Chiến lược hồi lại sau giao cắt vàng EMA

Tổng quan

Chiến lược giao dịch hồi giá với đường EMA vàng là một chiến lược giao dịch định lượng dựa trên chỉ báo EMA. Chiến lược này sử dụng ba đường EMA với các chu kỳ khác nhau để tạo tín hiệu giao dịch, kết hợp với cơ chế hồi giá để thiết lập stop loss và take profit, thực hiện giao dịch tự động.

Nguyên lý chiến lược

Chiến lược này sử dụng ba đường EMA:

- EMA1: Dùng để xác định mức hỗ trợ/kháng cự khi giá hồi, chu kỳ ngắn, mặc định 33 kỳ.

- EMA2: Dùng để lọc bớt các tín hiệu đảo chiều, chu kỳ gấp 5 lần EMA1, mặc định 165 kỳ.

- EMA3: Dùng để xác định xu hướng tổng thể, chu kỳ gấp 11 lần EMA1, mặc định 365 kỳ.

Tín hiệu giao dịch được tạo ra theo logic sau:

Tín hiệu Long: Giá vượt lên trên EMA1, sau đó xảy ra hồi giá, hình thành đáy cao hơn phía trên EMA1, biên độ hồi không chạm EMA2. Khi điều kiện được thỏa mãn, vào lệnh Long khi giá lại vượt lên trên EMA1.

Tín hiệu Short: Giá vượt xuống dưới EMA1, sau đó xảy ra hồi giá, hình thành đỉnh thấp hơn phía dưới EMA1, biên độ hồi không chạm EMA2. Khi điều kiện được thỏa mãn, vào lệnh Short khi giá lại vượt xuống dưới EMA1.

Cách thức stop loss: Giá thấp nhất/cao nhất trong lần hồi. Take profit được đặt gấp 2 lần stop loss.

Ưu điểm của chiến lược

Chiến lược này có các ưu điểm sau:

- Sử dụng chỉ báo EMA để tạo tín hiệu giao dịch, độ tin cậy cao.

- Kết hợp cơ chế hồi giá, có thể tránh bị kẹt lệnh hiệu quả.

- Điểm dừng lỗ đặt tại vùng giá cao/thấp trước đó, kiểm soát rủi ro tốt.

- Đặt điểm chốt lời theo tỷ lệ stop loss/take profit, đáp ứng yêu cầu tỷ lệ lời/lỗ.

- Có thể điều chỉnh tham số EMA theo thị trường, thích ứng với các chu kỳ khác nhau.

Rủi ro của chiến lược

Chiến lược này cũng có một số rủi ro:

- Chỉ báo EMA có độ trễ, có thể bỏ lỡ điểm đảo chiều xu hướng.

- Phạm vi hồi giá quá lớn, vượt quá EMA2 có thể tạo tín hiệu giả.

- Trong thị trường xu hướng mạnh, stop loss có thể bị phá vỡ.

- Cài đặt tham số không phù hợp có thể dẫn đến giao dịch quá thường xuyên hoặc bỏ lỡ cơ hội.

Có thể tối ưu hóa tham số bằng cách điều chỉnh chu kỳ EMA, giới hạn phạm vi hồi giá, v.v. Cũng có thể kết hợp các chỉ báo khác để lọc tín hiệu.

Hướng tối ưu hóa chiến lược

Chiến lược này còn có thể được tối ưu hóa từ các khía cạnh sau:

- Thêm chỉ báo xu hướng để tránh giao dịch ngược xu hướng. Ví dụ: kết hợp MACD.

- Thêm chỉ báo khối lượng giao dịch để tránh phá vỡ giả. Ví dụ: kết hợp OBV.

- Tối ưu hóa tham số chu kỳ EMA, hoặc sử dụng EMA thích ứng.

- Kết hợp các phương pháp học máy như mô hình túi từ để tối ưu hóa tham số động.

- Thêm dự đoán mô hình, thiết lập stop loss/take profit thích ứng.

Tổng kết

Chiến lược giao dịch hồi giá với đường EMA vàng đã xây dựng hệ thống giao dịch ba đường EMA, kết hợp đặc tính hồi giá để thiết lập take profit và stop loss, thực hiện giao dịch tự động. Chiến lược này kiểm soát rủi ro giao dịch hiệu quả và có thể được tối ưu hóa bằng cách điều chỉnh tham số theo thị trường. Nhìn chung, logic của chiến lược hợp lý và có thể áp dụng thực tế. Trong tương lai, có thể tối ưu hóa thêm từ các khía cạnh như xác định xu hướng, tối ưu hóa tham số, kiểm soát rủi ro, v.v.

