Chiến lược động lượng hồi quy trung bình

Tổng quan

Chiến lược động lượng hồi quy trung bình là một chiến lược giao dịch xu hướng theo dõi mức giá trung bình ngắn hạn. Nó kết hợp chỉ báo hồi quy trung bình và chỉ báo động lượng để đánh giá xu hướng trung hạn của thị trường.

Nguyên lý chiến lược

Chiến lược này trước tiên tính toán đường hồi quy trung bình và độ lệch chuẩn của giá. Sau đó kết hợp với các ngưỡng được thiết lập bởi tham số Upper Threshold và Lower Threshold để xác định xem giá có vượt quá phạm vi một độ lệch chuẩn so với đường hồi quy trung bình hay không. Nếu vượt quá, tín hiệu giao dịch sẽ được tạo ra.

Đối với tín hiệu mua (long), cần có giá thấp hơn đường hồi quy trung bình một độ lệch chuẩn, giá đóng cửa (Close) thấp hơn đường trung bình động SMA chu kỳ LENGTH, và cao hơn đường SMA xu hướng (TREND SMA). Khi thỏa mãn ba điều kiện này, lệnh mua sẽ được mở. Điều kiện đóng lệnh là giá cắt lên trên đường SMA chu kỳ LENGTH.

Đối với tín hiệu bán (short), cần có giá cao hơn đường hồi quy trung bình một độ lệch chuẩn, giá đóng cửa (Close) cao hơn đường SMA chu kỳ LENGTH, và thấp hơn đường SMA xu hướng (TREND SMA). Khi thỏa mãn ba điều kiện này, lệnh bán sẽ được mở. Điều kiện đóng lệnh là giá cắt xuống dưới đường SMA chu kỳ LENGTH.

Chiến lược này cũng kết hợp Percent Profit Target và Percent Stop Loss để quản lý chốt lời và cắt lỗ.

Phương thức thoát lệnh (Exit) có thể chọn đột phá đường trung bình động hoặc đột phá hồi quy tuyến tính.

Thông qua sự kết hợp giao dịch hai chiều mua/bán, lọc xu hướng, chốt lời/cắt lỗ, chiến lược này đạt được khả năng đánh giá và theo dõi xu hướng trung hạn của thị trường.

Lợi thế của chiến lược

-

Chỉ báo hồi quy trung bình có thể đánh giá hiệu quả liệu giá có lệch khỏi giá trị trung tâm hay không

-

Chỉ báo động lượng SMA có thể lọc nhiễu thị trường ngắn hạn

-

Giao dịch hai chiều mua/bán, có thể nắm bắt toàn diện cơ hội xu hướng

-

Cơ chế chốt lời/cắt lỗ có thể kiểm soát rủi ro hiệu quả

-

Phương thức thoát lệnh có thể lựa chọn, linh hoạt thích ứng với điều kiện thị trường

-

Chiến lược giao dịch xu hướng hoàn chỉnh, nắm bắt tốt xu hướng trung hạn

Rủi ro của chiến lược

-

Chỉ báo hồi quy trung bình nhạy cảm với việc thiết lập tham số, ngưỡng không phù hợp có thể dẫn đến tín hiệu giả

-

Trong thị trường biến động mạnh, có thể xảy ra cắt lỗ quá thường xuyên

-

Khi thị trường đi ngang, tần suất giao dịch có thể quá cao, làm tăng chi phí giao dịch và rủi ro trượt giá

-

Khi tính thanh khoản của sản phẩm giao dịch thấp, việc kiểm soát trượt giá có thể không lý tưởng

-

Giao dịch hai chiều mua/bán có rủi ro lớn hơn, cần quản lý vốn thận trọng

Có thể kiểm soát các rủi ro này thông qua tối ưu hóa tham số, điều chỉnh phương thức cắt lỗ, quản lý vốn, v.v.

Hướng tối ưu hóa chiến lược

-

Tối ưu hóa thiết lập tham số của chỉ báo hồi quy trung bình và động lượng, làm cho chúng phù hợp hơn với đặc điểm của từng sản phẩm khác nhau

-

Thêm chỉ báo đánh giá xu hướng, nâng cao khả năng nhận diện xu hướng

-

Tối ưu hóa chiến lược cắt lỗ, làm cho nó thích ứng tốt hơn với biến động lớn của thị trường

-

Thêm mô-đun quản lý vị thế, điều chỉnh quy mô vị thế theo điều kiện thị trường

-

Thêm nhiều mô-đun kiểm soát rủi ro, như kiểm soát drawdown tối đa, kiểm soát đường cong NAV, v.v.

