Estratégia de negociação de curto prazo com rompimento de momentum

Visão Geral

Esta estratégia acompanha os dados de negociação do SPY, combinando médias móveis, MACD, RSI e outros sinais de indicadores técnicos para identificar com precisão as tendências de curto prazo e tomar decisões de compra e venda, visando obter lucros em operações de curto prazo.

Princípio da Estratégia

A lógica central desta estratégia baseia-se nos seguintes indicadores técnicos para avaliar tendências de curto prazo e momentos de entrada:

- O cruzamento de alta (golden cross) e de baixa (death cross) das médias exponenciais de 5 e 13 períodos (EMA) são usados para identificar reversões de tendência de alta/baixa.

- O indicador MACD avalia se há momentum de alta.

- O indicador ADX verifica a existência de tendência.

- O indicador RSI mede a força da tendência.

Ao otimizar os parâmetros desses indicadores, são identificados os pontos críticos de reversão. Quando 5 das 6 condições são atendidas, um sinal branco é exibido indicando L ou S. Quando todas as seis condições são totalmente satisfeitas, um sinal dourado em formato de triângulo (△) é mostrado no fechamento da vela.

Condições para formação de sinal de compra:

EMA de 5 períodos maior que EMA de 13 períodos E linha MACD abaixo de 0,5 E ADX acima de 20 E inclinação do MACD maior que 0 E linha de sinal acima de -0,1 E RSI acima de 40

Condições para formação de sinal de venda:

EMA de 5 períodos menor que EMA de 13 períodos E linha MACD acima de -0,5 E ADX acima de 20 E linha de sinal abaixo de 0 E inclinação do MACD menor que 0 E RSI abaixo de 60

Análise de Vantagens

Esta estratégia apresenta as seguintes vantagens:

- Combina múltiplos sinais de indicadores, resultando em maior precisão nas decisões.

- Por meio da otimização de parâmetros, equilibra sensibilidade e precisão.

- Sinais claros e simples, com baixa barreira de execução.

- Adequada para negociação de curto prazo, alinhada ao perfil de risco da maioria dos investidores.

- Considera a necessidade de operações reais, evitando a alta volatilidade do período de fechamento.

Análise de Riscos

Esta estratégia também apresenta os seguintes riscos:

- Parâmetros mal ajustados podem levar a erros de sinalização. Requer testes e otimizações contínuas.

- Atua em um único ativo, não sendo possível diversificar riscos setoriais ou de alocação.

- Custos de transação e risco de slippage devido à alta frequência de negociações.

- A impossibilidade de abrir posições no período de fechamento pode resultar em perda de oportunidades.

Direções de Otimização

A estratégia pode ser melhorada nas seguintes dimensões:

- Testar modificações nos parâmetros para aumentar a precisão dos sinais.

- Adicionar indicadores de stop loss para controlar perdas individuais.

- Otimizar o horário de abertura de posições, filtrando períodos de alta volatilidade no fechamento.

- Incluir outros ativos como alvo da estratégia.

- Incorporar algoritmos de aprendizado de máquina para melhorar a adaptabilidade dos parâmetros.

Resumo

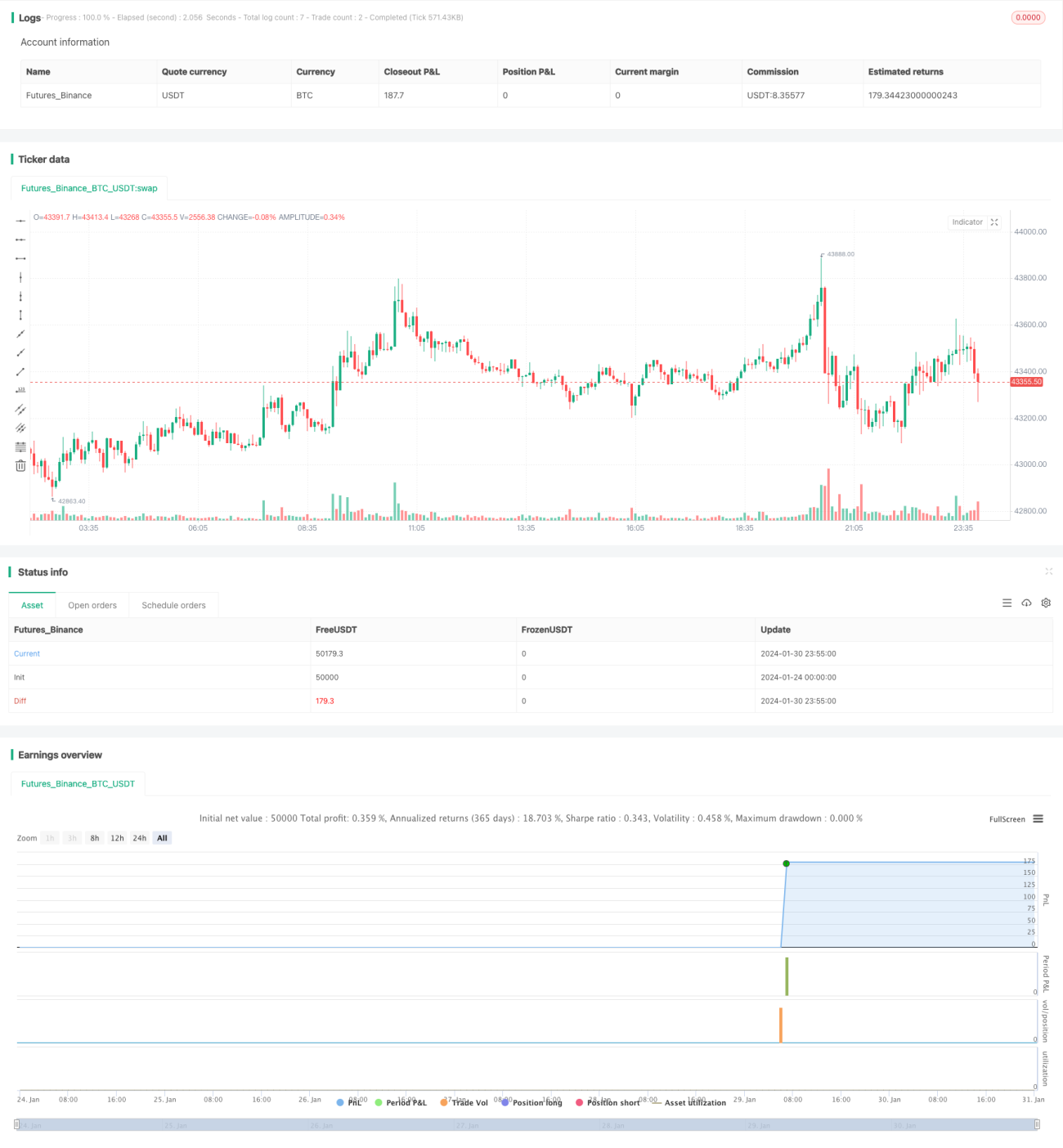

Esta estratégia acompanha os dados do SPY, combinando médias móveis, MACD, RSI e outros indicadores técnicos para avaliar tendências de curto prazo. Possui alta frequência de operações e baixo drawdown, sendo muito adequada para negociação de curto prazo. Pode ser otimizada em várias dimensões, oferecendo grande potencial de melhoria.

/*backtest

start: 2024-01-24 00:00:00

end: 2024-01-31 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=5

strategy(title="SPY 1 Minute Day Trader", overlay=true)

//This script has been created to take into account how the following variables impact trend for SPY 1 Minute- 1