Chiến lược giao dịch tự động toàn diện với đường trung bình động cầu vồng

Tổng quan

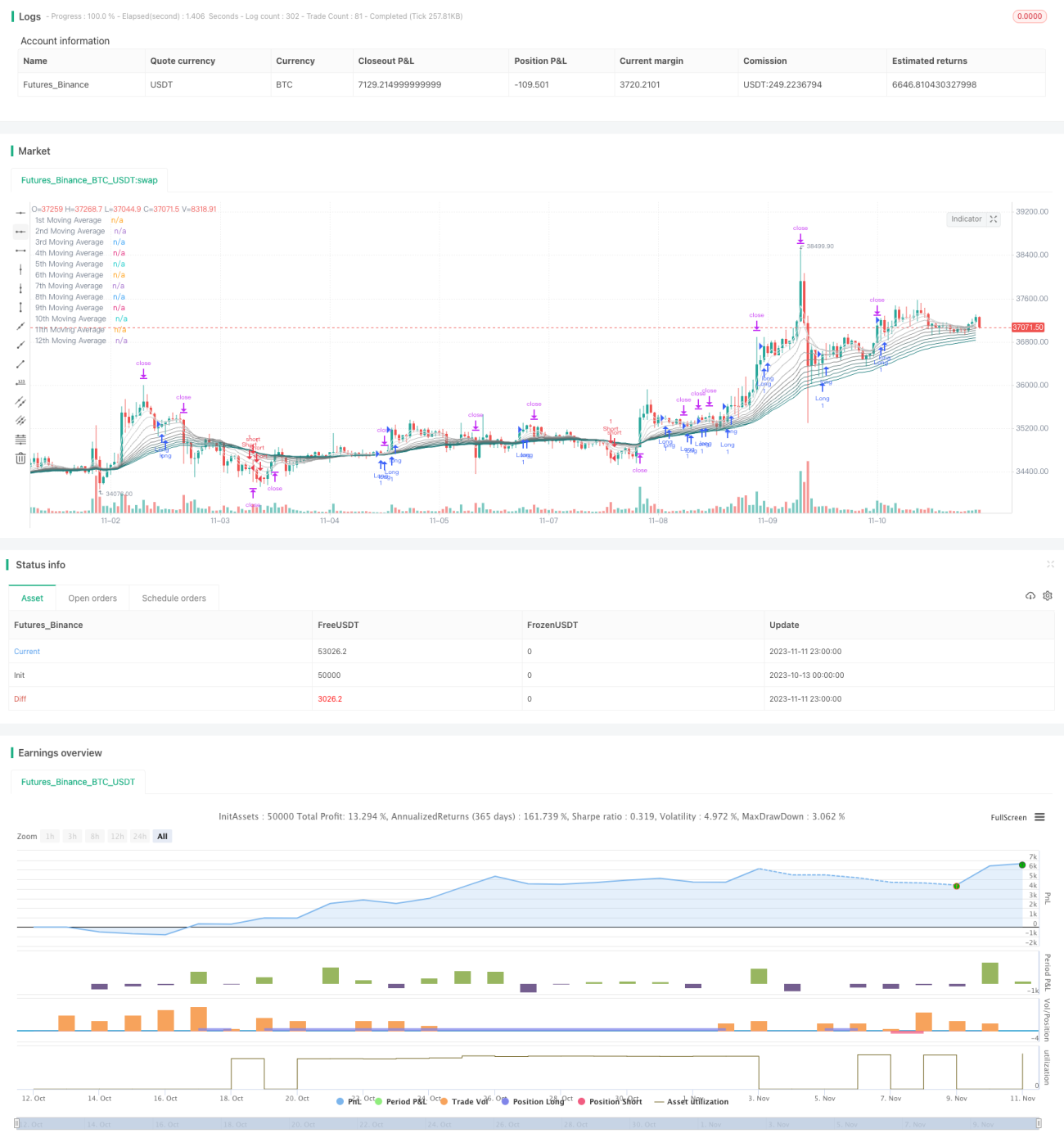

Chiến lược Cầu vồng MA Giao dịch Tự động Toàn diện là một chiến lược kết hợp nhiều đường trung bình động với nhiều khung thời gian điển hình. Nó sử dụng 12 đường trung bình động với các chu kỳ khác nhau, thông qua thứ tự sắp xếp của các đường trung bình động và mối quan hệ với giá để xác định hướng đi của thị trường, cũng như xác định các điều kiện vào lệnh, cắt lỗ và chốt lời, thực hiện giao dịch tự động. Chiến lược này có thể tự động nhận diện xu hướng và có cơ chế cắt lỗ hoàn chỉnh để kiểm soát rủi ro.

