grade.

- Quando o preço estiver abaixo de uma determinada linha de grade, abrir uma ordem de compra abaixo dessa linha; quando o preço estiver acima de uma determinada linha de grade, fechar uma ordem de venda acima dessa linha.

- Ajustar dinamicamente os limites superior e inferior da grade, a largura do intervalo e os preços das linhas da grade para se adaptar às mudanças do mercado.

Análise de Vantagens

- Pode obter lucros estáveis em mercados laterais e voláteis, sem ser afetado por movimentos unidirecionais.

- Suporta configuração manual e cálculo automático do intervalo da grade, com forte capacidade de adaptação.

- Permite otimizar os lucros ajustando o número de grades, a largura da grade e a quantidade de ordens.

- Possui controle de posição integrado para gerenciar riscos.

- Suporta ajuste dinâmico do intervalo da grade, conferindo forte adaptabilidade à estratégia.

Análise de Riscos

- Em movimentos de tendência acentuados, podem ocorrer perdas significativas.

- A definição inadequada do número de grades e da posição pode amplificar os riscos.

- O cálculo automático do intervalo da grade pode falhar em condições extremas de mercado.

Soluções para riscos:

- Otimizar os parâmetros da grade e controlar rigorosamente a posição total.

- Fechar a estratégia antes da chegada de grandes movimentos de mercado.

- Combinar com indicadores de tendência para avaliar as condições do mercado e, se necessário, fechar a estratégia.

Direções de Otimização

- Selecionar o número ideal de grades com base nas características do mercado e no tamanho do capital.

- Testar diferentes períodos de tempo para otimizar os parâmetros de cálculo automático da grade.

- Otimizar o método de cálculo da quantidade de ordens para obter lucros mais estáveis.

- Combinar com outros indicadores para identificar grandes movimentos e definir condições de fechamento da estratégia.

Resumo

Esta estratégia dinâmica de trading em grade adapta-se às mudanças do mercado ajustando dinamicamente os parâmetros do intervalo da grade, permitindo obter lucros em mercados laterais e voláteis. Ao mesmo tempo, o controle adequado da posição pode gerenciar os riscos. A otimização dos parâmetros da grade, combinada com indicadores de tendência, pode aumentar ainda mais a estabilidade da estratégia.

Source

Pine

/*backtest

start: 2023-12-23 00:00:00

end: 2024-01-22 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("sarasa srinivasa kumar", overlay=true, pyramiding=14, close_entries_rule="ANY", default_qty_type=strategy.cash, initial_capital=100.0, currency="USD", commission_type=strategy.commission.percent, commission_value=0.1)

i_autoBounds = input(group="Grid Bounds", title="Use Auto Bounds?", defval=true, type=input.bool) // calculate upper and lower bound of the grid automatically? This will theorhetically be less profitable, but will certainly require less attention

i_boundSrc = input(group="Grid Bounds", title="(Auto) Bound Source", defval="Hi & Low", options=["Hi & Low", "Average"]) // should bounds of the auto grid be calculated from recent High & Low, or from a Simple Moving AverageStrategy parameters

Related strategies

Comment

All comments (0)

No data

- 1