Estratégia de trading quantitativo combinando Fractal de Williams com indicador Zig Zag

Visão Geral

Esta é uma estratégia de negociação quantitativa que combina a teoria dos fractais de Bill Williams com o indicador ZZ. A estratégia determina a tendência do mercado calculando os fractais de Williams e, em seguida, utiliza o indicador ZZ para desenhar linhas de suporte e resistência, de modo a identificar possíveis pontos de rompimento e realizar negociações de acompanhamento de tendência.

Princípio da Estratégia

A estratégia primeiro calcula os fractais de Williams para determinar se o fractal atual é de alta ou de baixa. Se for um fractal de alta, considera-se que o mercado está em tendência de alta; se for de baixa, considera-se que está em tendência de baixa.

Em seguida, com base nos pontos fractais, traçam-se as linhas de suporte e resistência do indicador ZZ. Se o preço romper a linha de resistência correspondente ao fractal de alta, a estratégia assume uma posição comprada (long); se o preço romper a linha de suporte correspondente ao fractal de baixa, assume uma posição vendida (short).

Com essa combinação, é possível capturar as mudanças de tendência no momento em que ocorrem, realizando negociações de acompanhamento de tendência.

Análise das Vantagens da Estratégia

Esta estratégia combina dois métodos diferentes de análise técnica — fractais de Williams e indicador ZZ — para descobrir mais oportunidades de negociação.

Ela permite identificar rapidamente as mudanças de tendência do mercado e estabelece condições adequadas de stop loss e take profit, ajudando a acompanhar a direção da tendência principal. Além disso, o indicador ZZ pode filtrar alguns falsos rompimentos, evitando perdas desnecessárias.

Em suma, a estratégia considera tanto a identificação da tendência quanto a seleção de pontos de entrada específicos, equilibrando risco e retorno.

Análise de Risco da Estratégia

O maior risco desta estratégia reside no fato de que os fractais e o indicador ZZ podem gerar sinais de negociação falsos, resultando em perdas desnecessárias. Por exemplo, após romper uma linha de resistência, o preço pode cair rapidamente, sem conseguir continuar subindo.

Além disso, o cálculo dos fractais pode ser impreciso se o período de tempo for mal configurado. Se o período for muito curto, aumenta a probabilidade de falsos rompimentos.

Para reduzir esses riscos, é possível ajustar os parâmetros de cálculo dos fractais ou adicionar filtros adicionais para diminuir sinais falsos. Também é possível definir um stop loss mais amplo para controlar a perda por operação.

Direções de Otimização da Estratégia

Esta estratégia pode ser otimizada nos seguintes aspectos:

-

Adicionar filtros de momentum, como MACD ou Bandas de Bollinger, para evitar falsos rompimentos.

-

Otimizar os parâmetros dos fractais, ajustando o cálculo dos pontos máximos e mínimos e reduzindo o período de tempo para obter uma identificação de tendência mais precisa.

-

Incorporar algoritmos de aprendizado de máquina para avaliar a precisão da tendência, utilizando inteligência artificial para superar as limitações de configurações manuais.

-

Implementar um mecanismo de stop loss adaptativo, que ajuste a amplitude do stop loss de acordo com a volatilidade do mercado.

-

Utilizar algoritmos de aprendizado profundo para otimizar a configuração geral dos parâmetros.

Resumo

Esta estratégia combina habilmente a teoria dos fractais de Williams com o indicador ZZ, permitindo identificar e capturar rapidamente as mudanças de tendência do mercado. Ela mantém uma alta taxa de acerto e tem potencial para gerar retornos excedentes estáveis no longo prazo. No próximo passo, com a introdução de mais filtros e o uso de inteligência artificial, espera-se melhorar ainda mais a estabilidade e a rentabilidade da estratégia.