Nguyên lý

Chiến lược sử dụng 12 đường trung bình động, bao gồm các chu kỳ 3, 5, 8 cho đến 55. Loại đường trung bình động có thể chọn EMA, SMA, RMA, v.v. Trước tiên, chiến lược đánh giá mối quan hệ sắp xếp giữa các đường trung bình động chu kỳ ngắn và chu kỳ dài (Đường 1-4 chu kỳ và Đường 5-8 chu kỳ). Nếu các đường ngắn nằm trên, được xác định là môi trường xu hướng tăng; nếu các đường ngắn nằm dưới, được xác định là môi trường xu hướng giảm.

Trong xu hướng tăng, nếu giá phá vỡ đường trung bình động tương ứng với đáy trước đó, được xác định là tín hiệu vào lệnh, mua lên; cắt lỗ đặt tại đường trung bình động tương ứng với đáy trước đó, chốt lời cách cắt lỗ 1,6 lần. Trong xu hướng giảm, nếu giá phá vỡ đường trung bình động tương ứng với đỉnh trước đó, được xác định là tín hiệu vào lệnh, bán khống; cắt lỗ đặt tại đường trung bình động tương ứng với đỉnh trước đó, chốt lời cách cắt lỗ 1,6 lần.

Chiến lược này còn có chức năng phát hiện đảo chiều xu hướng. Trong thời gian nắm giữ vị thế, nếu các đường trung bình động chu kỳ ngắn thay đổi thứ tự sắp xếp, đồng thời giá vượt qua đỉnh hoặc đáy gần nhất, thì được xác định là có khả năng xảy ra đảo chiều xu hướng. Lúc này, thoát khỏi vị thế hiện tại, chuyển sang vị thế ngược lại, lấy đỉnh hoặc đáy mới làm vị trí cắt lỗ và chốt lời.

Ưu điểm

-

Chiến lược này kết hợp phân tích đa khung thời gian, có thể đánh giá tốt hướng xu hướng.

-

Chiến lược bổ sung đánh giá thứ tự thuận nghịch của các đường trung bình động, tránh bị đánh lừa trong thị trường đi ngang.

-

Chiến lược có cơ chế cắt lỗ hoàn chỉnh, có thể kiểm soát hiệu quả rủi ro cho từng giao dịch.

-

Chiến lược có chức năng phát hiện đảo chiều xu hướng, có thể kịp thời nắm bắt cơ hội đảo chiều, giảm rủi ro hệ thống.

-

Các tham số của chiến lược linh hoạt, chu kỳ và loại đường trung bình động đều có thể tùy chỉnh.

-

Chiến lược sử dụng phương pháp cắt lỗ theo dõi (trailing stop), có thể khóa lợi nhuận tối đa.

Rủi ro

-

Chiến lược kết hợp nhiều đường trung bình động, việc thiết lập tham số ảnh hưởng đến hiệu suất, cần tối ưu hóa và kiểm tra.

-

Trong thị trường đi ngang, các đường trung bình động sẽ phát ra tín hiệu sai, nên điều chỉnh tham số phù hợp hoặc tạm thời không giao dịch.

-

Tồn tại độ trễ nhất định, có thể bỏ lỡ cơ hội gần các điểm đảo chiều xu hướng.

-

Cần chú ý đến các chỉ báo kỹ thuật khác, tránh mở lệnh bán khống gần các vùng hỗ trợ quan trọng.

-

Rủi ro hệ thống cần được quan tâm, cơ chế phát hiện đảo chiều không thể loại bỏ hoàn toàn rủi ro này.

-

Cần thêm cơ chế kiểm soát sụt giảm, có thể xem xét thêm quản lý vị thế động.

Hướng tối ưu hóa

-

Kiểm tra các loại đường trung bình động và thiết lập tham số khác nhau để tìm ra tổ hợp tốt nhất.

-

Tối ưu hóa cơ chế phát hiện đảo chiều, thiết lập điều kiện kích hoạt đảo chiều chính xác hơn.

-

Thêm cơ chế quản lý vị thế động, giảm vị thế khi sụt giảm quá lớn.

-

Xem xét thêm thuật toán học máy, sử dụng dữ liệu lớn để huấn luyện xác định các điểm quan trọng.

-

Kết hợp với các tín hiệu chỉ báo khác để đánh giá tổng hợp, nâng cao độ chính xác của quyết định.

-

Xây dựng danh mục giao dịch đa sản phẩm, sử dụng mối tương quan không liên quan để phân tán rủi ro.

Tổng kết

Nhìn chung, Chiến lược Cầu vồng MA Giao dịch Tự động Toàn diện là một chiến lược theo xu hướng vững chắc, có khả năng nhận diện xu hướng và kiểm soát rủi ro mạnh mẽ. Thông qua việc tối ưu hóa tham số, thêm quản lý vị thế động và các cải tiến khác, nó có thể trở thành một chiến lược giao dịch định lượng rất thực tế. Chiến lược này có tư duy rõ ràng, dễ hiểu, đồng thời có tính linh hoạt nhất định, đáng để nghiên cứu sử dụng và liên tục tối ưu hóa.

- 1