Chiến lược giao dịch đảo chiều TD động lượng

Tổng quan

Chiến lược giao dịch đảo chiều Momentum TD là một chiến lược giao dịch định lượng sử dụng chỉ báo TD Sequential để xác định tín hiệu đảo chiều giá. Chiến lược này dựa trên phân tích động lượng giá, thiết lập vị thế mua hoặc bán sau khi xác nhận tín hiệu đảo chiều giá.

Nguyên lý chiến lược

Chiến lược này sử dụng chỉ báo TD Sequential để phân tích biến động giá và xác định mô hình đảo chiều giá gồm 9 nến liên tiếp. Cụ thể, khi phát hiện 9 nến liên tiếp tăng giá sau đó xuất hiện nến giảm, chiến lược xác định cơ hội bán khống; ngược lại, khi phát hiện 9 nến liên tiếp giảm giá sau đó xuất hiện nến tăng, chiến lược xác định cơ hội mua lên.

Nhờ lợi thế của chỉ báo TD Sequential, có thể bắt được tín hiệu đảo chiều giá sớm. Kết hợp với cơ chế mua đuổi bán đuổi với số lượng nhất định trong chiến lược này, có thể thiết lập vị thế mua hoặc bán kịp thời sau khi xác nhận tín hiệu đảo chiều, từ đó có được cơ hội vào lệnh tốt hơn ở giai đoạn đầu của quá trình đảo chiều giá.

Phân tích ưu điểm

- Sử dụng chỉ báo TD Sequential có thể xác định sớm cơ hội đảo chiều giá

- Thiết lập cơ chế mua đuổi bán đuổi, giúp xác nhận đảo chiều giá kịp thời hơn

- Xây dựng vị thế trong giai đoạn hình thành đảo chiều, đạt được điểm vào lệnh tối ưu

Phân tích rủi ro

- Chỉ báo TD Sequential có thể xuất hiện tín hiệu phá vỡ giả, cần kết hợp các yếu tố khác để xác nhận

- Cần kiểm soát quy mô vị thế và thời gian nắm giữ hợp lý để giảm thiểu rủi ro

Hướng tối ưu hóa

- Kết hợp các chỉ báo khác để xác định tín hiệu đảo chiều, tránh rủi ro phá vỡ giả

- Thiết lập cơ chế cắt lỗ để kiểm soát tổn thất từng giao dịch

- Tối ưu hóa quy mô vị thế và thời gian nắm giữ, cân bằng giữa lợi nhuận và kiểm soát rủi ro

Tổng kết

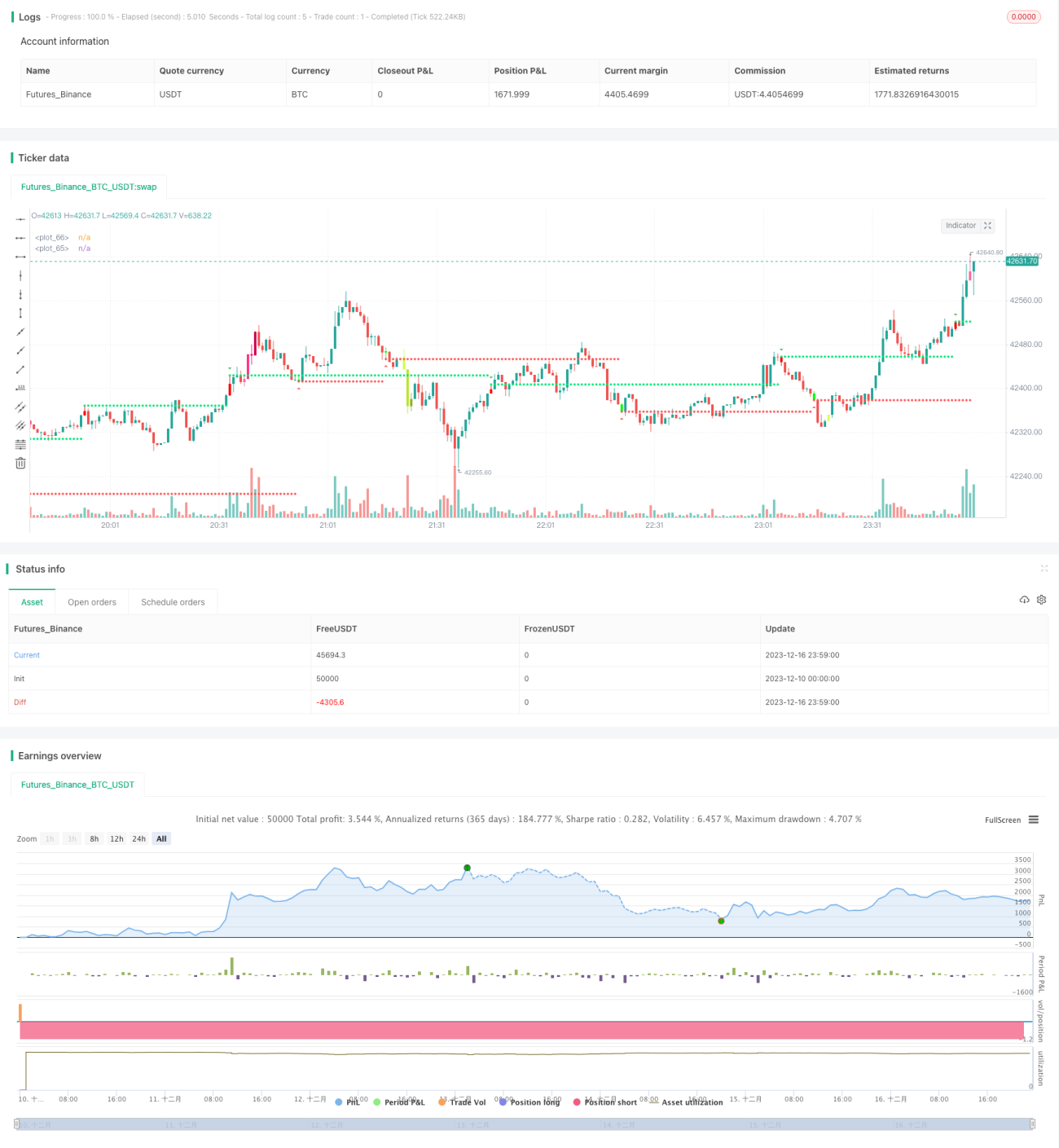

Chiến lược giao dịch đảo chiều Momentum TD xác định sớm sự đảo chiều giá thông qua chỉ báo TD Sequential và thiết lập vị thế nhanh chóng sau khi xác nhận đảo chiều, là một chiến lược rất phù hợp cho các nhà giao dịch động lượng. Chiến lược này có lợi thế trong việc nhận diện cơ hội đảo chiều, nhưng cần chú ý kiểm soát rủi ro, tránh tổn thất lớn do tín hiệu phá vỡ giả. Thông qua tối ưu hóa thêm, đây là một chiến lược giao dịch có tỷ lệ lợi nhuận/rủi ro cân bằng.

/*backtest

start: 2023-12-10 00:00:00

end: 2023-12-17 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

//This strategy is based on TD sequential study from glaz.

//I made some improvement and modification to comply with pine script version 4.

//Basically, it is a strategy based on proce action, supports and resistance.- 1