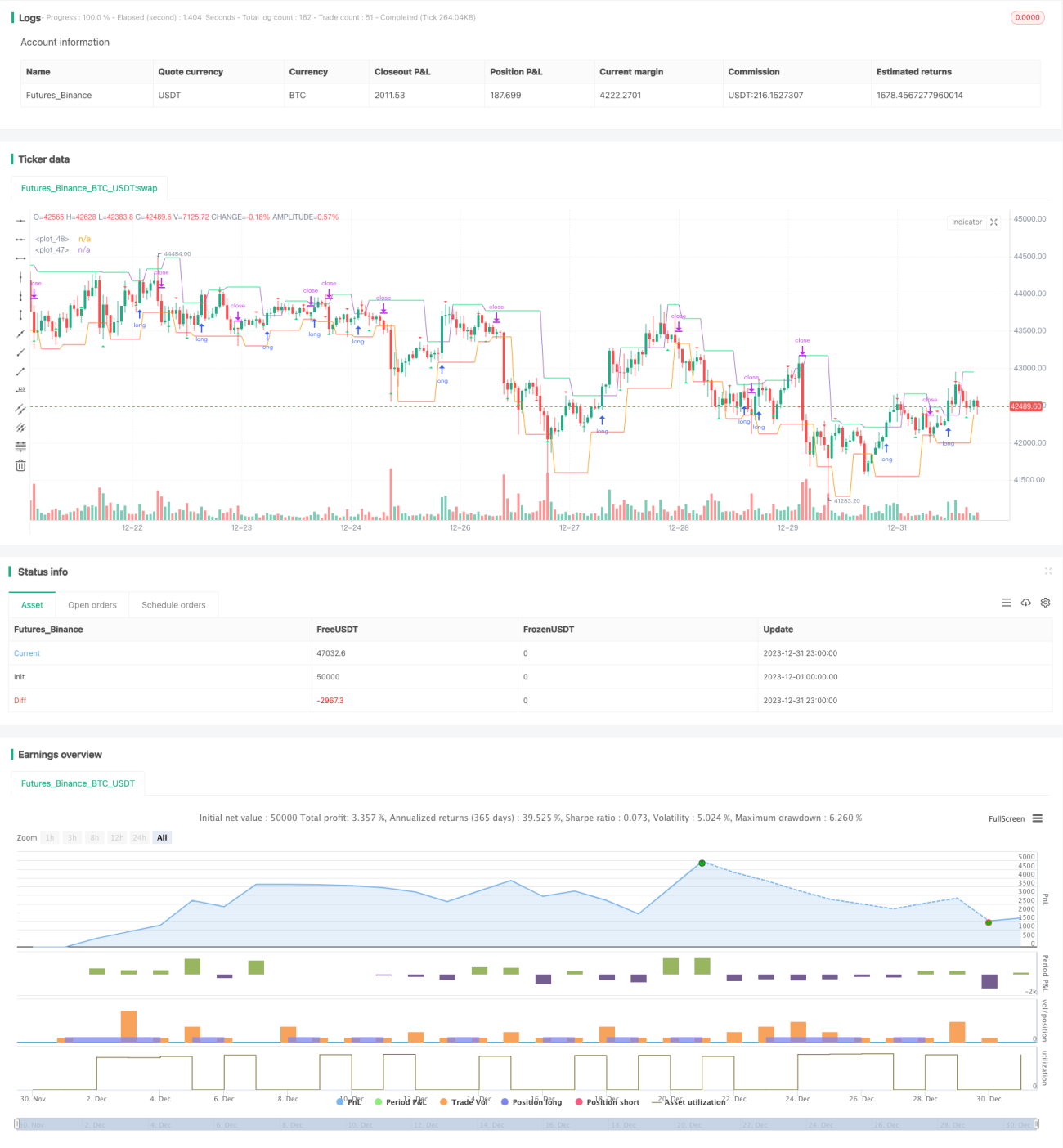

/*backtest

start: 2023-12-01 00:00:00

end: 2023-12-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy(title = "robotrading ZZ-8 fractals", shorttitle = "ZZ-8", overlay = true, default_qty_type = strategy.percent_of_equity, initial_capital = 100, default_qty_value = 100, commission_value = 0.1)

//Settings- 1