میڈین ریورژن اور موومنٹم حکمت عملی

خلاصہ

میانہ قدر واپسی (Mean Reversion) کی رفتار کی حکمت عملی ایک رجحان تجارتی حکمت عملی ہے جو مختصر مدت کی قیمت کی اوسط کو ٹریک کرتی ہے۔ یہ میانہ قدر واپسی کے اشارے اور رفتار کے اشارے کو ملا کر مارکیٹ کے درمیانی مدت کے رجحان کا اندازہ لگاتی ہے۔

حکمت عملی کا اصول

یہ حکمت عملی پہلے قیمت کی میانہ قدر واپسی کی لکیر اور معیاری انحراف کا حساب لگاتی ہے۔ پھر Upper Threshold اور Lower Threshold پیرامیٹرز میں طے شدہ حدوں کو ملا کر یہ جانچتی ہے کہ آیا قیمت میانہ قدر واپسی کی لکیر سے ایک معیاری انحراف کی حد سے باہر ہے یا نہیں۔ اگر باہر ہے تو تجارتی سگنل پیدا ہوتا ہے۔

لمبی پوزیشن (Long) کے سگنل کے لیے، قیمت میانہ قدر واپسی کی لکیر سے ایک معیاری انحراف نیچے ہونی چاہیے، بند (Close) قیمت LENGTH مدت کی SMA اوسط سے نیچے اور TREND SMA اوسط سے اوپر ہونی چاہیے۔ ان تین شرائط کے پورا ہونے پر لمبی پوزیشن کھولی جاتی ہے۔ پوزیشن بند کرنے کی شرط یہ ہے کہ قیمت LENGTH مدت کی SMA اوسط کو اوپر سے عبور کرے۔

چھوٹی پوزیشن (Short) کے سگنل کے لیے، قیمت میانہ قدر واپسی کی لکیر سے ایک معیاری انحراف اوپر ہونی چاہیے، بند قیمت LENGTH مدت کی SMA اوسط سے اوپر اور TREND SMA اوسط سے نیچے ہونی چاہیے۔ ان تین شرائط کے پورا ہونے پر چھوٹی پوزیشن کھولی جاتی ہے۔ پوزیشن بند کرنے کی شرط یہ ہے کہ قیمت LENGTH مدت کی SMA اوسط کو نیچے سے عبور کرے۔

یہ حکمت عملی Percent Profit Target اور Percent Stop Loss کو بھی ملاتی ہے تاکہ منافع اور نقصان کا انتظام کیا جا سکے۔

باہر نکلنے (Exit) کا طریقہ مووینگ ایوریج بریک آؤٹ یا لکیری رجعت بریک آؤٹ میں سے انتخاب کیا جا سکتا ہے۔

لمبی اور چھوٹی دونوں طرف تجارت، رجحان کی فلٹریشن، اور منافع/نقصان کے انتظام کے امتزاج سے مارکیٹ کے درمیانی مدت کے رجحان کا تعین اور اس کی پیروی ممکن ہوتی ہے۔

حکمت عملی کے فوائد

-

میانہ قدر واپسی کا اشارہ مؤثر طریقے سے یہ جانچ سکتا ہے کہ قیمت اپنی بنیادی قدر سے ہٹ گئی ہے یا نہیں۔

-

SMA رفتار کا اشارہ مختصر مدت کے مارکیٹ کے شور کو فلٹر کر سکتا ہے۔

-

لمبی اور چھوٹی دونوں طرف تجارت رجحان کے مواقع کو ہر طرف سے پکڑ سکتی ہے۔

-

منافع اور نقصان کا انتظامی طریقہ کار خطرے کو مؤثر طریقے سے کنٹرول کر سکتا ہے۔

-

باہر نکلنے کے قابل انتخاب طریقے مارکیٹ کے حالات کے مطابق لچک فراہم کرتے ہیں۔

-

مکمل رجحان تجارتی حکمت عملی درمیانی مدت کے رجحان کو بہتر طور پر سمجھنے میں مدد دیتی ہے۔

حکمت عملی کے خطرات

-

میانہ قدر واپسی کا اشارہ پیرامیٹر کی ترتیب کے لیے حساس ہے، حدوں (Thresholds) کی غلط ترتیب جھوٹے سگنلز کا سبب بن سکتی ہے۔

-

بڑے اتار چڑھاؤ والی مارکیٹ میں نقصان روکنے (Stop Loss) کی حد بار بار لگ سکتی ہے۔

-

اتار چڑھاؤ والے رجحان میں تجارت کی تعدد بہت زیادہ ہو سکتی ہے، جس سے تجارتی اخراجات اور سلپیج (Slippage) کا خطرہ بڑھ جاتا ہے۔

-

جب تجارتی شے کی روانی (Liquidity) کم ہو تو سلپیج کا کنٹرول بہتر نہیں ہو سکتا۔

-

لمبی اور چھوٹی دونوں طرف تجارت کا خطرہ زیادہ ہوتا ہے، اس لیے سرمائے کے انتظام میں احتیاط ضروری ہے۔

ان خطرات کو پیرامیٹر کی اصلاح، نقصان روکنے کے طریقہ کار میں تبدیلی، اور سرمائے کے انتظام کے ذریعے کنٹرول کیا جا سکتا ہے۔

حکمت عملی کی اصلاح کے ممکنہ شعبے

-

میانہ قدر واپسی اور رفتار کے اشارے کے پیرامیٹرز کو مختلف اشیاء کی خصوصیات کے مطابق بہتر بنانا۔

-

رجحان کا تعین کرنے والے مزید اشارے شامل کرنا تاکہ رجحان کی شناخت کی صلاحیت بہتر ہو۔