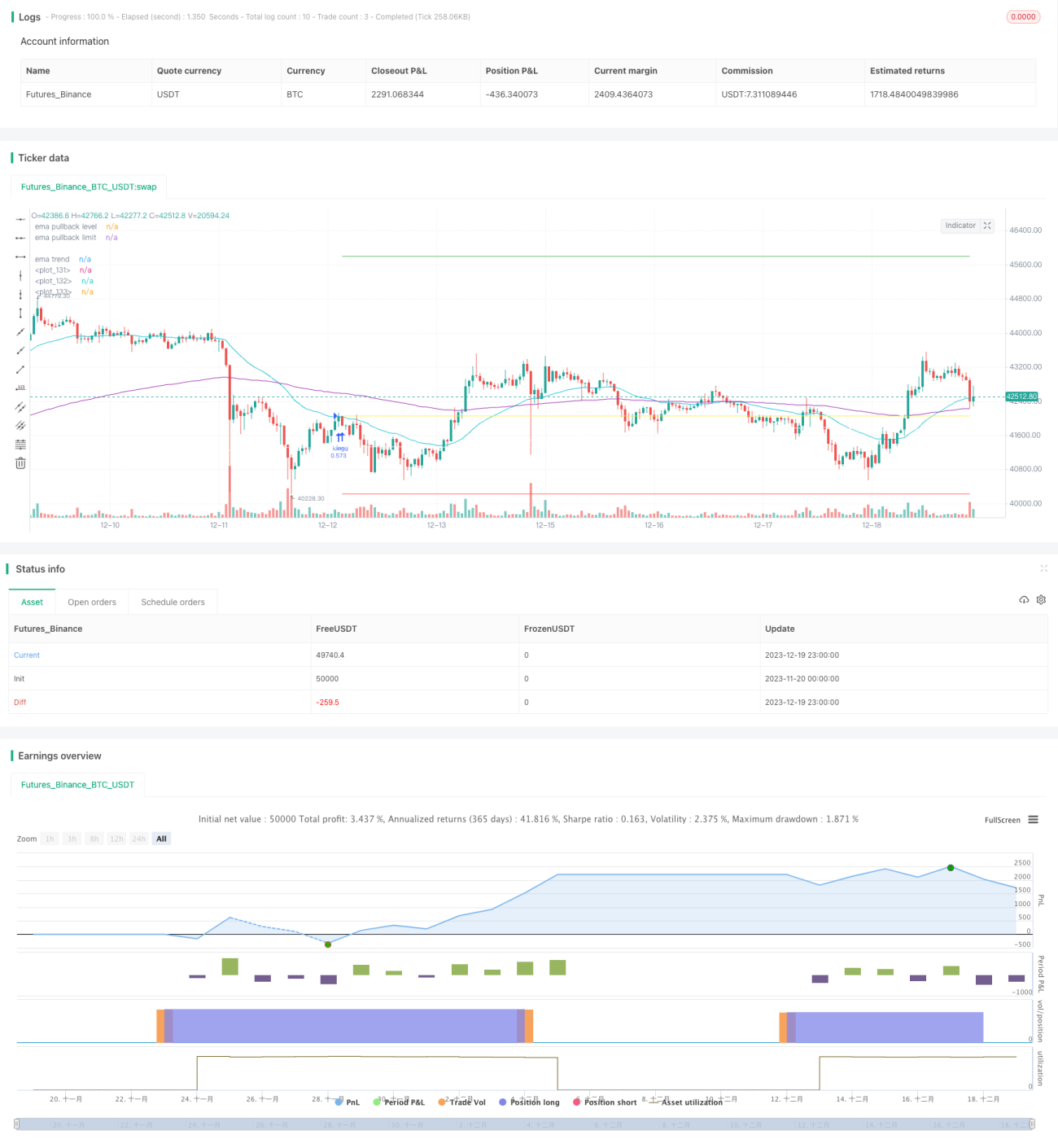

/*backtest

start: 2023-11-20 00:00:00

end: 2023-12-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// created by Space Jellyfish

//@version=4

- 1