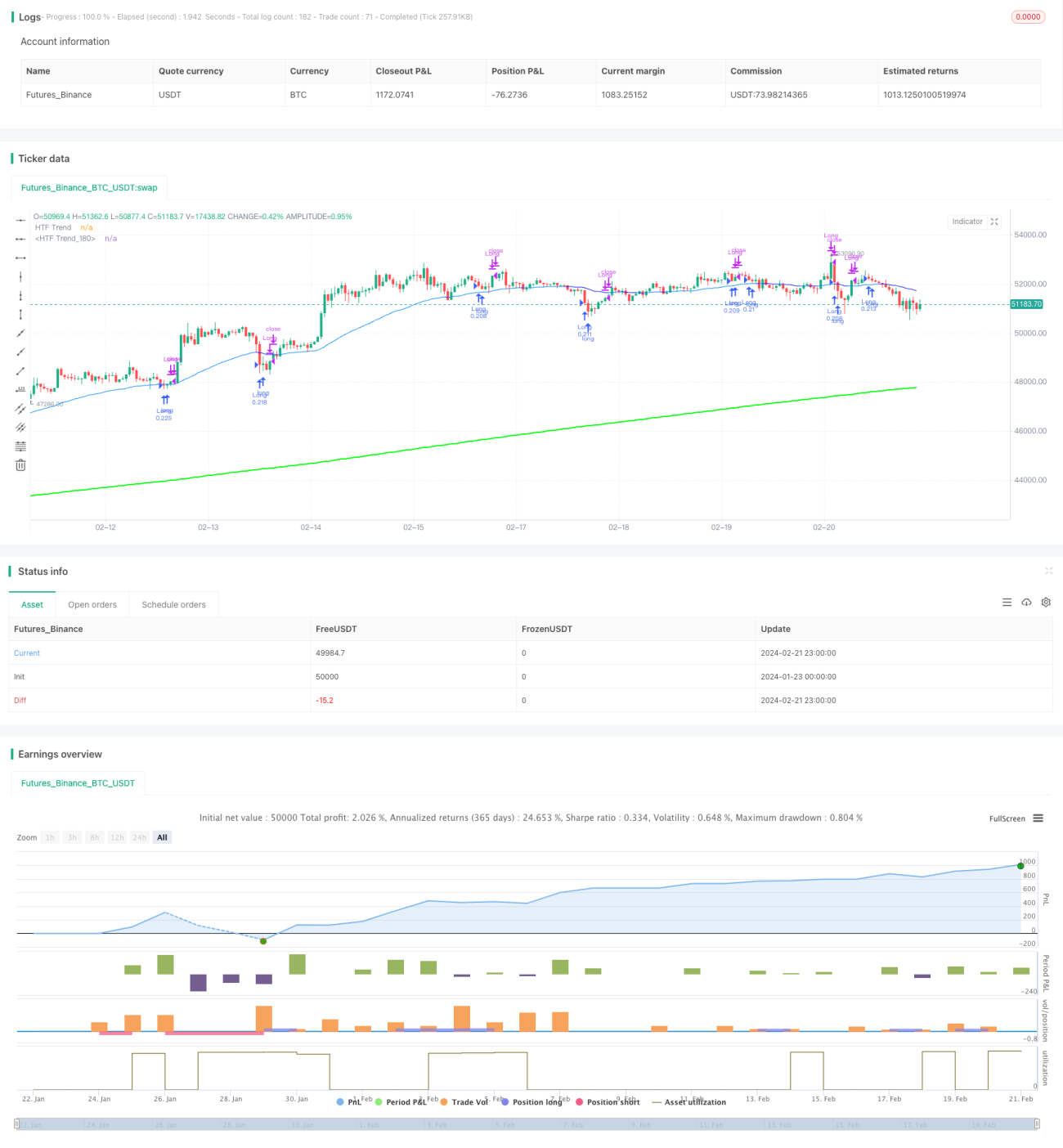

Estratégia de Seguimento de Tendência com Três Médias Móveis Dinâmicas

Visão Geral

A estratégia de seguimento de tendência com três médias móveis dinâmicas utiliza múltiplos períodos de tempo de médias móveis suavizadas dinamicamente para identificar a tendência do mercado, realizando a filtragem de consistência de tendência entre diferentes períodos de tempo, aumentando assim a fiabilidade dos sinais de negociação.