-

نقصان روکنے کی حکمت عملی کو بہتر بنانا تاکہ مارکیٹ کے بڑے اتار چڑھاؤ کو برداشت کیا جا سکے۔

-

پوزیشن کے حجم کے انتظام کا ماڈیول شامل کرنا تاکہ مارکیٹ کے حالات کے مطابق پوزیشن کا سائز تبدیل کیا جا سکے۔

-

مزید خطرے کے انتظام کے ماڈیول شامل کرنا، جیسے زیادہ سے زیادہ کمی (Maximum Drawdown) کا کنٹرول، نیٹ ویلیو کرو (Net Worth Curve) کا کنٹرول وغیرہ۔

-

مشین لرننگ کے طریقوں کو شامل کرنے پر غور کرنا تاکہ حکمت عملی کے پیرامیٹرز خود بخود بہتر ہو سکیں۔

خلاصہ

مذکورہ بالا تمام باتوں سے یہ نتیجہ اخذ کیا جا سکتا ہے کہ میانہ قدر واپسی کی رفتار کی حکمت عملی سادہ اور مؤثر اشارے کے ڈیزائن کے ذریعے درمیانی مدت کی قدر واپسی کے رجحان کو پکڑتی ہے۔ اس حکمت عملی میں اعلیٰ موافقت اور عام اطلاق کی صلاحیت ہے، لیکن اس میں کچھ خطرات بھی موجود ہیں۔ مسلسل اصلاح اور دیگر حکمت عملیوں کے ساتھ امتزاج سے بہتر کارکردگی حاصل کی جا سکتی ہے۔ یہ حکمت عملی مجموعی طور پر مکمل ہے اور رجحان کی تجارت کے لیے ایک قابل غور طریقہ ہے۔

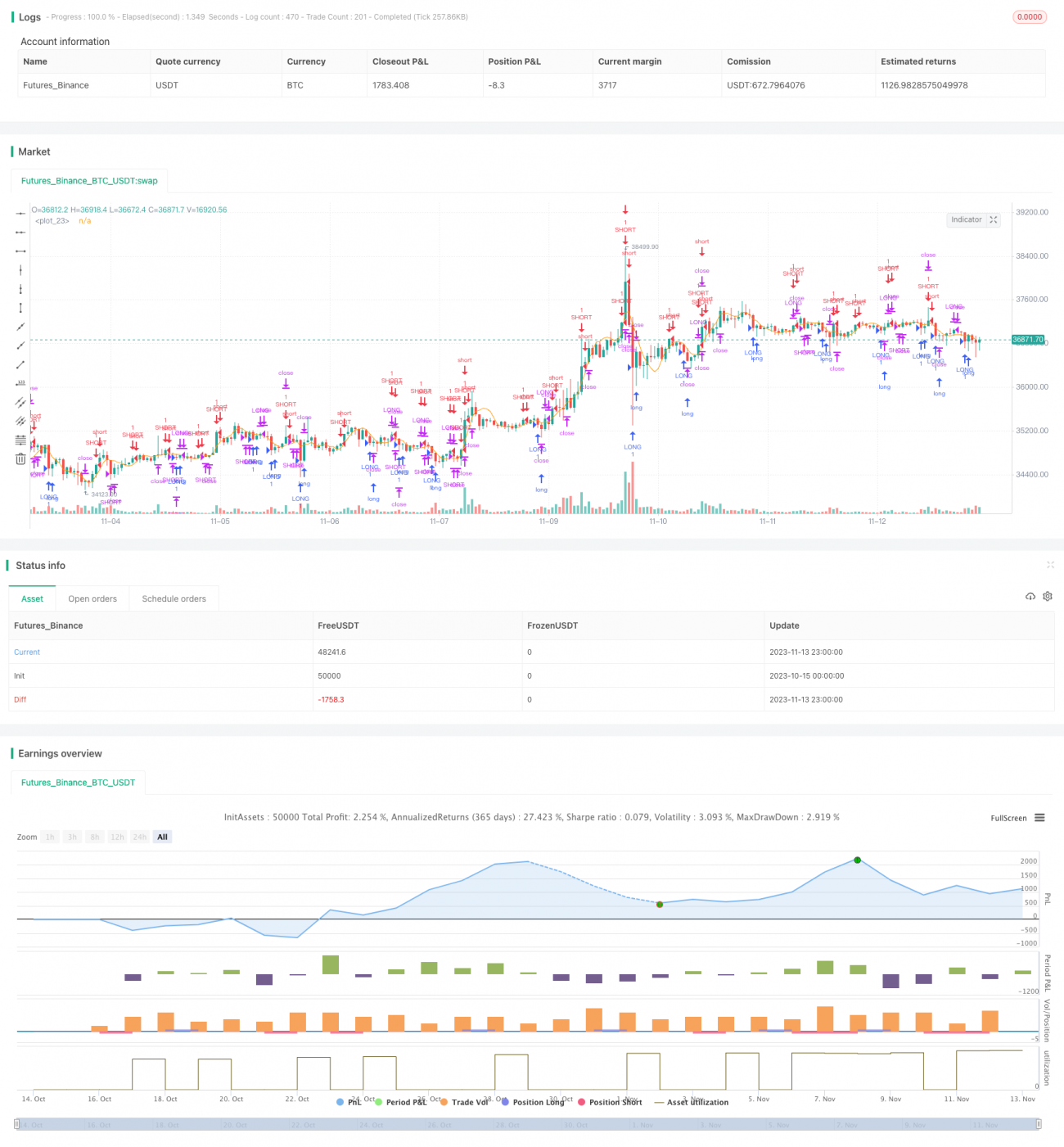

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1