Chiến lược quản lý vị thế đòn bẩy cao nhằm ngăn chặn yêu cầu ký quỹ bổ sung

Tổng quan

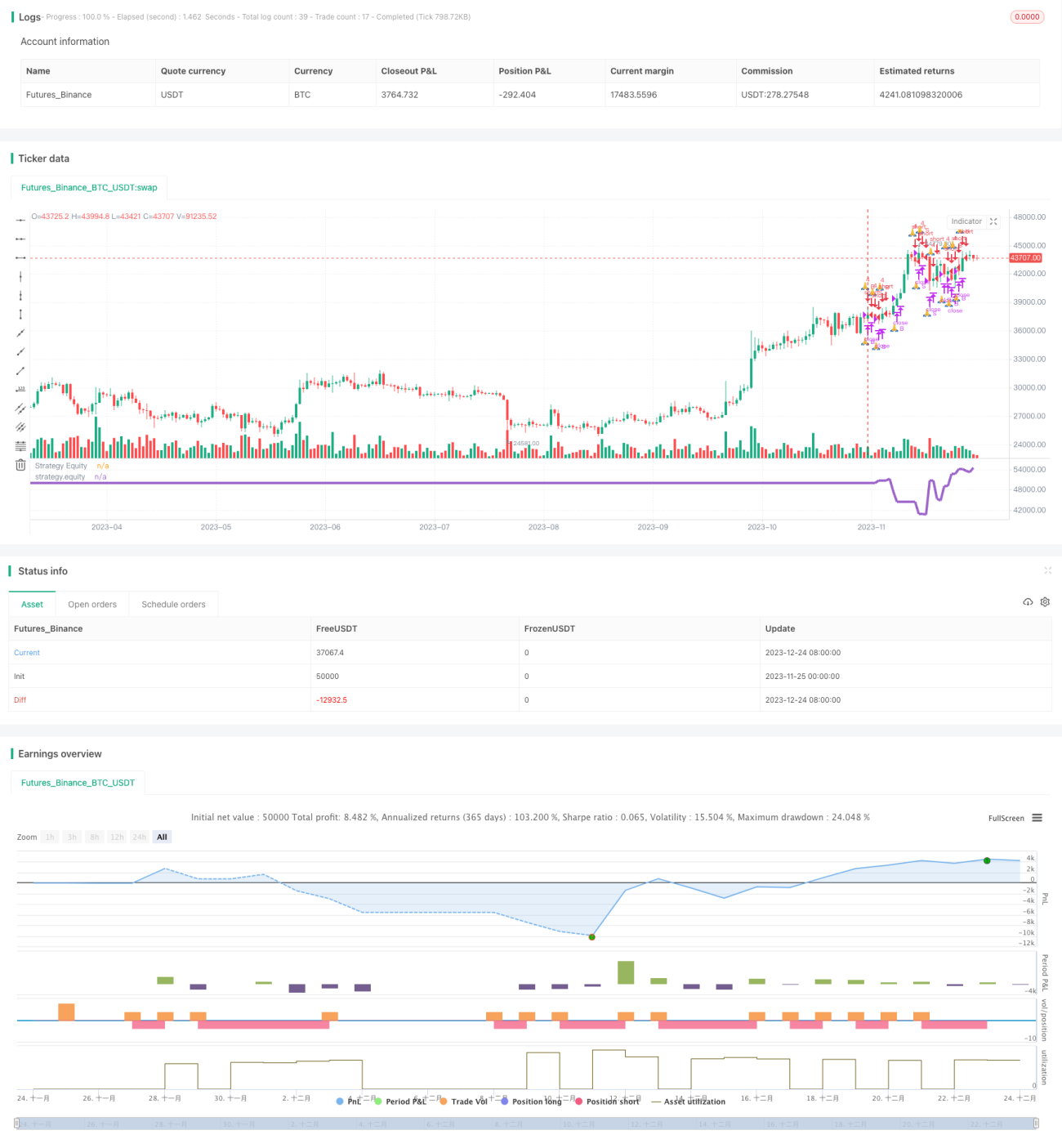

Chiến lược này quản lý rủi ro bằng cách thiết lập đòn bẩy cao và điều kiện ký quỹ bổ sung, kịp thời đóng vị thế khi thị trường biến động mạnh, từ đó ngăn ngừa rủi ro ký quỹ bổ sung.

Nguyên lý chiến lược

- Thiết lập tỷ lệ đòn bẩy cao, ví dụ tỷ lệ đòn bẩy 4x

- Thiết lập mức ký quỹ bổ sung, ví dụ $25,000

- Khi vốn chủ sở hữu thấp hơn mức ký quỹ bổ sung, chiến lược ngừng mở vị thế

- Khi vốn chủ sở hữu tiếp tục giảm và kích hoạt tín hiệu ký quỹ bổ sung, chiến lược đóng tất cả các vị thế

Thông qua các thiết lập trên, có thể kịp thời cắt lỗ khi thị trường biến động mạnh dẫn đến vốn chủ sở hữu giảm nhanh, ngăn ngừa rủi ro ký quỹ bổ sung.

Phân tích ưu điểm

- Có thể linh hoạt thiết lập tỷ lệ đòn bẩy dựa trên khả năng chịu đựng cá nhân, kiểm soát rủi ro từng giao dịch

- Cơ chế ký quỹ bổ sung có thể ngăn ngừa tài khoản bị cháy

- Khi sử dụng đòn bẩy cao, cắt lỗ kịp thời, tối đa hóa việc tránh rủi ro

Phân tích rủi ro

- Đòn bẩy cao khuếch đại lợi nhuận đồng thời cũng khuếch đại rủi ro

- Cần thiết lập hợp lý mức ký quỹ bổ sung, phù hợp với mức cắt lỗ

- Cắt lỗ dễ bị mắc kẹt, cần tối ưu hóa chiến lược cắt lỗ

Có thể giảm rủi ro bằng cách điều chỉnh tỷ lệ đòn bẩy phù hợp, thiết lập mức ký quỹ bổ sung phù hợp với mức cắt lỗ, tối ưu hóa chiến lược cắt lỗ.

Hướng tối ưu hóa

- Kết hợp các chỉ báo xu hướng, tránh mở vị thế ngược xu hướng

- Tối ưu hóa phương pháp cắt lỗ, tránh bị mắc kẹt khi cắt lỗ

- Thiết lập khoảng thời gian không giao dịch, tránh mở vị thế trong các khung giờ nhất định

- Kết hợp thuật toán học máy, điều chỉnh tham số động

Tổng kết

Chiến lược này quản lý rủi ro thông qua đòn bẩy cao và thiết lập ký quỹ bổ sung, có thể ngăn ngừa tài khoản bị cháy. Tuy nhiên, đòn bẩy cao cũng khuếch đại rủi ro, cần tiếp tục giảm rủi ro thông qua các phương pháp như nhận định xu hướng, tối ưu hóa cắt lỗ, kiểm soát thời gian giao dịch. Đồng thời có thể áp dụng các kỹ thuật phức tạp hơn như học máy để tối ưu hóa tham số một cách linh hoạt, tìm kiếm sự cân bằng tối ưu giữa lợi nhuận và rủi ro.

- 1