Princípio da Estratégia

Esta estratégia utiliza três médias móveis suavizadas dinamicamente com diferentes configurações de parâmetros. A primeira média móvel calcula a direção da tendência do preço no período atual; a segunda calcula a direção da tendência do preço num período de tempo superior; a terceira calcula a direção da tendência do preço num período de tempo ainda mais elevado. Quando a primeira média móvel cruza para cima a segunda, gera-se um sinal de compra, e se a terceira média móvel também estiver numa tendência ascendente, valida-se a fiabilidade do sinal de compra. Toda a estratégia, através da filtragem de tendência entre diferentes períodos de tempo, alcança a consistência de tendência em múltiplos quadros temporais, garantindo assim a fiabilidade dos sinais de negociação.

As médias móveis utilizam uma função de suavização dinâmica que calcula automaticamente e aplica os fatores de suavização adequados entre diferentes períodos de tempo, fazendo com que as médias móveis de períodos superiores apareçam como linhas de tendência suaves em gráficos de períodos inferiores, em vez de linhas irregulares em ziguezague. Esta suavização dinâmica permite que a estratégia julgue a direção geral da tendência em períodos de tempo superiores, enquanto executa operações em períodos de tempo inferiores, realizando um seguimento de tendência eficiente.

Vantagens da Estratégia

A maior vantagem desta estratégia reside no mecanismo de filtragem de tendência em múltiplos quadros temporais. Ao calcular a direção média da tendência dos preços em diferentes períodos de tempo e exigir consistência entre eles, é possível filtrar eficazmente a interferência das flutuações de curto prazo nos sinais de negociação, garantindo que cada sinal está inserido numa tendência de maior amplitude, aumentando significativamente a probabilidade de lucro.

Outra vantagem é a aplicação da função de suavização dinâmica. Isto permite que a estratégia identifique simultaneamente a tendência global em períodos de tempo superiores e os pontos de entrada específicos em períodos de tempo inferiores. A estratégia pode determinar a direção geral da tendência num período superior enquanto executa operações concretas num período inferior. Esta utilização de múltiplos quadros temporais ajuda a aproveitar as oportunidades de mercado ao mesmo tempo que controla o risco de negociação.

Riscos e Otimização

O principal risco desta estratégia é o baixo número de sinais de negociação. Condições rigorosas de filtragem de tendência reduzem a quantidade de oportunidades de negociação, o que pode não ser adequado para investidores que procuram negociação de alta frequência. É possível obter mais oportunidades de negociação reduzindo o rigor dos critérios de filtragem.

Além disso, os parâmetros precisam ser testados e otimizados cuidadosamente, especialmente o comprimento do período das médias móveis. Diferentes mercados requerem diferentes parâmetros de período para alcançar os melhores resultados. Podem ser realizados backtests para encontrar a combinação ideal de parâmetros.

Futuras direções de otimização podem incluir a adição de mais indicadores técnicos para filtragem, ou a introdução de algoritmos de aprendizagem automática para otimizar automaticamente os parâmetros. Estas serão formas eficazes de melhorar o desempenho da estratégia.

Resumo

No geral, esta estratégia é uma estratégia de seguimento de tendência muito prática. O mecanismo de filtragem de tendência em múltiplos quadros temporais fornece um bom suporte de direção para cada decisão de negociação, reduzindo eficazmente o risco de negociação. A adição da função de suavização dinâmica também permite que esta abordagem de múltiplos quadros temporais seja implementada de forma eficiente. Toda a estrutura da estratégia é razoável e funciona de forma eficiente, merecendo ser estudada e aplicada.

- 1