-

Xem xét kết hợp phương pháp học máy để tự động tối ưu hóa tham số chiến lược

Tổng kết

Tóm lại, chiến lược động lượng hồi quy trung bình thông qua thiết kế chỉ báo đơn giản và hiệu quả, đã đạt được khả năng nắm bắt xu hướng hồi quy về giá trị trung hạn. Chiến lược có tính thích ứng và phổ quát cao, nhưng cũng tồn tại một số rủi ro nhất định. Thông qua tối ưu hóa liên tục và kết hợp với các chiến lược khác, có thể đạt được hiệu suất tốt hơn. Nhìn chung, chiến lược này khá hoàn chỉnh và là một phương pháp giao dịch xu hướng đáng xem xét.

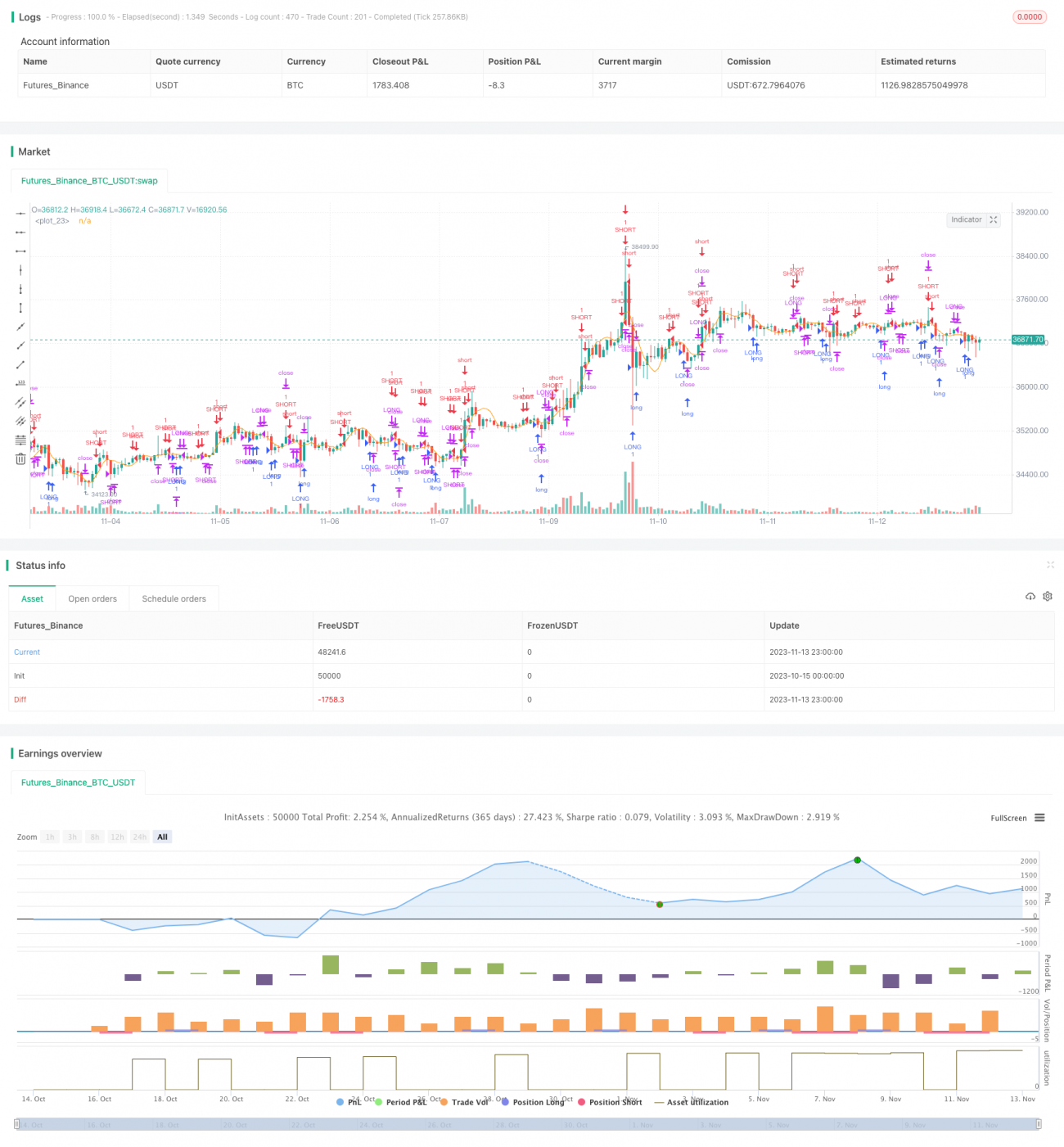

/*backtest

start: 2023-10-15 00:00:00

end: 2023-11-14 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © GlobalMarketSignals

//@version=4- 1